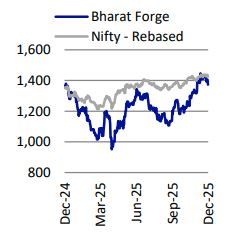

Neutral Bharat Forge Ltd for the Target Rs. 1,290 by Motilal Oswal Financial Services Ltd

Defense, aerospace and JSA to be key growth drivers

Overseas performance improvement contingent upon success of restructuring

We met BHFC management to understand the outlook for its key segments. Defense is likely to be a key growth driver for BHFC given that it now has an order backlog of ~INR114b to be executable over 3-4 years and it has developed capabilities across multiple platforms like ATAGs and carbines and across military and naval applications. The outlook for its aerospace segment is strong as it targets to cross INR3.5b in revenue in FY26 (from INR2.5b in FY25) and the momentum is likely to remain intact going ahead. However, the outlook for US CVs remains weak and is likely to revive only by 2HCY26. While domestic CV OEMs have seen good offtake in the last couple of months, there are no clear signs of a sustainable uptick in MHCV demand in the coming quarters yet. In overseas subsidiaries, a material performance improvement is contingent on the outcome of its restructuring initiatives, which would be clear by 4QFY26. We estimate BHFC to deliver a CAGR of 11%/14%/28% in revenue/EBITDA/PAT over FY25-28. However, despite factoring in all the positives, the stock trading at 54x/38x FY26E/FY27E consolidated EPS appears fairly valued. We reiterate our Neutral rating with a TP of INR1,290 (based on 32x Sep’27E consolidated EPS).

Defense, aerospace and JSA to be key growth drivers ahead

BHFC enjoys an order backlog of almost ~INR114b in defense to be executable over the next 3-4 years. Defense is likely to evolve as a long-term sustainable growth story as BHFC has developed capabilities across multiple platforms like ATAGs and carbines and across military and naval applications. The aerospace business is expected to deliver more than INR3.5b in revenue in FY26E (INR2.5b in FY25) and the momentum is likely to remain intact going forward. Even for JSA, the demand outlook remains healthy, though management is focusing on improving operational efficiencies in business from hereon.

CV outlook remains uncertain

Outlook for US Class8 continues to be weak due to inventory destocking and is likely to pick up only from 2HCY26. Europe CV outlook is stable. For domestic CVs, OEMs have seen good traction in the last couple of months, though management is cautious about sustaining it in 4Q and beyond, especially over a high base. Overseas subsidiaries Management continues to evaluate restructuring options for its

overseas subsidiaries, especially the steel forging units. The outcome of these restructuring initiatives will be critical to drive margin improvement there.

Valuation and View

While 3Q is likely to be similar to 2Q, we expect the demand environment to start improving from 4Q onward. We factor in BHFC to post a CAGR of 11%/14%/28% in revenue/EBITDA/PAT over FY25-28E. However, despite factoring in all the positives, the stock trading at 54x/38x FY26E/FY27E consolidated EPS appears fairly valued. We reiterate our Neutral rating with a TP of INR1,290 (based on 32x Sep’27E consolidated EPS).

Key takeaways from our management meeting are as below

Domestic CVs: No clear visibility of a sustainable uptick

- The current growth in the sector was partly led by strong demand in certain segments like ILCVs and SCVs, seasonal recovery in tippers, and a low base.

- However, management remains cautious about the CV outlook in 4Q and beyond, especially given that 4Q has a relatively high base.

- BHFC continues to be positive on demand revival in LCVs but remains cautious on the MHCV segment.

Export CVs: US Class8 recovery likely only by 2HCY26

- The recent reduction in US tariffs on CV component exports to 25% from 50% is certainly a welcome move for export-focused players like BHFC.

- However, most industry participants await a proper FTA for countries doing business with the US, which would then bring a lot of certainty on future tariffs.

- In 2Q, BHFC had to bear about INR240m of additional impact for absorbing higher tariffs, which will not recur in subsequent quarters.

- However, the US Class8 market continues to see weak demand trends, primarily driven by the deferment of the EPA guidelines. As a result, management expects the market revival to commence by 2HCY26.

- Further, management indicated that the outlook for Europe CV markets is stable currently, albeit at the lower levels.

Non-auto update (excl. defense and aerospace): Stable outlook ahead

- Given weak crude prices, exports are weak in the oil and gas segment and now contribute to just about 25% of this segment. The near-term outlook for this segment remains weak.

- On the other hand, demand continues to be strong from construction and mining segments globally.

- In the domestic market, demand in heavy HP engine applications for standby power like in data centers continues to be robust and is likely to remain a key growth driver for this segment going forward.

Defense and Aerospace will be the key growth drivers for BHFC going ahead

- BHFC has an order backlog of INR95b in defense to be executable over the next 3-4 years.

- However, this does not include the recent carbine order won by BHFC. The Indian Army has signed a contract worth INR27b to buy 425k carbines from BHFC and PLR Systems. BHFC has emerged as the L1 bidder and will supply 60% of the contract value. This order is likely to be signed in a quarter or so and the SOP would commence over 9-12 months after the signing of the contract. This is to be executed over a four-year period.

- KSSL, its 100% subsidiary, has won an INR2.5b contract from MoD for supplying advanced underwater and unmanned marine systems to the Indian Navy. This order is slated for delivery by Nov’26.

- The domestic ATAG order (BHFC’s share worth INR41.4b and included in the above) is likely to commence SOP from FY27.

- Management has indicated that defense is likely to evolve as a long-term sustainable growth story as BHFC has developed capabilities across multiple platforms like ATAGs and carbines and across military and naval applications.

- Given its presence in multiple platforms, BHFC expects to develop a sizeable revenue stream from defense over the next 3-4 years.

- Defense business offers healthy margins and returns.

- Aerospace business is also likely to see strong revenue growth in the coming years. While it ended FY25 with INR2.5b in revenue, it is expected to end FY26 with revenue of more than INR3.5b. This momentum is likely to continue at least for the next 3-4 years.

Update on BFISL – continues to show healthy momentum

- JS Auto Cast continues to see a healthy pickup in demand and management is confident of delivering 15% revenue CAGR in this business in the coming years.

- It is also looking to improve margins in this business and has identified opportunities to improve efficiencies like improving yields, etc.

- For Sanghvi Forgings, BHFC has got a management team in place to revive the business. This business is expected to see a gradual pickup from FY28 onward.

Overseas subsidiaries – restructuring initiatives to drive margin improvement

- Management continues to work on restructuring operations at its European subsidiaries. More specifically, it is currently considering how to restructure its overseas steel business in Europe, while the aluminum business would continue given the upbeat outlook in the long run.

- The decision for restructuring comes from the fact that manufacturing in Europe, especially in Germany, is now becoming increasingly difficult given the sharp rise in inflation like energy and labor costs. Given the adverse macro and the weak domestic demand environment where discounts are reasonably high, European OEMs are not in a position to reprice contracts that would adjust for current inflationary trends. Further, rising interest rates have only added to the pain.

- Things under consideration would involve whether or not to shut down any facility in Europe and if possible, shift production to India, thereby looking to minimizing the revenue loss from this. BHFC may not look to shift anything to India which would not make business sense. It would need to work with key OEMs and understand which business can be shifted to India and which may not be viable even in India and give time to OEMs to scout for an alternative.

K-drive Mobility – management focusing on aggressive growth plans

- In 2Q, this business posted revenue of INR2.9b and EBITDA of INR92m that translates to just 3.1% margin.

- The key reason for weak margin is the old legacy order from a large customer, which has relatively lower margins. Excl. this order, margins for other orders continue to be healthy.

- BHFC would look to drive synergy benefits after the acquisition and strive to improve margins in the coming years in this segment.

- It has a non-compete clause with the US parent for supplies to North America for five years.

- Management continues to have an aggressive growth plan for scaling up this business.

Valuation and view

Continued focus on de-risking the business and increasing value additions

Over the last decade, BHFC has broadened its revenue stream by entering new segments (non-auto) and markets across the globe, resulting in a decline in the share of the auto business to ~56% in FY25 from ~80% in FY07. It has increased value addition by focusing on machined components, whose contribution grew ~50%, boosting realizations and margin. After having invested for over 10 years, it is now seeing meaningful traction in the defense business. It is also ramping up the Al mix in its overseas subsidiaries. These diversification initiatives have helped reduce cyclicality in BHFC revenue over the last few years.

Domestic auto business: Recovery expected in PVs and CVs

After the GST rate cut, the entire auto segment has seen a pickup in demand, especially in the festive season. From BHFC’s perspective, CV segment demand is likely to pick up with a lag. However, management has indicated that they expect CV business to remain flat YoY in 2H. CV demand revival will remain a key monitorable from Jan’26 onward, in our view. Domestic PV segment has also picked up in festive and its revival is expected to continue in the coming quarters. We factor in PV segment to post 7% volume CAGR over FY27-28E.

Defense to be the key growth driver for BHFC over FY25-28E Over the last decade, BHFC has developed new frontiers for growing beyond its core business, with investments in capabilities and capacities in place. Some of these new businesses offer huge potential in the long term and the scope to drive the next phase of evolution for the company. BHFC has ramped up its defense business to INR14.2b in FY24 and further to INR15.7b in FY25, up 10% YoY. On the back of strong demand, its defense order book has scaled up to ~INR95b to be executable over the next 3 to 4 years, which includes the domestic ATAG order worth about INR41.4b, which is likely to commence from CY26 onward. Beyond this, BHFC has recently won a carbine order worth INR14b and an INR2.5b order from Indian Navy for unmanned marine systems. Given the robust order backlog, we expect the defense business to be the key growth driver for BHFC in the coming years.

Auto export outlook remains uncertain

The US CV industry is witnessing a sharp slowdown currently and is likely to pick up only by 2HCY26E. Even auto demand in Europe remains muted. On account of these factors, we expect the export outlook for BHFC to remain subdued at least in the near term, unless we have a favorable tariff reduction.

Valuation and view

Defense, aerospace and JSA are likely to be key growth drivers from hereon. A pickup in the export business, both auto and non-auto, is contingent upon stable US tariffs for India relative to other regions. While 3Q is likely to be similar to 2Q, we expect the demand environment to start improving from 4Q onward. We factor in BHFC to post revenue/EBITDA/PAT CAGR of 11%/14%/28% over FY25-28E. However, despite factoring in all the positives, the stock trading at 54x/38x FY26E/FY27E consolidated EPS appears fairly valued. We reiterate our Neutral rating with a TP of INR1,290 (based on 32x Sep’27E consolidated EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

-96767.jpg)