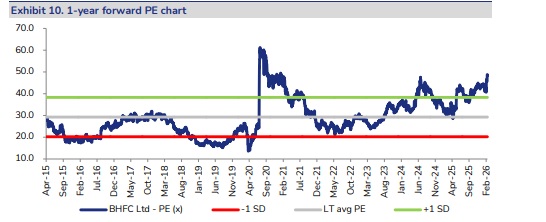

Buy Bharat Forge Ltd for the Target Rs. 2,040 by JM Financial Services Ltd

In 3QFY26, Bharat Forge (BHFC) reported a consolidated EBITDA margin of 17.3% (-70bps YoY/QoQ). Tariff impacts stood at INR 310mn. BHFC’s defence order book expanded to ~INR 111bn (vs. INR 95bn in 2QFY26), supported by the CQB Carbine contract for 250,000 units, which strengthens the Small Arms vertical with a five?year execution runway. The company expects defence revenues of INR 17-18bn in FY26, with ~30-40% growth in FY27 as ATAGS execution begins in 2HFY27. Further, management highlighted that the defence business is expected to achieve EBITDA profitability comparable to the auto segment, with higher ROCE given its lower capital investment. The domestic business is seeing an upcycle in CVs driven by GST 2.0 and the government’s capex push, while the PV segment continues to sustain strong demand momentum. On exports, management indicated that the worst is behind (expects the NA CV cycle to normalize by 1QFY27, compared to operating at roughly half its typical level during the same period last year) and that the company should benefit from the improved outlook following the India?US trade deal. Overall, the ramp?up in defence orders, strong momentum across domestic segments, and improving export trends are expected to drive growth, with management guiding for strong, high-20% revenue growth in FY27. We upgrade our rating from ADD to BUY, with a TP of INR 2,040 at 37x (35x earlier) on FY28E EPS.

? 3QFY26 performance: Consol. revenue stood at INR 43.4bn (+25% YoY, +7.7% QoQ), 3.6% above JMFe. EBITDA margin stood at 17.3% (-70bps YoY/QoQ), 60bps below JMFe. EBITDA stood at INR 7.5bn (+20%YoY, +3.3% QoQ). QoQ Revenue saw growth driven by Defence whereas YoY revenue and EBITDA was impacted by consolidation of K Drive Mobility (revenue/ EBITDA impact of INR 2.9bn/147mn). PAT stood at INR c. 3.3bn (+54.4% YoY, +9.8% QoQ).

? Positive domestic business: Domestic revenue grew significantly 24% YoY (+17% QoQ) to ~INR 11.7bn in 3Q. CV revenue grew 15% YoY (+17% QoQ) to INR 2.6bn due to singificant production volumes increase post GST rate changes. The government’s capex push and an increase in construction and manufacturing activity remain medium-to-long-term growth drivers. PV revenue stood at INR 1bn (+4% YoY, +12% QoQ), pickup in demand post GST rationalisation. The management expects momentum to continue in medium-term. Industrial segment revenue grew 38% YoY (+20% QoQ) to approximately INR 7.1bn. driven by strong execution in Defence and good traction for Heavy Horse-power engines.

? Defence business: BHFC’s defence order book stands at ~INR 111bn, supported by the CQB Carbine deal for 250,000 units, which boosts the Small Arms vertical with a five?year execution window. Defence revenues are guided at INR 17-18bn for FY26 with ~30-40% growth in FY27, alongside ATAGS order execution beginning in 2HFY27

? Export business outlook – worst is behind: Export revenue declined 21% YoY (-3% QoQ) to INR 9.1bn in 3QFY26. CV segment revenue stood at INR 2.5bn (-51% YoY, -13% QoQ), due to de-strocking and tariff uncertainty weighed on CV demand in NA. PV segment revenue, however, grew 7% YoY (-12% QoQ) to INR 2.6bn. Despite the challenges in the US, the YoY growth was primarily led by diversification efforts across geographies and products. Further, the management anticipates a recovery in consumer confidence as trade disputes subside. Industrial revenue declined approximately 1% YoY (+11% QoQ) to INR 4bn, led by mixed performance across segments (HHP engines/aerospace improved execution, however, oil & gas was weak due to weak crude prices). Overall, the management indicated that the worst is behind and things are started to look up with the trade deal between India and the USA.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361