Add Siemens Energy AG For Target Rs.3,900 By InCred Equities

Extending strength into next year

* Siemens Energy beat street’s 4QFY25 revenue/EBITDA/PAT by 23%/10%/2% on the back of strong project biz execution in power transmission (+48% YoY).

* Order inflow came in flattish YoY at Rs23.5bn (advancement of orders last quarter). Backlog grew by 47% YoY to Rs162.1bn (2.1x FY25 sales).

* Maintain ADD rating with a higher target price of Rs3,900 as we build in one HVDC worth Rs48bn in FY26F and assign 65x on FY27F EPS of Rs59.6.

Strong broad-based execution-led growth

4QFY25 revenue of Siemens Energy grew by 27.3% YoY to Rs26.5bn. Gross margin grew by 100bp YoY to 35.6%. The EBITDA margin came in at 18.1% vs.18.5% in 4QFY24 and 19.1% last quarter (hit due to higher revenue mix of project business). PAT grew by 31.4% YoY to Rs3.6bn. Order inflows were flattish YoY at Rs23.5bn. Backlog at Rs162.1bn (2.1x FY25 sales). The company’s board recommended a dividend of Rs4/share. Segmental: Power transmission segment’s revenue grew by 48% YoY to Rs13.6bn (51.4% mix). The EBIT margin stood at 18.1% (+200bp YoY). Power generation revenue rose by 11% YoY to Rs12.9bn (48.6% mix). The EBIT margin stood at 15.6% (320bp down YoY).

A case of diversification and longevity

The ongoing global transmission super-cycle on the back of energy transition theme provides visibility, not to mention potential scale-up in industrial capex (once private capex picks up) where it has diverse offerings such as turbines, compressors, gensets, etc. comprising ~50% of revenue mix. We feel that over next few years, around eight-to-nine HVDCs (~five being VSCs) domestically shall be prime growth drivers, apart from playing a crucial role as feeders to parent group cos. Siemens Energy is a potential candidate for imminent margin uptick led by high-margin VSC HVDCs in pipeline along with exports.

Optimistic outlook, given golden pipeline at play

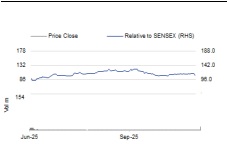

Siemens Energy, listed on stock exchanges on 19 Jun 2025 (demerged from Siemens India), tactically focuses across entire energy value chain offering customers greater focus and agility, while unlocking shareholder value. Given strong electrification demand in India (Rs9.15tn T&D capex over 2023-32F;nine HVDCs in pipeline), public capex uptick, and growth in data centres, the company is incurring a capex of Rs2.8bn for expanding its HV switchgear and transformer capacities which cater to both domestic and export demand.

Outlook and valuation

We build in one HVDC worth Rs48bn (likely Khavda-South Olpad VSC) in FY26F as base order inflow should continue to showcase ~30%-plus CAGR over the next two-to-three years on the back of energy transition playing out as a global theme, with MNCs being better positioned given exports a key optionality. Maintain ADD rating on stock with a higher target price of Rs3,900 (Rs3,850 earlier). Downside risks: Export slowdown, working capital management, execution delay due to supply chain constraints, rising competition, etc

Above views are of the author and not of the website kindly read disclaimer

600-400.jpg)