Buy Aditya Birla Capital Ltd for the Target Rs.415 by Motilal Oswal Financial Services Ltd

Strengthening fundamentals across all businesses

Broad-based momentum across NBFC and HFC, with improving asset quality

* Aditya Birla Capital (ABCL) is entering a structurally stronger earnings phase, supported by synchronized momentum across its lending, asset management, and insurance franchises. The company has demonstrated robust operating execution through FY26YTD, with broad-based improvement in growth, asset quality, and profitability across its core businesses.

* Importantly, the recent phase of portfolio recalibration within the NBFC business is now largely behind the company, and the group has resumed calibrated growth in higher-yield segments while maintaining risk discipline. We expect the contribution of the P&C book to continue rising, which should act as a key lever for margin expansion as the portfolio mix normalizes and yields improve.

* By prioritizing a digital-first ecosystem, the company has successfully pivoted toward high-growth retail and MSME segments. This transformation is anchored in proprietary platforms like the ABCD App and Udyog Plus, which serve as the backbone for enhanced operational productivity. This digital push, complemented by a robust omnichannel strategy, has fundamentally tightened D2C engagement and widened the firm's market footprint.

* We remain constructive on the company’s outlook, underpinned by sustained momentum across its diversified franchises, continued improvement in asset quality, and strengthening earnings visibility. With its core platforms scaled, growth engines firing across segments, and a sizeable addressable opportunity across retail, MSME, and insurance markets, the company is well-positioned to transition into its next phase of disciplined, scalable, and profitability-led expansion.

* With the housing finance subsidiary well capitalized following the recent equity infusion from Advent International, and with steady expansion in AMC and insurance profitability, ABCL is well positioned for sustained earnings compounding over the next two years. We expect consolidated PAT CAGR of ~26% over FY26–28 and RoE expansion to ~16% by FY28. Reiterate BUY with a Mar’28E SoTP-based TP of INR415.

NBFC: Growth resumes with improving asset quality and margins

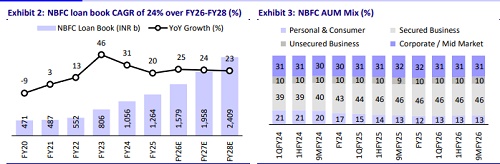

* The NBFC business has moved beyond its risk recalibration phase and is witnessing broad-based growth across retail, MSME, and unsecured segments. Disbursement momentum has strengthened over the past two quarters, reflecting a return to balanced and sustainable growth, with a calibrated rebuild of the unsecured portfolio.

* As the share of higher-yielding segments, particularly P&C, increases, we expect gradual margin expansion and improvement in RoA. Asset quality remains robust, with consolidated GS2+GS3 improving 150bp YoY and unsecured GS3 at 1.9%, nearly 40% of which is backed by government guarantees, limiting downside risk and supporting stable credit costs.

* We expect the NBFC loan book to double over the next three years, supported by an improving product mix, operating leverage, and steady RoA expansion.

HFC: Accelerating growth with improving profitability and strong capital support

* Aditya Birla Housing Finance (ABHFL) has emerged as a key growth driver for ABCL, having built a full-stack housing finance franchise across prime, affordable, and construction finance segments, backed by investments in technology, distribution, and analytics. Over the past three years, the HFC loan book has expanded at a robust CAGR of 48% to INR422b, with growth well diversified across segments.

* Importantly, rapid scale-up has been accompanied by improving asset quality, with 30+ dpd declining from 2.9% in Mar’24 to 1% as of Dec’25, underscoring disciplined underwriting and portfolio granularity. The recent INR27.5b capital infusion from Advent International significantly strengthens the balance sheet, providing growth headroom to sustain momentum, accelerate market share gains, and improve profitability.

* We expect ABHFL to maintain strong growth, with operating leverage driving steady RoA expansion as the loan book scales over the medium term

AMC: Broad-based growth across MF, alternatives, and passives

* ABSL AMC has delivered healthy growth momentum, supported by improving fund performance, steady SIP inflows, and strong traction across alternatives and passive products. The mutual fund franchise remains anchored in consistent retail participation, with ~4m contributing SIP accounts providing visibility into stable, long-term equity inflows.

* The alternatives platform has scaled meaningfully, aided by large institutional mandates such as ESIC, while the PMS/AIF business continues to build organic momentum among HNIs and family offices. The passive segment is emerging as a key growth driver, with ETFs and precious metal offerings gaining traction and enhancing product diversification.

* Expansion into offshore and GIFT City operations, along with progress on mandates such as EPFO, strengthens the AMC’s positioning for diversified and structurally sustainable long-term growth.

Life and health insurance

* The life insurance business continues to scale, supported by an improving product mix and strengthening distribution across proprietary and banca channels, including deeper penetration with partners such as Axis Bank. Growth is increasingly value-accretive, driven by strong traction in ULIPs and Credit Life, including cross-sell within the group ecosystem. Despite GST headwinds, VNB margins remain resilient, with management guiding for over 20% CAGR in individual FYP and a doubling of net VNB over the next three years.

* The health insurance business continues to outpace industry growth, led by robust expansion in the corporate segment and steady improvement in profitability. Its differentiated, digitally enabled health-first model enhances customer selection and engagement, improving unit economics and positioning the franchise for sustainable, margin-accretive growth.

Valuation and view

* ABCL continues to deliver healthy growth across its core businesses - NBFC, HFC, AMC, and life and health insurance - supported by improving profitability, operating leverage, and sustained customer acquisition momentum. The ‘One ABC’ strategy is strengthening cross-sell, enhancing wallet share, and driving cost efficiencies, while ongoing investments in digital capabilities and distribution expansion provide structural support to long-term growth.

* We expect consolidated PAT CAGR of ~26% over FY26-28, with improving mix and operating leverage driving RoE expansion to ~16% by FY28. Reiterate BUY with a Mar’28E SoTP-based TP of INR415.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041