Buy Larsen & Toubro Ltd for the Target Rs.4,400 by Motilal Oswal Financial Services Ltd

Turning into ‘moving parts’ from ‘sum-of-the-parts’

With a constantly changing scenario in the Middle East impacting core EPC business and increasing risks for IT business from AI-led disruption, LT is turning more into a ‘moving parts’ thesis from a ‘sum-of-the-parts’ thesis. While we are positive about the company’s growth outlook based on its strong order book and prospects of healthy core PAT earnings over FY25-28E, we do believe that near-term headwinds persist on 1) international revenue, with the Middle East accounting for nearly 39-40% of its total order book as of 9MFY26; and 2) IT subsidiary’s valuations, which are getting impacted by AI-led disruption. We have limited clarity on how things will unfold in the Middle East over the medium term, but in the near term, it can impact execution as well as margins for certain projects. We adjust our core business valuations to 25x (from 27x) to bake in the current volatile scenario for now and arrive at a revised twoyear forward TP of INR4,400 (vs. INR4,600 earlier). Retain BUY

International business accounts for majority of core business revenue

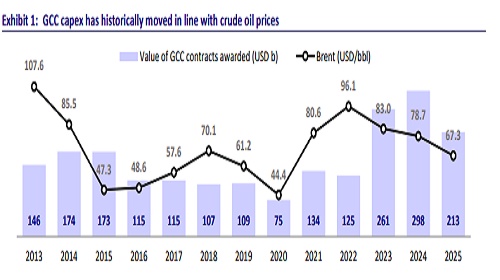

As of 9MFY26, international order inflows and order book stood at INR1.54t/INR3.8t, with the Middle East forming 75% of its international order book. International inflows contributed to 51%/57%/53% of total inflows in FY24/FY25/9MFY26. International revenue contributed to 34%/44%/50% of its total revenue in FY24/FY25/9MFY26. Within the Middle East, LT has diversified its country base, such as Saudi Arabia, Kuwait and Qatar, and has also diversified its project mix across hydrocarbon – onshore as well as offshore, gas-related projects, renewables, and transmission. We believe that in the near term, execution can be impacted by supply chain disruption, while in the long term, the company has adequate risk management in place for existing contracts. In the medium to long term, whenever oil prices have moved up, overall capex spending has also moved up in the GCC region, where LT has now created a strong position.

Domestic business is currently growing from select segments

Domestic segment ordering was largely flat over FY23-25 and had started growing in FY26, driven by large thermal power projects, building and factories, domestic refineries and metals. While government capex spending has been weak across large projects, the company remains optimistic about gaining a larger share from thermal power projects, real estate as well as select private sector industries. Domestic order inflows grew by 29% YoY in 9MFY26 to INR1.35t vs. INR1.2t over FY23-FY25. This can provide some support to overall order inflows in case international order inflows turn weak in the near term.

Subsidiary valuations impacted by AI-led disruption for IT business

In businesses other than core E&C, a larger part of the SoTP valuation is driven by IT businesses, which are currently getting impacted by AI-led disruption. As per our IT analyst, IT sector revenue faces direct exposure to AI-driven productivity/displacement risk, with incremental pressure from third-party software efficiencies and automation layers. We are constantly watching the scenario

Near-term headwinds persist with limited clarity as of now

LT’s core business two-year forward P/E multiple had remained strong at 25x just prior to the recent Middle East conflict on the back of a strong order book, expectations of execution scale-up, non-core business divestments, and the scale-up expected in defense, data centers and real estate. We expect these areas to remain strong going forward too. However, in the near term, headwinds persist on 1) international revenue, with the Middle East accounting for nearly 39-40% of total order book as of 9MFY26; and 2) IT subsidiary’s valuations, which are getting impacted by AI-led disruption. We have limited clarity on how things will unfold in the Middle East over the medium term, but in the near term, it can impact execution as well as margins for certain projects. We adjust our core business valuations to bake in the current volatile scenario for now and arrive at a revised two-year forward TP of INR4,400 (vs. INR4,600 earlier). Retain BUY.

Key risks and concerns

A slowdown in order inflows, geopolitical issues, delays in the completion of mega and ultra-mega projects, a sharp rise in commodity prices, an increase in working capital, and increased competition are a few downside risks to our estimates.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)