Hold Escorts Kubota Ltd For Target Rs. 3,249 By Geojit Financial Services Ltd

Overall tractor volume below expectation.

Escorts Kobota Ltd (EKL) is the third largest agricultural tractor manufacturer in India. It has a strong presence in the north & west markets, with a 11.1% market share.

* We expect the volume growth to improve in Q4 and in FY26 due to rural development and strong agricultural output owing to better reservoir levels. In addition, government’s infra project push will support the overall construction equipment sales.

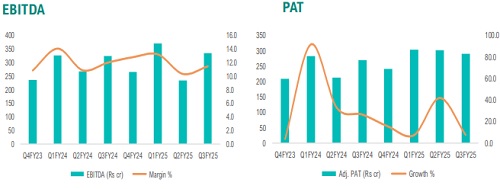

* 9mFY25 standalone revenue grew by 7% YoY due to superior mix and price hike. The tractor segment grew by 9.4%YoY, while Construction equipment grew by 4.3%YoY.

* EBITDA margin contracted by 185bps, owing to weak sales and lower operating leverage. On a 9month basis Adj. PAT grew by 17%YoY.

* We expect mid single digit growth for the domestic tractor segment for the fiscal year. Furthermore, the lacklustre performance of exports is likely to continue in the near term due to adverse geopolitical economic situations.

* Currently, Kubota holds the major stake in the EKL and also enjoys 30% of the global tractor market share. This will enable EKL to expand its geographical footprint into the western market in the long run.

Outlook & Valuation

Given the pick up in rural demand and better crop output, we expect green shoots in tractor sales. In addition, new launches in the construction equipment and tractor to support overall volume growth. We expect the margin to show resilience at the current level due to softening raw material prices and cost control initiatives. However, considering the slow ramp in exports, the partnership gains with Kubota in agribusiness are expected to take longer than initially anticipated due to sluggish international markets. The near-term pressure in demand has brought some consolidation to the current valuation. Considering the optimistic outlook, we value EKL at 26xFY27E EPS recommend Hold rating at CMP with a revised target price of Rs.3,249

For More Geojit Financial Services Ltd Disclaimer https://www.geojit.com/disclaimer

SEBI Registration Number: INH200000345