Buy ICICI Prudential Life Insurance Ltd for the Target Rs. 800 by Motilal Oswal Financial Services Ltd

VNB margin consistent sequentially at 24.4%; 90bp beat

Protection contribution continues to rise

* ICICI Prudential Life Insurance (IPRU) reported APE of INR25.3b (in line), up 4% YoY, in 3QFY26. In 9MFY26, APE declined 1% YoY to INR68.1b.

* VNB margin expanded 320bp YoY to 24.4% vs. our estimate of 23.5%. Absolute VNB grew 19% YoY to INR6.2b (in line) in 3QFY26. For 9MFY26, VNB grew 6% YoY to INR16.6b, reflecting an improvement in VNB margin to 24.4% (22.8% in 9MFY25).

* PAT grew 19% YoY to INR3.9b (21% beat) in 3QFY26 (23% YoY growth for 9MFY26).

* Management indicated that GST reforms should be value-accretive for all stakeholders, including distributors. Partner-specific negotiations are underway to ensure VNB neutrality while maintaining distributor economics.

* We have maintained our APE growth estimates for FY26-28. However, we have raised VNB margin assumption by 50bp/50bp/100bp for FY26/27/28, considering the 3QFY26 performance. We maintain our BUY rating with a TP of INR800 (based on 1.7x FY28E EV).

Favorable product mix driving VNB margins

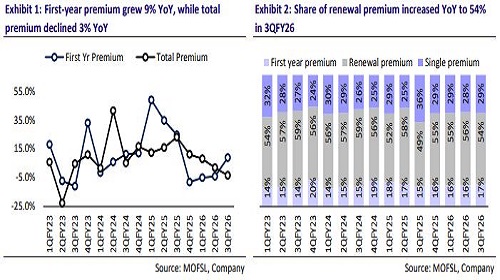

* IPRU’s gross premium declined 3% YoY to INR122b (13% below estimates) in 3QFY26, driven by 8% YoY growth in renewal premium, while single premium declined 25% YoY.

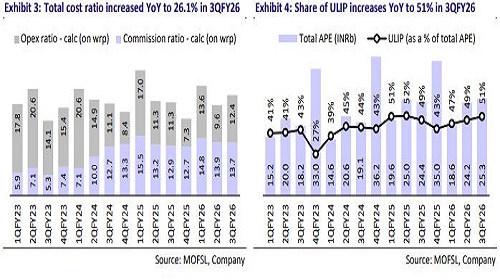

* APE growth of 4% YoY in 3QFY26 was driven by 19% YoY growth in protection, partly driven by GST exemption, 8% YoY growth in ULIP and 5% YoY growth in non-par savings. Annuity business continued to decline YoY owing to a high base due to product launch last year. Retail growth was partially offset by 43% YoY decline in the lumpy group business. The retail contribution to APE continued to rise and was at 83.8% in 3QFY26.

* The 320bp YoY expansion in VNB margin to 24.4% was driven by a higher contribution from the non-linked business at 18.1% (11% in 3QFY25), along with continued growth in retail protection contribution from 6% in 3QFY25 to 8.2% in 3QFY26 (overall protection contribution at 18.4% in 3QFY26 from 16% in 3QFY25). Other margin improvement drivers included higher sum assured, rise in rider attachments and favorable yield curve movement.

* Commission expenses grew 12% YoY to INR12.7b, while operating expenses grew 15% YoY, resulting in a rise in EoM ratio from 16.4% in 3QFY25 to 19.3% in 3QFY26. However, on a 9M basis, the cost ratio has improved to 19.3% from 19.8% last year despite the loss of input tax credit.

* On the distribution front, agency/direct channels were largely flat YoY, contributing 29%/15% to the mix owing to a high base. The bancassurance channel witnessed growth of 10% YoY, with contribution rising from 25% in 3QFY25 to 27% in 3QFY26. Corporate agent channel continued to witness strong growth (+52% YoY), contributing 13.5% to the mix (from 9.2% in 3QFY25), backed by strong growth in traditional products. The group channel declined 20% YoY, resulting in contribution declining from 21% in 3QFY25 to 16.2% in 3QYF26.

* On a premium basis, persistency declined in 3QFY26, with 13th month persistency at 81% (85.6% in 3QFY25) and 61st month persistency at 58.6% (62.6% in 3QFY25). However, 37th month persistency improved from 72.7% in 3QFY25 to 74.9% in 3QFY26.

* AUM grew 7% YoY to INR3.3t, while solvency improved to 214.8% (211.8% in 3QFY25)

Highlights from the management commentary

* APE growth in 9MFY26 was slow owing to a supportive market environment last year, which supported ULIPs and annuity product launch. IPRU delivered a twoyear APE CAGR of 13.8%, marginally ahead of the industry’s 13.3%, with management indicating improving momentum based on trends seen in 3QFY26.

* Retail protection remains a structural opportunity, with only ~13% of the population currently protected. Group protection growth remained in single digits, impacted by a slowdown in MFI-linked credit life during 9MFY26, though early signs of recovery were seen in 3Q, which should benefit the company going forward.

* Persistency ratios remained below desired levels, though management outlined multiple corrective actions, which should lead to a recovery in 13M persistency to 85%+ by next year.

Valuation and view

* IPRU’s continued efforts toward product mix shift, increasing retail protection contribution and robust cost optimization measures have resulted in continued YoY expansion in VNB margin, despite the loss of input tax credit after GST exemption. In the longer term, the company’s profitability will be supported by higher volumes driven by GST exemption, increased traction of non-linked products, and improved product-level margins.

* We have maintained our APE growth estimates for FY26-28. However, we have raised VNB margin assumption by 50bp/50bp/100bp for FY26/FY27/FY28 considering the 3QFY26 performance. We maintain our BUY rating with a TP of INR800 (based on 1.7x FY28E EV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412