Buy ICICI Lombard Ltd for the Target Rs.2,230 by Motilal Oswal Financial Services Ltd

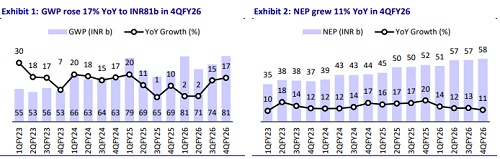

* ICICI Lombard (ICICIGI)’s gross written premium grew 17% YoY in 4QFY26 to INR80.7b (in line). NEP rose 11% YoY to INR57.9b (6% miss) in 4Q, while it grew 13% YoY to INR222.6b in FY26.

* ICICIGI’s claims ratio for the quarter stood at 70.8% (vs our est. 70.9%) vs 71.6% in 4QFY25. The expense ratio came in at 12.1%, which was flat YoY (in line). The commission ratio was 18.3% vs. 18.7% in 4QFY25 (our expectation at 19.6%).

* The combined ratio stood at 101.2% (vs. our expectation of 102.5%) compared to 102.5% in 4QFY25. For FY26, the combined ratio was 103.4% (102.4% excluding the impact of 1/n) vs. 102.8% in FY25.

* PAT at INR5.5b grew 7% YoY (23% miss), hit by lower-than-expected investment income and INR0.5b of impairment on the equity portfolio. For FY26, ICICIGI’s PAT grew 11% YoY to INR27.7b.

* Management expects high single-digit industry growth for the motor insurance business in FY27, aiding ICICIGI’s growth trajectory. Fire insurance growth is likely to be muted due to price discounting. The insurer is awaiting opportunities in the crop insurance market but will remain selective.

* We have cut our NEP/PAT estimates by 2%/3% and 6%/2%, respectively, for FY26/27, considering the 4QFY26 performance. We expect the combined ratio to improve to 101.8% by FY28, considering a stable claims environment and continued operational efficiency. Reiterate BUY with a TP of INR2,230 (based on 28x FY28E EPS).

Recovery in motor segment and continued market share gains in health

* ICICIGI’s NEP grew 11% YoY, fueled by a 19% YoY growth in the health (including PA) segment. The fire segment grew 11% YoY, while the motor segment grew 6% YoY.

* The continued momentum with respect to fresh business in the motor and health segments post-GST reductions resulted in higher URR creation and a 6% NEP miss.

* Underwriting loss was INR2.8b compared to a loss of INR2.1b in 4QFY25 (vs. our estimates of INR2.3b).

* Total investment income on policyholders' accounts was 12% below our estimates at INR8.3b. For the shareholders' accounts, it was 20% below our estimates at INR2.4b, largely due to an MTM on the debt portfolio.

* The claims ratio at 70.8% improved 80bp YoY due to a 90bp improvement in the motor OD loss ratio and a 700bp YoY improvement in the motor TP loss ratio. The insurer has recalibrated its motor portfolio to drive claims efficiency. The health segment’s loss ratio improved 80bp YoY due to the retail health segment, which improved 680bp YoY. Commercial lines’ loss ratio increased YoY due to heightened competitive intensity.

* The investment book grew 9% YoY to INR584.2b, reflecting a strong investment leverage of 3.5x. Absolute investment yield for FY26 was 8.5%, which was slightly higher YoY (vs. 8.4% in FY25). The investment portfolio mix for FY26 stood at 40.8%/35%/18.7% for corporate bonds/G-Sec/equity (incl. equity ETF).

* The impact on profitability due to impairment of equity assets led to an RoE of 13.3% for 4QFY26 vs. 14.5% in 4QFY25. For FY26, RoE was at 17.8% compared to 19.1% in FY25 (excluding the wage code impact, RoE was 18.1% for FY26).

* The solvency ratio stood at 2.67x (vs. 2.69x in 4QFY25).

Key highlights from the management commentary

* The commercial lines’ growth moderated in 2HFY26 for the industry due to elevated competitive intensity in the fire segment. Renewals from 1st April 2026 are at discounted pricing, reflecting continued pressure.

* ICICIGI’s CV contribution remained stable at ~22%. The company is selectively evaluating opportunities in CV, leveraging its strengths in fleet management. While PV and 2W remain core strengths, CV traction has been gradually improving and is expected to contribute better going forward.

* The focus in commercial lines remains on underwriting discipline and profitability amid heightened competitive intensity, which has led to some market share loss. However, ample reinsurance capacity has helped mitigate competitive pressures.

Valuation and view

* ICICIGI witnessed a better-than-industry growth trajectory in 2HFY26, driven by recovery in motor insurance (owing to GST cuts) and strong market share gain in retail health (additional boost from GST exemption).

* The company's retail health segment continues its strong momentum, gaining market share through effective new customer acquisition, strong distribution capabilities, and significant traction of its "Elevate" product. Competitive intensity remains high in the motor OD segment, but the company has witnessed recovery driven by rising fresh vehicle sales. While the commercial lines segment is expected to face heightened competition, ICICIGI is well-positioned to capture profitable business within the segment.

* We cut our NEP/PAT estimates by 2%/3% and 6%/2%, respectively, for FY26/27, considering ICICIGI’s 4QFY26 performance. We expect the combined ratio to improve to 101.8% by FY28, given a stable claims environment and continued operational efficiency. Reiterate BUY with a TP of INR2,230 (based on 28x FY28E EPS).

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041

.jpg)