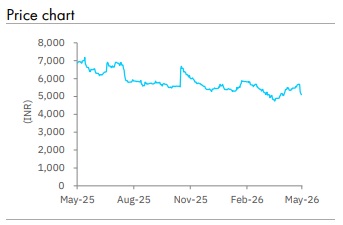

Accumulate Blue Dart Express Ltd for Target Rs 5,963 by Elara Capital

Ground network to drive growth

Blue Dart Express (BDE IN) delivered a steady Q4, with growth momentum supported by continued rise in e Commerce and surface express shipments. However, increasing contribution from heavier freight shipments resulted in softer realization. Surface logistics remain s a key growth driver, supported by expanding customer penetration and strengthening multimodal capabilities across the network. Operational efficiency was maintained by healthy aircraft utilization levels, network optimization , and pricing actions implemented from January. Future c apital allocation is focused on aircraft maintenance, automation, mate rial handling infrastructure , and select network expansion, while reiterating confidence in sustaining long -term profitability . We lower our earnings estimates by 12% for FY27 and 11% for FY 28. We retain Accumulate with a lower TP of INR 5,963 valuing the express segment at 35x ( unchanged) FY28E P/E and equity investment in Blue Dart Aviation (100% subsidiary) at book value .

In-line revenue; margin lower than our estimates:

BDE reported 8.2% YoY revenue growth to INR 15.3bn in Q 4FY26, led by an 8.7% YoY increase in tonnage to ~ 359,913 tonne and 4.6% YoY rise in shipments to 96.2mn. Tonnage growth outpaced shipments led a by higher share of heavy volume freight . Realization per shipment increased by 3.4% YoY while realization per kg remains flat YoY . EBITDA margin declined 20bp YoY to 8.1%, dragged by higher vehicle hiring and employee cost on account of setting up new functions . Adjusted PAT decreased by 18.5% YoY to INR 434m n

Surface-led growth sustains momentum:

The revenue mix remain s tilted toward B2B shipments, while B2C contribution remain stable at ~30% of revenue, driven by e Commerce volume. Surface express continue s to outpace air express growth, led by rising ground -based eCommerce movements, warehouse -to-store replenishment shipments , and increasing preference for cost -efficient logistics solutions. The quarter witnessed a shift toward heavier freight shipments, moderating realization growth despite pricing actions und ertaken from January. Continued focus on network optimization, multimodal integration, and automation supported operational efficiency, while freighter utilization remain s healthy at ~85% levels. Management says growth momentum continue s to be supported by sustained traction in eCommerce, B2B supply chain movements , and expanding ground express penetration across the domestic logistics network.

Retain Accumulate with a lower TP of INR 5,963:

Management expects surface to outpace air volume amid rising preference for cost -efficient transportation. Margin trajectory remain s dependent on shipment mix, pricing discipline, network optimization , and operating leverage . C ontinued investments in automation and infrastructure are set to support long - term efficiency. We lower our earnings estimates by 12% for FY27 and 11% for FY28 to factor in moderation in growth amid risk s of rising crude and aviation turbine fuel prices . We introduce our FY29 estimate s. We re tain Accumulate with a lower TP of INR 5,963 from INR 6,683, valuing the express segment at 35x (unchanged) FY28E P/E and investment in Blue Dart Aviation (100% subsidiary) at book value.

Please refer disclaimer at Report

SEBI Registration number is INH000000933