Neutral Shoppers Stop Ltd for the Target Rs.345 by Motilal Oswal Financial Services Ltd

Weak 3Q; profitability to remain under pressure

* Shoppers Stop (SHOP) reported a weak 3Q, with performance impacted by weaker-than-anticipated discretionary demand amid an early festive shift, resulting in operating deleverage.

* Store expansion remained muted, with two net store closures as portfolio rationalization continued. INTUNE’s ramp-up slowed materially, with only 3/14 store additions in 3Q/9MFY26, as focus shifted from scaling to fixing the supply chain and inventory execution.

* Gross margins contracted ~127bp, driven by earlier EOSS and inventory provisioning, while negative operating leverage amplified the impact, leading to a sharp profitability decline. Pre-Ind AS EBITDA fell ~50% YoY to INR461m.

* Premiumization initiatives continued to deliver, with improved premium mix and footfall trends supported by enhanced in-store experience.

* Nevertheless, profitability constraints persist, with low core segment margins, elevated losses in new ventures, and muted store expansion constraining the pace of earnings recovery.

* We tweak our FY26-28E, while EBITDA remains broadly unchanged, as a slower ramp-up in INTUNE was partly offset by improved performance in departmental. We build in FY25-28E revenue/EBITDA CAGR of 6%/7%.

* We value SHOP at 20x FY28E pre-INDAS EBITDA to arrive at our revised TP of INR345. Reiterate Neutral.

Weak performance impacted by a shift in festive and operating deleverage

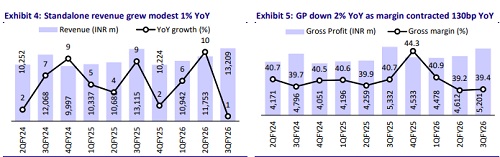

* SHOP’s standalone revenue was flat YoY at INR13.2b (vs our est of 5% growth), owing to the shift in the festive season (2Q+3Q revenue was up 5% YoY).

* Departmental store revenue remained flat; however, the format continued to witness strong LFL footfall growth of 5%, marking the second consecutive quarter of growth.

* Premiumization continues to drive growth, with the premium mix growing 6% (LFL 6% vs. 14%/9% in 2Q/1Q). Top categories include Beauty (14%), Handbags (13%), and Watches (12%).

* The Beauty segment’s (ex-distribution) revenue grew 2% YoY, while including distribution, revenue grew 19% YoY.

* Revenue from INTUNE stood at INR770m (vs. INR700m QoQ, up 22% YoY), with presence expanding to 81 stores (vs. 78 QoQ).

* Store additions remained muted, with the company reporting two net store closures (seven opened and nine closed).

* Respective store count stood at Departmental: 110 (three opened, four closed), Beauty: 79 (five closed), INTUNE: 81 (three opened), and Home Stop: 11 (one addition), with the total store count at 301.

* Gross profit declined 2% YoY to INR5.2b (7% below estimates), as gross margins contracted ~112bp YoY to 39.4%.

* Employee costs/other expenses increased 4%/7% YoY.

* EBITDA declined 13% YoY to INR2.1b (15% below), with margins at 15.9% (contracting ~240bp YoY, 210bp miss), owing to operating deleverage.

* Pre Ind-AS operating profit stood at INR461m (vs. profit of INR877m in 3QFY25), with margins at 3.5% (vs 6.7% in 3QFY25).

* YTD Pre-IND AS EBITDA stood at INR756m (vs INR1.1b YoY), with margins at 2.1% vs 3.2%.

* Depreciation and interest costs rose 1%/9% YoY.

* The company recognized a one-time exceptional charge of INR175m in 3Q/9MFY26 arising from the New Labor Codes.

* Reported PAT stood at INR126m (vs INR488m in 3QFY25). Adj for this, provision PAT stood at INR301m.

Segment performance

* The core segment reported INR15.2b revenue (flat YoY), with Pre-IND AS EBITDA at INR900m (down 24% YoY) and margins of 5.9% (down ~190bp on account of operating deleverage).

* New ventures reported sales of INR830m (up 30% YoY), with Pre-IND AS EBITDA loss of (-) INR200m (loss doubled YoY).

* Segment-level EBITDA includes other income.

INTUNE: Scale-up remains challenging

* INTUNE delivered weak growth, with revenue at INR770m (+22% YoY vs 70% in 2Q), driven by legacy inventory, lower freshness, and heavy discounting in a competitive value-fashion market.

* Expansion has been deliberately curtailed, with only ~14 stores added in 9MFY26 vs initial guidance of 30–40, as focus has shifted from scaling to fixing supply chain and inventory.

* Inventory clean-up is ongoing with Inventory down from ~INR1.0bn to ~INR0.6bn, led by higher provisioning and early EOSS (GMs impacted by ~50bp), with a full store refresh targeted by 4Q to support FY27 recovery.

* Losses remain elevated but have likely peaked, with FY26 losses guided at ~INR0.6bn, declining to INR200–250m in FY27, and subsequently breaking even in FY28.

Highlights from the management commentary

* Demand trends: SHOP has seen weaker-than-anticipated discretionary demand in 3Q, impacted by early Diwali, post-festive demand taper, and pollution-led footfall disruptions, particularly in North India. While customer entry remained resilient, momentum was uneven through the quarter, resulting in flat LFL performance despite continued traction in premium categories.

* Store additions: SHOP undertook net store rationalisation in 3Q, with two net closures as the company prioritized portfolio clean-up and productivity over footprint expansion. Store additions remain calibrated, with near-term focus on replacing sub-scale stores with larger, more productive formats rather than accelerating net adds.

* INTUNE performance weakened sequentially, with growth moderating sharply due to legacy inventory overhang, lower freshness, and aggressive discounting. Store additions remained well below earlier guidance, as SHOP shifted focus decisively toward fixing supply chain, inventory quality, and in-store execution, with a full refresh targeted by end-4Q to support recovery in FY27.

Valuation and view

* SHOP stands to benefit from the recent measures taken by the government to boost consumption, which has led to improved footfalls in malls during the ongoing festive season.

* However, for sustained growth, SHOP would require: 1) profitability improvement in the Departmental format; 2) sustained high-growth in the margin-accretive Beauty segment; and 3) profitable ramp-up in INTUNE, which has so far proven challenging.

* We tweak our FY26-28E, while EBITDA remains broadly unchanged, as the slower ramp-up in INTUNE was partly offset by improved performance in departmental. We build in FY25-28E revenue/EBITDA CAGR of 6%/7%.

* We value SHOP at 20x Dec’27E Pre-IND AS EV/EBITDA to arrive at our revised TP of INR345. Reiterate Neutral.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041