Buy Lenskart Ltd for the Target Rs 650 by Motilal Oswal Financial Services Ltd

Stellar growth and margin expansion drive big beat

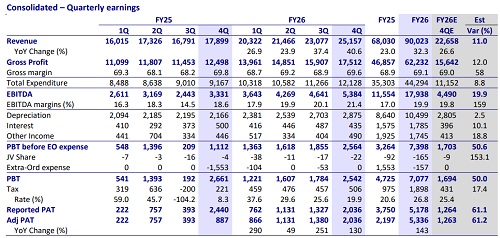

* Lenskart delivered a stellar 4QFY26, with consol. revenue rising ~41% YoY, (11% beat) driven by 25% YoY volume growth and ~12% YoY ASP increase (premiumization benefits, further aided by a low base in 4QFY25).

* 4QFY26 pre-IND AS EBITDA doubled YoY (34% beat), as margin expanded ~380bp YoY (+140bp QoQ) and came in ~220bp ahead of our estimate, driven by operating leverage benefits both in India and International.

* FY26 consolidated revenue grew ~32% YoY (vs. 23% YoY in FY25), led by volume growth (+30% YoY), acceleration in store additions (+22% YoY) and modest ~2% YoY ASP uptick. India/International grew 34%/30% YoY.

* FY26 pre-IND AS EBITDA grew 96% YoY to INR10.1b, as margin expanded ~370bp YoY, aided by 25bp product margin expansion and operating leverage on employee costs (140bp), other expenses (125bp) and rentals (~75bp). India/International witnessed 460bp/335bp margin expansion.

* Management believes Lenskart has entered a structural compounding phase, with incremental revenue translating into significantly higher EBITDA and PAT growth, aided by operating leverage across stores, supply chain and tech investments. The long-term margin target is ~25%.

* We raise our FY27E/FY28E revenue by 5%/6%, pre-IND AS EBITDA by ~15%/10% and PAT by ~12%/7%, driven by upgrades in India and International growth and margin assumptions.

* We now model a CAGR of 25%/42%/44% in revenue/pre-IND AS EBITDA/ PAT over FY26-28E, driven by 26%/23% revenue growth and 275bp/350bp margin expansion in India/International.

* We reiterate our BUY rating on Lenskart with a revised TP of INR650, premised on unchanged 55x FY28E pre-IND AS EBITDA.

India: 4Q growth accelerates to ~44% YoY; margin expands ~455bp in FY26

* Pro forma 4Q revenue stood at INR14.8b, with growth acceleration to ~44% YoY (vs. ~40% YoY in 3Q) and coming in ~11% ahead of our estimates.

* Volume grew ~24% YoY to 7.9m (+32% YoY in 3Q), while implied ASP rose ~16% YoY to INR1,867 (+7% YoY in 3Q, 6%), driven by premiumization and lower ASP in the base quarter due to the commencement of the lens replacement scheme.

* The company added 170 net stores during 4Q to reach 2,609 stores (up 26% YoY). It added 542 net stores in FY26 (vs. 282 YoY), with tier 2 cities accounting for 254 net additions (vs. 89 YoY).

* Gross profit grew 44% YoY to INR9.5b (+7% QoQ, 11% beat) as product margin was stable YoY at 64% (+30bp QoQ) despite headwinds from INR depreciation.

* Pro forma reported EBITDA doubled YoY to INR3.1b (+9% QoQ, 14% beat) as margin expanded ~575bp YoY to 21.2% (+40bp QoQ, ~70bp beat).

* Lease rentals grew ~30% YoY, resulting in pre-INDAS EBITDA growth of ~2.5x YoY to INR2.26b (21% beat), with margin expanding ~640bp YoY to 15.3% (+40bp QoQ, 135bp ahead of our estimate).

* India pro forma FY26 revenue grew ~34% YoY (vs. ~27% YoY in FY25), driven by 26%/6% YoY growth in volume/ASP.

* FY26 pre-IND AS EBITDA surged 96% YoY to INR7.6b as margins expanded 455bp YoY to 14.3%, driven by operating leverage on marketing spends (190bp), employee costs (110bp), other expenses (125bp) and rentals (~20bp).

Valuation and view

* Lenskart has built strong moats in a difficult-to-scale category through -

i) a centralized, highly automated manufacturing facility and logistics network

ii) strong backward integration, which provides significant cost advantage

iii) large omnichannel presence

iv) leveraging technology to ease constraints in scaling up

v) house-of-brands architecture spanning mass to premium eyewear, to achieve its goal of making quality eyewear accessible and affordable. Please refer our IC for detailed thesis on Lenskart.

* We raise our FY27E/FY28E revenue by 5%/6%, pre-IND AS EBITDA by ~15%/10% and PAT by ~12%/7%, driven by upgrades in India and International growth and margin assumptions.

* We now model a CAGR of 25%/42%/44% in revenue/pre-IND AS EBITDA/PAT over FY26-28E, driven by ~26%/23% revenue growth and ~275bp/350bp margin expansion in India/International.

* We reiterate our BUY rating on Lenskart with a revised TP of INR650, premised on unchanged 55x FY28E pre-IND AS EBITDA.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412