Buy JSW Infrastructure Ltd for the Target Rs. 360 by Motilal Oswal Financial Services Ltd

In-line 2Q; outlook bright with expansion projects underway

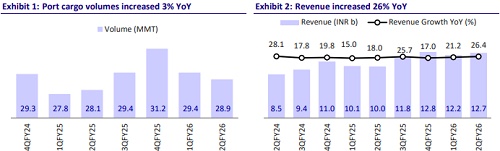

* JSW Infrastructure (JSWINFRA)’s consolidated revenue grew 26% YoY to INR12.6b (in line). During 2QFY26, the company handled cargo volumes of 28.9m tons (+3% YoY). The volume growth was impacted due to subdued performance in the Paradip iron ore terminal. Weak volume was offset by growth in the Southwest, Jaigarh, and Dharamtar ports. Interim operations at the Tuticorin Terminal and JNPA Liquid Terminal also supported growth.

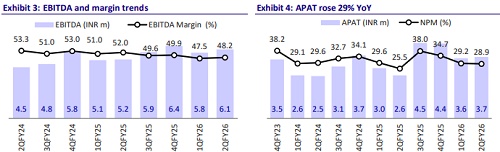

* EBITDA grew 17% YoY to INR6.1b (in line). EBITDA margin stood at 48.2% (vs. our estimate of 50.4%). The margin was lower by ~380bp YoY and ~70bp QoQ. JSWINFRA’s APAT grew ~39% YoY to INR3.6b (in line).

* Port revenue grew 10% YoY to INR11b. The logistics segment recorded a revenue of INR1.6b for the quarter.

* JSWINFRA posted a muted volume growth in 2QFY26, hit by a dip in iron ore volume at the Paradip iron ore terminal. The price of iron ore impacted the movement of commodities across key ports in India, which hurt volumes. The situation is normalizing, and volumes are likely to be much better from 3QFY26.

* The company is executing multiple expansion projects across ports and logistics, with INR55b capex planned in FY26. Backed by a strong balance sheet and rising cargo diversity, JSWINFRA aims to scale port capacity to 400MTPA and logistics revenue to INR80b by FY30, positioning it well for longterm growth. We broadly retain our FY26 and FY27 estimates. We estimate a volume/revenue/EBITDA/APAT CAGR of 15%/24%/26%/23% over FY25-28. Reiterate BUY with a TP of INR360 (premised on 17x FY28 EV/EBITDA).

Cargo volumes up 3% YoY, hit by low iron ore volumes; a strong balance sheet to support capex in the ports and logistics businesses

* JSWINFRA posted subdued cargo volumes of 28.9MT in 2QFY26, up 3% YoY, due to poor performance in the Paradip iron ore terminal, partially offset by better performance in the Southwest, Jaigarh, and Dharamtar ports.

* The port business contributed INR11b in revenue (+10% YoY), while the logistics segment recorded INR1.6b. Third-party cargo volumes decline 1.5% YoY, with contribution declining to 46% in 2Q FY26 (vs. 48% in 2Q FY25), reflecting a change in cargo mix primarily due to the volume impact in the Paradip iron ore terminal.

* Navkar delivered strong growth, with EXIM container volumes rising 22% YoY and domestic cargo growing 45% YoY.

* The company maintains a healthy balance sheet with net debt at INR18.1b and cash and equivalents of INR30.88b as of Sep’25, supporting its expansive capex program.

Highlights from the management commentary

* JSWINFRA expects volatility in iron ore volume to stabilize going forward, which should support the volume growth ahead.

* For FY26, management expects a volume growth of 8-10% despite the slow growth in 1HFY26. ? Management expects the interim operation to start in the Kolkata Container terminal by the end of FY26.

* The company is aggressively scaling its logistics footprint through an asset-light model, targeting pan-India multimodal integration. Management maintains its guidance of the logistics segment to generate INR7–8b in revenue and ~INR1b in EBITDA in FY26, aided by synergies from Navkar and operational ramp-up of the recently added infrastructure.

* JSWINFRA is executing multiple brownfield and greenfield expansion projects, including the Kolkata Container Terminal (6.3MTPA), Tuticorin (7MTPA), and JNPA Liquid Terminal (4.5MTPA), with completion timelines over FY26–28. Strategic capacity upgrades are ongoing at Mangalore, Southwest Port, Dharamtar, and Jaigarh, with a combined expansion of over 40MTPA. Landmark greenfield projects such as the Keni Port (30MTPA), Jatadhar Port (30MTPA), and a 302km slurry pipeline in Odisha are progressing well, all scheduled for commissioning by FY28–30.

* Execution continues to be on track across major port and logistics infrastructure projects, with the recent acquisition of an 86-acre brownfield rail siding in Kudathini, Ballari (Karnataka), which is being transformed into MMLP, further strengthening its multimodal logistics play. The total planned capex continues to be at INR55b for FY26 (INR40b for ports and INR15b for logistics).

Valuation and view

* Management expects its FY26 cargo volume growth guidance to be ~8-10%, with stronger traction in 2HFY26. Long-term vision includes expanding port capacity to 400MTPA by FY30 and building a logistics platform delivering INR80b in revenue and a 25% EBITDA margin. Backed by aggressive yet disciplined capex, customer diversification, and multimodal infrastructure expansion, JSWINFRA remains well-positioned for structural growth across India’s maritime and logistics value chain.

* We expect JSWINFRA to strengthen its market dominance, leading to a 15% volume CAGR over FY25-28. This, along with a sharp rise in logistics revenues, is expected to drive a 24% CAGR in revenue and a 26% CAGR in EBITDA over the same period. We reiterate our BUY rating on the stock with a TP of INR360 (based on 17x FY28 EV/EBITDA).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412