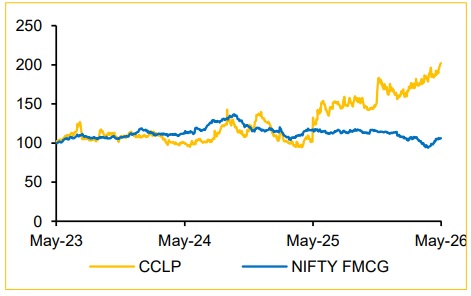

Buy CCL Products India Ltd for the Target Rs. 620 by Choice Institutional Equities

Absolute EBITDA/kg Remains Intact

Q4FY26 revenue came in ahead of expectations, while margins were impacted due to elevated coffee prices and a higher share of relatively low margin coffee contracts. However, the key operating metric — EBITDA/kg — remained strong at INR 138/kg (FY26 average: INR 135/kg). This reflects the company’s ongoing improvement in product mix, driven by a higher contribution from premium Freeze Dried Coffee (FDC) and increasing salience of small-pack consumer offerings over the years. Following the sharp increase in coffee prices during CY25, recent stabilisation (down ~17% YTD) is positive, enabling longer duration contracts, lower working capital needs and better demand visibility.

Branded Business (Continental Coffee) – Emerging as a Value Driver

Branded business reported strong momentum in FY26, with revenue increasing from INR 3.0 Bn in FY25 to INR 4.4 Bn in FY26, reflecting robust 47% YoY growth. The growth was driven by rapid distribution expansion to ~1.4 lakh outlets, along with a strong presence across quick commerce and e-commerce platforms. Continental Coffee has now emerged as the No. 3 instant coffee brand in India. Management expects the branded business to sustain healthy momentum, with revenue growth guidance of 20–25% in the near term.

Valuation:

We value the company using the DCF approach, having a target price of INR 1,365, with a 21% upside and a BUY rating. We have marginally increased our FY28 estimates to account for better capacity utilisation. This equates to an implied PE of 27x on FY28 EPS (Base case – we have assumed CAGR 14%/18%/26% Revenue/EBITDA/PAT over FY26-29E).

Q4FY26 Result: Higher Raw Material Cost Weigh on Margins; Absolute Profitability Remains Intact

* Volume was up 18% YoY and realisation was up 25% YoY. EBITDA/kg remained healthy at INR 138/kg.

* Revenue was up 46.5% YoY and up 16.6% QoQ to INR 1,224 Mn (vs CIE est. at INR 1,134 Mn).

* EBITDA was up 17.5% YoY and down 0.7% QoQ to INR 192 Mn (vs CIE est. at INR 203 Mn). EBITDA margin was down 387 bps YoY and 208 QoQ to 15.7% (vs CIE est. at 17.9%). EBITDA margin declined on account of subdued gross margin performance on the back of higher raw material cost, up 71% YoY and higher share of low margin coffee contract.

* Adj. PAT was up 12.4% YoY and down 8.4% QoQ to INR 115 Mn (vs CIE est. at INR 110 Mn).

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131