Buy CCL Products (India) Limited for Target Rs. 1,350 by Choice Institutional Equities

Improved Product Mix and Stable Coffee Price to Drive Profitability

CCLP has shifted its product mix towards premium offering through Freeze Dried Coffee (FDC) and increase salience of small packs (LUPs). FDC delivers 30–40% EBITDA/kg higher than Spray Dried Coffee (SDC), while small packs (LUPs) add further premiumisation. Though premium products form only 5–10% of volumes, they contribute 10–15% of value. As a result, EBITDA/kg has improved, from INR 90–100 (FY20) to INR 135–140 (Q3 FY26), which is further expected to increase, going forward, driven by higher FDC utilization and growth in small packs.

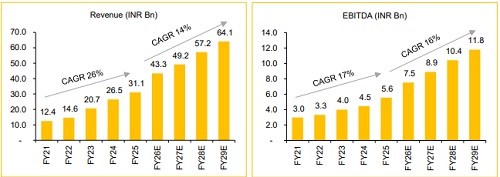

Post elevated coffee prices in FY25, recent stabilization in coffee prices (down ~13%/33% YTD and YoY) is positive enabling longer contracts, lower working capital needs and better demand visibility. This underpins 17–18% EBITDA margin and 16% EBITDA CAGR over FY26–29E.

Branded Coffee – Emerging as a Value Driver

Driven by rapid distribution expansion to 1.4 lakh outlets and strong presence across quick-commerce and e-commerce. Continental Coffee has emerged as the No. 3 instant coffee brand in South India, with revenue growing to INR 3.0 Bn in FY25 and expected to reach INR 4.3–4.4 Bn in FY26E (40–50% growth). Over the medium term, the management targets INR 5 Bn revenue, 30–35% growth, and double-digit EBITDA margin (vs. 5–8% at present), supported by operating leverage and premiumisation. The relaunch of Percol and Rocket Fuel in the UK is gaining traction, with FY26 revenue expected to increase t0 INR 300-320 Mn (2x) from INR 150–160 Mn in FY25.

Post-capex Phase: Utilization led Growth with Improving Financial Metrics

Driven by capacity expansion in Vietnam (FDC) and India (SDC), CCLP has nearly doubled its capacity, from ~38,500 MTA (FY22) to ~77,000 MTA (FY26E). With the capex cycle largely complete, the company has strong headroom for near-term growth. Vietnam adds structural advantages – zero income tax, lower interest costs, and proximity to Robusta sourcing–with its 16,500 MTA SDC capacity ramped up, while the new FDC facility supports product mix improvement.

Further, stable coffee prices (easing working capital) and post-capex cash flow recovery are expected to restore FCF, enabling debt reduction of INR 1.5–2 Bn per quarter after four years of negative FCF.

Valuation and View: The company offers a compelling medium-term growth story, driven by premiumisation (FDC, small packs, B2C) and capacity ramp-up post 2x expansion. This supports EBITDA/PAT CAGR of 16%/24% (FY26–29E), aided by stable coffee prices and improving product mix. With the capex cycle largely complete, FCF recovery and deleveraging are expected to drive ROE expansion to ~20–21% by FY29. We initiate CCLP with a BUY rating and a one–year DCF-based target price of INR 1,315 per share implying an upside of 20% upside from the existing level, supported by a reasonable ~27x FY28E P/E (Implied

Upside Trigger: Faster utilization and decline in coffee prices.

Key Risks: Possible increase in coffee prices, Geo-politics & tariff risk negatively impacting overall supply chain and slower capacity utilization.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131