Buy Apollo Hospital Ltd for the Target Rs.9,015 by Motilal Oswal Financial Services Ltd

Hospital engine strong; HealthCo inflection in sight

We recently met with the management of Apollo Hospital (APHS) to gain deeper insights into the company’s business prospects.

The key takeaways are as follows:

* APHS has implemented efforts to gear up for the next phase of growth in the hospital segment through: a) a sustained shift toward higher-complex case mix and b) a disciplined greenfield/brownfield expansion plan, with 45% (~3,660) beds to be added over the next five years in a phased manner.

* In HealthCo, APHS is progressing well on: a) expanding offerings on its online platform, b) optimizing costs, c) adding physical stores, and d) improving storelevel productivity. Notably, it is on track to achieve EBITDA break-even in Apollo 24/7 by 4QFY26.

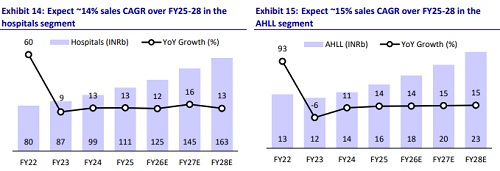

* The AHLL segment is transitioning into a diagnostics-led growth platform, with specialty and day-care integration expected to drive sustained high-teen revenue growth and mid-teen EBITDA margins beyond FY27.

* Overall, we remain positive on APHS, expecting a 14%/17%/24% CAGR in revenue/EBITDA/PAT over FY25-28. We value APHS on an SoTP basis (30x EV/EBITDA for the hospital business, 20x EV/EBITDA for retained pharmacy, 23x EV/EBITDA for AHLL, 25x EV/EBITDA for front-end pharmacy, and 2x EV/sales for Apollo 24/7) to arrive at a TP of INR9,015. Reiterate BUY

Hospital: Case mix upgrade/capacity addition to drive growth

* Hospital remains a key contributor, accounting for ~50%/83% of revenue/EBITDA; the segment delivered a strong 10% YoY revenue growth in 1HFY26 with EBITDA margin expansion of ~24.6% YoY.

* While the current occupancy level is at ~65-67%, the company indicated that it is focusing on optimizing the case mix/ALOS to further strengthen EBITDA.

* Specifically, day care services for local patients across certain indications are enabling the company to reduce ALOS and treat a higher number of patients.

* Compared to a 13-14% oncology share in the case mix three years ago, APHS’s efforts have increased it to 17% currently. Likewise, management indicated an enhanced focus on CNS indications. APHS’s objective is to further increase the share of CONGO (cardiology, oncology, neuroscience, gastro, orthopedics) to drive profitable revenue growth in the hospital segment.

* Over the last three years, the company has onboarded ~180 doctors across new and existing hospitals, strengthening specialty depth and supporting complex case additions.

* Management indicated temporary headwinds in the Eastern cluster due to the transfer of a doctor team from the Bhubaneshwar hospital. APHS has since revived team strength and, accordingly, expects performance to improve going forward.

* In the North cluster, growth remains constrained by bed capacity. APHS is in the process of resolving this through greenfield expansions in Gurgaon, Lucknow, and Varanasi.

* Limited bed capacity in Indore has restricted the addition of doctors.

* Overall, APHS has outlined a plan to add 3,660 beds over the next five years at a total project cost of ~INR83b, of which INR58b remains to be spent.

* Considering: a) improving efficiency in existing hospitals and b) the addition of new hospitals, the hospital business has the potential to deliver 10-15% YoY EBITDA growth in FY27. Opex losses from new hospitals would be INR500m/INR1.5b in 2HFY26/FY27, according to management.

HealthCo: Increased online offerings/store addition to support strong EBITDA growth

* While the HealthCo segment’s contribution is limited (42%/11% of revenue/EBITDA), it is the highest EBITDA-growing segment for APHS.

* Management emphasized that HealthCo is transitioning from a predominantly pharmacy-led revenue model to a multi-vertical healthcare services platform. The strategic play includes: 1) locking in recurring interactions and higher lifetime value through condition-management programs (diabetes, cardiac, and neuro), 2) capturing growth in preventive health-check spend, and 3) expanding home-care and doctor-led outreach to deepen engagement and stickiness.

* The current business is pharmacy-heavy, with ~65% of revenue derived from pharma and the balance from consulting and IP/OP services. Management is actively focused on diversifying revenue through the monetization of consulting services, OPD offerings, and insurance commissions, thereby diversifying and adding new growth drivers.

* APHS has guided for 15% YoY GMV growth, backed by 16-17% YoY growth in the pharmacy segment and the scale-up of new offerings.

* The focus is on significantly improving growth prospects in online pharmacy, while continuing efforts on cost optimization.

* Even on the offline pharmacy side, APHS is on track to: a) add 400-500 stores, b) improve revenue per store.

* Management showcased confidence in achieving EBITDA break-even in its online pharmacy and distribution businesses in 4QFY26.

* Subsequently, the FY27 outlook remains promising, with an 18-20% YoY growth expected in the offline pharmacy business and EBITDA contribution from the online pharmacy business

Diagnostics/speciality integration to drive growth engine

* The AHLL segment remains a small but improving contributor, accounting for ~7.5% of consolidated revenue; the segment delivered a strong 18% YoY revenue growth, with EBITDA margins gradually expanding to ~10% YoY in 1HFY26.

* APHS is working on two main aspects in this segment: a) scale up the diagnostics business and b) integrate day-surgery centers with APHS Group hospitals.

* APHS intends to add three reference labs over the next 12-18M, in addition to expanding its collection centers in the diagnostics space.

* APHS appointed a new CEO to strengthen growth prospects in the diagnostics segment.

* Integrating day-surgery centers is expected to enhance EBITDA margins of specialty care within AHLL from 11% (currently) to ~20% over the next 12-18M.

* Recently, the Competition Commission of India has accorded its approval for AHPS’s acquisition of 30.58% equity stake in AHLL from International Finance Corporation, Washington (IFC) and IFC EAF Apollo Investment Company (IFC EAF), for a purchase consideration of INR12.5b.

Valuation and view

* We value APHS on an SoTP basis (30x EV/EBITDA for the hospital business, 20x EV/EBITDA for retained pharmacy, 23x EV/EBITDA for AHLL, 25x EV/EBITDA for front-end pharmacy, and 2x EV/sales for Apollo 24/7) to arrive at a TP of INR9,015.

* APHS continues to build comprehensive healthcare services through hospitals, pharmacies (offline/online), diagnostics, and specialty clinics.

* While APHS remains the largest healthcare service provider on a national level, it is implementing efforts to expand across focus areas of super-specialty hospitals and improve the revenue/operating profit prospects of HealthCo.

* Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041