Buy SBI Life Insurance Company Ltd For Target Rs.2,200 by Prabhudas Liladhar Capital Ltd

Healthy growth and margin outlook

Quick Pointers

* Q4 APE grew 5% YoY; margin in-line with expectation

* Expect ~13% APE growth in FY27E

* FY26 VNB margin stood at 27.5%; expect gradual improvement as the product mix improves

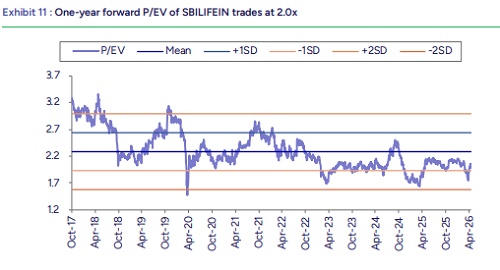

Q4FY26 APE grew 5% YoY led by a pick-up in PAR/Annuity and retail protection. On FY26 basis, SBI Life has grown 13% YoY; we build a similar run-rate over FY27-FY28E, in-line with the guidance. Q4/FY26 VNB margin contracted to 28.4%/27.5% impacted by GST exemption. We build a gradual improvement to 27.6%/ 27.7% for FY27/FY28E as the drag from GST exemption neutralizes and the company diversifies away from ULIP. We roll forward to FY28E with a multiple of 2.0x (vs. 2.5x earlier) and value SBILIFEIN using the Appraisal Value framework with a TP of INR 2,200. Upgrade to ‘BUY’ on healthy APE growth and margin outlook over FY26-28E.

* Expect 13% APE CAGR over FY26-28E: Q4 APE grew 5% YoY to INR 57.4bn driven by a sustained momentum in retail protection (+30% YoY). Commentary indicated positive tailwinds from GST reform and a shift toward higher sum assured/ pure term products aided growth. Credit life APE grew 14% YoY driven by increased attachment rates in the HL portfolio. While PAR and Annuity segment grew +194%/+33% YoY on a small base, ULIP remained largely flat. While Feb/ Mar-26 have seen decent growth in ULIP, commentary highlighted a small impact of the Gulf War-related volatility on NPAR (-9.4% YoY). ULIP/ PAR/ NPAR/ Protection/ Annuity/ Group Savings comprised 52.1%/8.7%/20.2%/10.1%/3.5%/5.4% of APE mix in Q4FY26. FY26 APE has grown 13% YoY driven by new product launches and the company has guided for an APE CAGR of ~14% over FY26-28E. We build an APE CAGR of 13% over FY26-28E, driven by sustained growth in protection/ PAR and annuity.

* Expect gradual improvement in margin over FY26-28E: Q4 VNB saw a slight decline of 1.8% YoY to INR 16.3bn, while VNB margin stood at 28.4%. Commentary indicated the impact of GST is likely to be absorbed by H1FY27 supported by enhancement of product profile (higher share of protection) and rider attachments to the ULIP portfolio. FY26 VNB grew by 12% to INR 66.7bn while margin stood at 27.5%, and the company expects to maintain in the current range of 26%-28%. We build a gradual improvement of 10/10 bps to 27.6%/ 27.7% VNB margin for FY27/ FY28E, as the impact of GST exemption neutralizes.

* Agency contribution to increase; focus on direct channel: Banca/Agency/Others contributed to 52.3%/34.7%/13.1% of Q4FY26 APE. Banca witnessed a de-growth of ~4% YoY due to sluggish volumes; expect growth to pick up in subsequent quarters. While there is no concrete guideline from the regulator on open architecture, company remains confident to navigate regulatory challenges. Agency channel grew 28% YoY driven by agent additions (+24% YoY) and improved productivity. While the channel contributes ~29% of the APE mix (in FY26), company expects the share to improve by ~3-4% over the next 2-3 years. Commentary highlighted continued investment in the direct channel with the company adding 120 new branches in FY26 to strengthen its offline presence.

* EV grows 15% YoY; cost ratio increases due to one-offs: Embedded value grew 15% YoY to INR 808bn with positive operating variance recorded majorly due to better mortality and persistency experience. While 61M persistency dropped to 58.1% (vs. 63.6% in FY25), it was largely due to a Covid cohort; others saw improvement (13M/25M/37M/49M at 87.9%/78.0%/72.3%/69.1%). Total cost ratio increased to 10.6% in FY26 (vs. 9.7% in FY25) due to (1) one-offs such as GST exemption and labour-code regulation and (2) higher opex on branch expansion/ manpower/ training etc. AUM grew 9% YoY to INR 4,871.6bn. Solvency ratio was lower at 190% (vs. 196% in FY25) due to underwriting a higher share of protection business. However, the company expects it to remain in a similar range and does not foresee the need for additional capital.

Please refer disclaimer at https://www.plindia.com/disclaimer/

SEBI Registration No. INH000000271

.jpg)