Buy Delhivery Ltd for the Target Rs 580 by Motilal Oswal Financial Services Ltd

In-line performance; strong transportation volume and margin expansion drive earnings

Strong show across Express and PTL segments

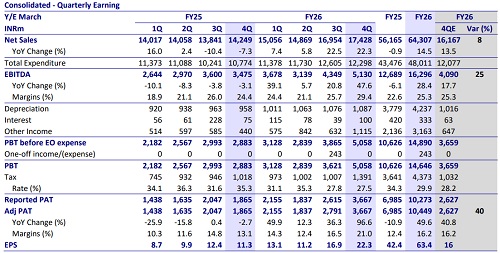

* Delhivery reported a 30% YoY increase in revenue to INR28.5b in 4QFY26 (in line). Reported EBITDA rose 80% YoY to ~INR2.1b, while EBITDA margins stood at 7.5%, up 210bp YoY and 10bp QoQ.

* APAT came in at INR708m (-2.5% YoY) against our estimate of INR774m.

* Core transportation segment, comprising Express Parcel and Part Truckload (PTL) segments, saw robust volume growth (Express Parcel: +73% YoY and PTL: +20% YoY). Service EBITDA margins for Express Parcel/PTL stood at 18.8%/13.4%.

* Delhivery delivered a strong 4QFY26 performance, aided by strong consumption-led demand, integration of Ecom Express, and market share gains driven by industry consolidation. Management expects to sustain the strong momentum in Express business and PTL going forward. New services such as Delhivery Direct and Rapid are scaling up well. We maintain our FY27 and FY28 EBITDA estimates, factoring in strong growth in the transportation segment, supported by healthy service EBITDA margins. We expect Delhivery to deliver a CAGR of 13%/33% in revenue/EBITDA over FY26-28. We reiterate our BUY rating with a DCF-based TP of INR580.

Strong core transportation businesses drive profit-accretive growth

* Express Parcel revenue grew 46% YoY to INR18.3b, with shipments rising 73% YoY to 306m after the integration of Ecom Express. The segment saw healthy service EBITDA margin of 18.8%, up 290bp YoY and 70bp QoQ.

* PTL revenue grew ~20% YoY to INR6.2b, with tonnage increasing 20% YoY to 0.549MT. Service EBITDA margin stood at 13.5%, up 240bp QoQ and 270bp YoY, supported by improved yields and a favorable client mix.

* The combined transportation business (Express + PTL) reported a healthy service EBITDA margin of 17.5% in 4Q, supported by strong volume-led operating leverage, improved route optimization, and steady investments in a high-capacity fleet and integrated gateways.

* The company expects volume growth of ~15-20% annually over the next few years across segments.

Valuation and view

* Delhivery is well positioned for future growth, supported by strong momentum in its core transportation businesses and a clear focus on profitability. With Express Parcel and PTL segments delivering strong volume growth and healthy service EBITDA margins, the company expects to sustain 16-18% margins over the next two years.

* The integration of Ecom Express is set to enhance network efficiency and reduce capital intensity, while new services like Delhivery Direct and Rapid offer longterm growth potential in on-demand and time-sensitive logistics.

* We expect Delhivery to deliver a CAGR of 13%/33% in revenue/EBITDA over FY26-28E. We reiterate our BUY rating with a revised DCF-based TP of INR580.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412