Buy Zensar Tech Ltd for Target Rs. 650 by Choice Institutional Equities

Key Conference Call Highlights

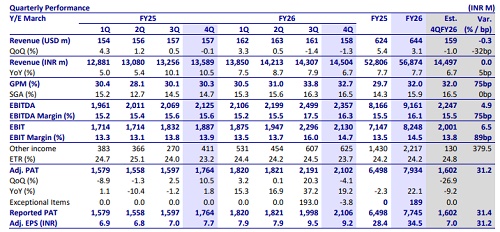

Segment Performance

* BFS: This is the strongest performer, expanding 1.2% QoQ in Q4. The vertical is expected to continue growing in the near term.

* HLS: The segment faced pressure in Q4 with a de-growth of 6.6% QoQ due to being consolidated out of a couple of accounts; the management expects this vertical to remain flat in FY27E.

* Manufacturing and Consumer Services: Recorded a decline of 3.9% QoQ. The management expects some growth here in the coming year.

* TMT: Faced significant stress, declining 9.7% for the full year. This decline was attributed to major tech clients cutting costs and adopting in-sourcing paradigms. The management projects continued pressure in TMT for the next few quarters.

* Service Line Highlights: The share of revenue from specialised service lines increased to 71.6% in Q4. Leading growth areas included Cloud Infrastructure and Security (13%) and Data Engineering and Analytics (8%).

Geographical Performance

* Europe and South Africa: The management stated it has righted the ship in these regions and expects to see good growth, going forward.

* Expansion: The company opened a new delivery center in Belgrade, Serbia, to leverage high-quality talent and provide nearshore benefits to clients.

Margin Trajectory

* Q4 Margin: EBITDA margin contracted by 130 bps sequentially due to lower working days (-0.3%), the reversal of a one-time leave utilisation benefit (- 1.1%), and initial costs related to mega deal implementation and SG&A (- 1.1%), which were partially offset by forex gains (+1.2%).

* Guidance: The management intends to maintain margin in the mid-teens (14% to 16%) for FY27E. They noted that while transition costs for new large deals will create pressure in Q1 and Q2, they will prioritise growth over immediate margin expansion if necessary.

Outlook & Guidance

* The company entered FY27 with its strongest-ever order book, totalling USD 401.8 Mn in Q4, a sequential increase of 122.9%.

* Mega Deal Win: The record order book was driven by a USD-210 Mn mega deal. Revenue from this deal is expected to start in Q1 FY27, with a full rampup anticipated by Q3 FY27.

* Growth Outlook: The management does not foresee a de-growth scenario for Q1 FY27 and expects overall performance to be contingent on the successful execution of the new mega deal.

AI Initiatives

* Workforce Readiness: 85% of the workforce is now AI-certified. AI learning hours per person increased by 136% in FY26 as compared to the previous year.

* AI-Native Offering: The company launched several refined AI-led solutions, including an Agentic Foundry for BFSI clients and Quality Intelligence (QI), which focuses on testing against user intent rather than just functional specs.

* Internal Adoption: The company acts as its own role model for AI adoption. Recruitment is now completely AI-enabled, and AI is used in finance for accounts receivable/payable and in legal for shortening contract processing times.

* Market Strategy: The management is using AI to expand its addressable market, specifically targeting traditional BPO business by proposing models where AI agents perform high-volume work traditionally done by people.

For Detailed Report With Disclaimer Visit. https://choicebroking.in/disclaimer

SEBI Registration no.: INZ 000160131