Buy Tata Steel Ltd for the Target Rs 250 by Motilal Oswal Financial Services Ltd

In-line earnings; high steel prices boosts outlook Standalone performance broadly in line

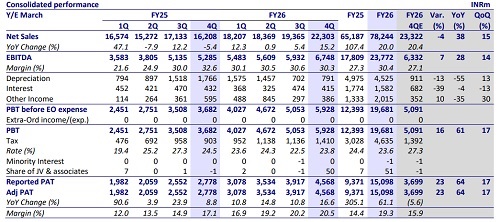

* Tata Steel’s (TATA) standalone revenue stood at INR385b (+12% YoY and +8% QoQ) in 4QFY26, in line with our estimate. The growth was largely driven by better domestic volumes and strong NSR recovery.

* Steel production stood at 5.97mt (+14% YoY and flat QoQ), whereas deliveries were in line with our est. at 6.2mt, up 11% YoY and 2% QoQ.

* ASP improved by 5% sequentially to INR62,113/t in 4QFY26 (+1% YoY), driven by strong steel price recovery led by safeguard duty.

* EBITDA stood at INR94.7b (+36% YoY and +23% QoQ), in line with our estimate, translating to EBITDA/t of INR15,300/t (+23% YoY and +20% QoQ) in 4QFY26 as the input cost inflation, led by higher coking coal consumption cost, was fully offset by strong NSR.

* APAT stood at INR48b (+29% YoY and +15% QoQ), in line with our estimate.

* In FY26, revenue grew 5% YoY to INR1,397b, aided by volume growth of 8% YoY to 22.5mt. This was partially offset by muted NSR of 2% YoY.

* EBITDA stood at INR325b (+17% YoY), translating to EBITDA/t of INR14,413 (+8% YoY), whereas APAT stood at INR172b, up 15% YoY in FY26.

Europe EBITDA turns positive in 4Q

* Combined Europe’s revenue stood at INR228b (+10% YoY and +17% QoQ) during the quarter, primarily driven by healthy NSR YoY and better volume QoQ.

* Combined steel deliveries stood at 2.2mt (-7% YoY and +16% QoQ), in line with our estimate, while ASP stood at USD1,123/t (+11% YoY and -2% QoQ).

* EBITDA was positive during the quarter at INR320m (in line with est.) against EBITDA loss of INR7.5b in 4QFY25 and INR1.7b in 3QFY26.

* This translates to EBITDA/t of USD2/t in 4QFY26 against EBITDA/t loss of USD36/t in 4QFY25 and USD10/t in 3QFY26.

Valuation and view: Long-term outlook remains strong

* Overall, TATA posted a strong performance in 4QFY26 as anticipated, primarily driven by healthy volume and NSR in India business. Combined Europe’s EBITDA continues to hover near its breakeven due to operational challenges; however, improving prices will support the margin.

* EBITDA improvement is expected for Europe’s operations in the coming quarters on account of ongoing cost-restructuring measures and improving prices, along with regulatory measures (CABM/reduction in import quotas) to support domestic business. The capacity ramp-up in the Netherlands and lower fixed costs should incrementally drive the overall EBITDA performance going forward.

* Though there are near-term uncertainties related to price volatility and emission challenges in Europe, the long-term outlook remains strong for TATA. We maintain our FY27/28 earnings estimates, considering better volume and an improved pricing environment.

* At CMP, TATA is trading at 7.1x EV/EBITDA and 2x P/BV on FY28E. We reiterate our BUY rating with an SOTP-based TP of INR250 on FY28E EPS.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)