Buy DCB Bank Ltd for the Target Rs. 235 by Motilal Oswal Financial Services Ltd

Steady quarter; on track for 1% RoA in FY27E

Asset quality healthy; NIMs expand 12bp QoQ

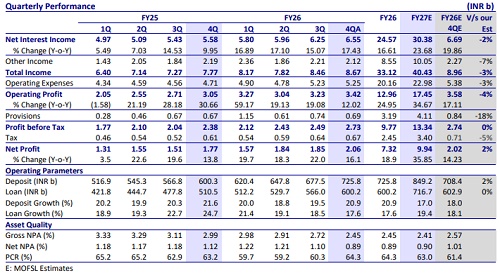

* DCB Bank (DCBB) reported 16.1% YoY growth in PAT at INR2.06b (broadly in line), aided by lower provisions and lower tax rate.

* NII grew 17% YoY to INR6.5b (inline, up 5% QoQ). NIMs expanded 12bp QoQ to 3.39% in 4QFY26, driven by lower funding cost and better loan mix.

* Other income declined ~3% YoY/declined 4.5% QoQ to INR2.1b (7% lower vs MOFSLe), amid muted treasury gains. Opex grew ~11% YoY (flat QoQ) to INR5.2b. PPoP stood at INR3.4b (up ~12% YoY/6% QoQ; broadly in line).

* Business growth remained healthy with advances growth of 17.6% YoY/6% QoQ, while deposits grew 20.9% YoY/7.1% QoQ. CASA mix stood at 22.4%.

* GNPA/NNPA ratios improved to 2.45%/0.89% (down 27bp/21bp QoQ), while PCR increased to ~64%. Slippage ratio declined to 2.3% vs 3.1% in 3QFY26.

* We largely maintain our earnings and estimate FY27E RoA/RoE of 1.01%/15.1%. Reiterate BUY with a TP of INR235 (based on 1.0x Sep’27E ABV).

Business growth robust; slippage declines 21% QoQ

* DCBB reported PAT of INR2.06b (up ~16% YoY/ ~11% QoQ; largely in line), aided by lower-than-expected provisions and lower tax rate.

* NII grew 17% YoY/4.9% QoQ to INR6.5b (up 5% QoQ, largely in line). NIMs expanded 12bp QoQ to 3.39% in 4QFY26, supported by lower funding cost and improving mix. Other income declined 3% YoY/4.5% QoQ to INR2.1b (7% lower vs MOFSLe).

* Opex grew 11.3% YoY/flat QoQ to INR5.2b (largely in line). PPoP, thus, grew 12% YoY/6% QoQ to INR3.4b (broadly in line).

* Provisions were lower at INR690m (up 2.6% YoY/ down 7% QoQ, 18% lower vs MOFSLe). PBT grew to INR2.73b (15% YoY/10% QoQ, largely in line).

* Advances grew 18% YoY/6% QoQ, led by gold, agri, as well as corporate book. While mortgage book grew slower at 5% YoY/ 2.9% QoQ, co-lending book declined by 7% QoQ.

* Deposits grew robust at 21% YoY/ 7% QoQ, while CASA deposits grew slow at 10.4% YoY/ 5.3% QoQ. As a result, CASA ratio declined to 22.4% vs 22.8% in 3QFY26. DCBB’s CD ratio declined by 84bp QoQ to 82.7%.

* Fresh slippages moderated by 21% QoQ, with annualized slippage ratio declining to 2.3% vs 3.1% in 3QFY26. GNPA/NNPA ratios improved to 2.45%/0.89% (down 27bp/21bp QoQ), while PCR increased to ~64%.

Highlights from the management commentary

* The bank remains confident of sustaining 18-20% growth in advances and deposits over the medium term.

* RoA trajectory remains toward 1%+ as margins, asset quality, and productivity improve.

* The bank expects deposit repricing benefit to continue till late 2QFY27/early 3QFY27.

* Priority remains liability quality and pricing discipline rather than chasing high-cost deposits.

Valuation and view

DCBB reported an in-line performance, with both NII and PAT meeting expectations, while lower-than-expected provisions offset weaker other income. Margins improved by 12bp QoQ, and management expects further expansion driven by an improving asset mix and a decline in the cost of deposits, which is likely to continue until 2QFY27. Business growth remained healthy, supported by an increased focus on higher-yielding segments such as business loans and gold loans. Asset quality improved, with a decline in slippages leading to lower provisions. The bank expects growth to remain robust, guiding for asset growth of 18–20%, along with a RoA target of ~1%, supported by better NIMs, improving asset quality, and enhanced operating efficiency. We largely maintain our estimates for FY27 and project an FY27E RoA/RoE of 1.01%/15.1%. Reiterate BUY with a TP of INR235 (based on 1.0x Sep’27E ABV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412