Neutral IDFC First Bank Ltd for the Target Rs. 75 by Motilal Oswal Financial Services Ltd

Tepid quarter marred by one-offs

NIM improves 17bp QoQ; elevated provisioning dents performance

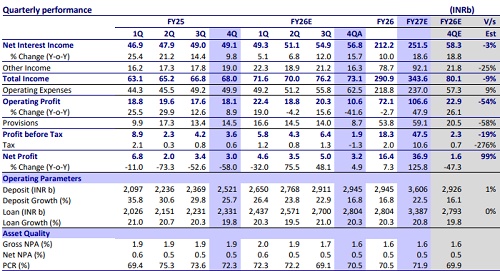

* IDFC First Bank (IDFCFB) reported a 4QFY26 PAT of INR3.19b (up 4.9% YoY/down 37% QoQ). This represented a 99% beat to MOFSLe amid a tax reversal of INR1.7b on account of a favorable tax order.

* The bank reported a treasury loss of INR1.6b, while also realizing a loss of INR2.7b in other income along with a corresponding release in provisions. The bank has also reported a loss of INR6.5b, owing to a deposit fraud in the Chandigarh branch.

* NII grew 15.7% YoY/3.4% QoQ to INR56.7b (inline). NIM expanded 17bp QoQ to 5.93%.

* Business growth remained robust, with advances growth at 20% YoY/4% QoQ. Deposit growth, though, was flat, affected by the noise around the deposit fraud incident. The CASA mix moderated to 49.8% (-180bp QoQ).

* GNPA ratio improved 8bp to 1.61%, while the NNPA improved by 5bp QoQ to 0.48%. PCR improved 139bp QoQ to 70.5%.

* We slightly lower our FY27/28E earnings by 1%/4% respectively and estimate an RoA/RoE of 0.8%/7.6% for FY27. Reiterate Neutral with a TP of INR75 (premised on 1.2x Sep’27E ABV).

Guides FY27E NIM to be similar to FY26; asset quality outlook better

* IDFC First Bank (IDFCFB) reported a 4QFY26 PAT of INR3.19b, hit by fraud-related provisioning and treasury loss, partly offset by tax reversals.

* NII grew 15.7% YoY/3.4% QoQ to INR56.8b (inline). Its NIM stood at 5.93% in 4QFY26 (vs. our estimate of 5.84%). The bank guides FY27 NIM to remain broadly stable at FY26 levels.

* Other income declined 14% YoY/ 23% QoQ, amid flat fee income and treasury loss of INR159m, while the bank also realized a loss of INR2.7b amid stressed power accounts (provision reversal of INR2.7b).

* Reported opex stood at INR62.5b in 4QFY26, including the fraud impact of INR6.46b. Adjusted for this opex growth stood controlled at ~12% YoY.

* Business growth stood modest, with net advances growing 20% YoY/4% QoQ, led by broad-based growth in retail (up 21.3% YoY/4.5% QoQ). Within Retail, VF and Consumer grew at 4.8%/4.3% QoQ, respectively. Wholesale grew 2.8% QoQ, while BB grew 7.7% QoQ.

* Deposit growth stood flat at 16.8% YoY/1.1% QoQ, affected by SA rate cuts, fraud, and tax outflows. The CASA mix moderated further to 49.8% (down 180bp QoQ). The CD ratio rose to 95.2%.

* The GNPA ratio improved 8bp to 1.61%, while the NNPA ratio declined 5bp QoQ at 0.48%. The PCR ratio improved to 70.5%. Gross slippages declined to INR17.8b from INR20.9b in 3QFY26.

Highlights from the management commentary

* IDFCFB’s NIM expanded 17bp QoQ. Of this, ~12bp was driven by the cost of funds reduction, ~2–3bp by CRR-related benefits, and the remainder was partly due to capital infusion during mid-quarter.

* For 4QFY26, management expects NIMs to trend towards ~5.85%, reflecting the full impact of savings rate reductions.

* ECL implementation is expected to be marginally positive overall, although it may result in some increase in reported credit cost going forward.

* INR750m of excess MFI provisions were written back as they were no longer required, while the bank continues to maintain a contingency buffer of INR1,650m for the MFI portfolio.

Valuation and view:

Reiterate Neutral with a TP of INR75 IDFCFB reported a tepid quarter, impacted by one-offs, including higher opex related to the deposit fraud at its Chandigarh branch, treasury losses, and modest business growth. NIM expanded 17bp QoQ, driven by a reduction in cost of funds despite subdued deposit growth, and is expected to remain broadly stable going forward. Deposit growth was muted, affected by savings rate cuts, the fraud-related overhang, and tax outflows. Loan growth remained steady and was led by healthy traction across retail and wholesale segments. One-offs led to a sharp increase in the C/I ratio to 85.5%; however, this is expected to normalize to ~65-70% over FY27E, supported by improving revenue growth and operating leverage. We slightly lower our FY27/28E earnings by 1%/4% and estimate an RoA/RoE of 0.8%/7.6% for FY27. Reiterate Neutral with a TP of INR75 (premised on 1.2x Sep’27E ABV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412