Buy Trent Ltd for the Target Rs. 5,250 by Motilal Oswal Financial Services Ltd

Superlative performance on all fronts

* After several quarters of deceleration in growth rate, Trent’s revenue grew ~20% in 4QFY26 as LFL recovered to low single digit (from mildly negative in 3Q). Trent added 198/52/6 net Zudio/Westside/Star stores in FY26.

* Trent’s gross margin expanded ~170bp YoY, likely driven by a favorable mix (with pick-up in Westside store additions). Further, the company continues to surprise us and the street with robust cost controls as 4QFY26 pre-IND AS EBITDA rose 43% YoY, driven by ~215bp YoY margin expansion.

* For FY26, despite a moderation in revenue growth to ~18% (vs. ~40% YoY in FY25), Trent’s pre-IND AS EBITDA/adj. PAT grew ~27%/24% YoY, driven by cost efficiency measures.

* Capex surged 80%+ YoY to INR14.9b, reflecting a shift toward companyoperated stores, leading to stable YoY FCF generation at INR1.9b.

* Trent’s board has approved raising up to INR25b in equity to accelerate investments in upgrading existing stores, incubating new brands/categories, automating the supply chain, and supporting a faster rollout of Star through selective investments in real estate development.

* We raise our FY27-28E Pre-IND AS EBITDA/PAT by ~4-6%, driven primarily by higher margins and partly offset by lower other income. We build in a CAGR of 21%/22%/11% in standalone revenue/pre-IND AS EBITDA/adj. PAT over FY26-28E.

* We reiterate BUY on Trent with a revised TP of INR5,250, premised on 45x FY28E EV/pre-IND AS EBITDA for the standalone (Westside and Zudio) business, 2.5x EV/sales for Star JV, and ~2x EV/EBITDA for Zara JV.

* The stock currently trades at ~62x FY28 standalone P/E, excluding contribution from Star and Zara JV, and we do not believe there is a scope of significant multiple re-rating, unless the company continues to surprise positively on growth as well as margins.

Revenue growth picks-up; 4QFY26 pre-INDAS EBITDA up 43% YoY

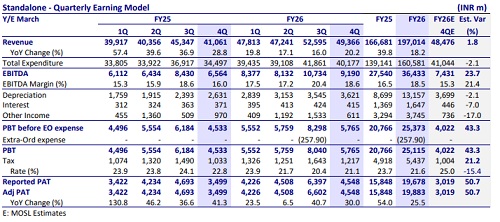

* 4Q standalone revenue at INR49.4b grew 20% YoY (disclosed earlier), driven by ~32% YoY net area additions as revenue per sq.ft. dipped ~11% YoY.

* Trent’s LFL growth for the fashion portfolio recovered to low single digit in 4QFY26 (vs. marginally negative in 3Q).

* Gross profit grew 25% YoY to INR21.9b (7% beat) as gross margin expanded ~170bp YoY to 44.3% (~195bp ahead).

* Despite ~32% YoY net area additions, employee cost grew modest ~11% YoY, while SG&A and other costs rose ~18% YoY. ? Trent’s occupancy cost (rentals above EBITDA) grew ~15% YoY, while lease rentals (below EBITDA) rose ~33% YoY, resulting in overall rental growth of ~21% YoY (broadly in line with revenue growth rather than area growth).

* As a result, reported EBITDA grew 40% YoY to INR9.2b, sharply above our and consensus estimate of INR7.4b/8.0b, with reported EBITDA margins expanding ~265bp YoY to 18.6% (~330bp beat).

* According to the company, 4QFY26 standalone pre-INDAS EBITDA grew 43% YoY to INR6.7b, with pre-INDAS EBITDA margin of 13.5% (up ~215bp YoY), while standalone Pre-Ind AS EBIT margin stood at 11.5% (up ~180bp YoY).

* Depreciation (+38% YoY) and interest costs (+12% YoY) jumped sharply, while other income declined 37% YoY, resulting in ~30% YoY growth in PAT to INR4.5b. The sharp beat on our estimate was driven by higher EBITDA and lower tax rate.

FY26 performance: Growth moderates but margin expands significantly

* For FY26, Trent’s revenue grew 18% YoY to INR197b, driven by ~32% YoY net retail area addition, though offset by a 13% YoY decline in SPSF.

* Reported EBITDA grew 32% YoY to INR36.4b as EBITDA margin expanded ~200bp YoY to 18.5%. Pre-IND AS EBITDA rose ~27% YoY to INR26.9b as margin expanded ~100bp YoY to 13.65%.

* Reported FY26 PAT grew ~24% YoY to INR19.7b (~25% YoY adjusted for labor code impact).

* Working capital days improved to 33 (vs. 37 YoY) as inventory days moderated to 42 (from 44 YoY).

* OCF (after interest and leases) surged 67% YoY to INR16.8b, driven by a 27% YoY increase in pre-IND AS EBITDA and favorable WC movements.

* However, Trent’s net capex jumped sharply to INR14.8b (vs. INR8.2b in FY25), which resulted in stable YoY FCF of INR1.9b.

* Trent’s net cash stood at ~INR2.9b in FY26 (vs ~INR3.4b at end-FY25).

Store adds accelerate; 80% of Zudio expansion driven by entry to new cities

* The pace of store additions accelerated with 122 net store additions, bringing the total fashion format store count to 1,286 (up 23% YoY).

* Westside recorded yet another highest quarterly net store additions of 22 stores (52 in FY26), taking the overall store count to 300 (+21% YoY).

* Zudio witnessed 109 net store openings in 4QFY26 (198 in FY26 vs. 220 in FY25), reaching 963 stores (+26% YoY).

* Trent’s other fashion format store count declined by 9 QoQ to 23 (-23% YoY).

* Notably, a large part of store additions in Zudio in FY26 has been driven by its entry into new cities (78 new cities), which could lead to a slower initial ramp-up but should not have a cannibalization impact on existing stores.

Star business: Muted performance continues; focusing on retail real estate to drive growth

* Revenue (ex-GST) grew 6% YoY (vs. 1% YoY in 3Q)

* Star added 5 net stores in 4QFY26 to reach 84 stores (opened 6 net stores in FY26, 12 opened, 6 closures).

* Calc. annualized revenue per sq.ft. declined ~5% YoY to INR24.3k and annualized revenue per store declined ~1% YoY to INR417m.

* The share of own brand offerings now contributes ~73% to Star’s revenue (+100bp YoY).

Consolidated performance summary

* Consolidated revenue grew 19% YoY to INR50.2b.

* Reported EBITDA grew 42% YoY to INR9.3b, with ~300bp YoY margin expansion to 18.4%. Operating (pre-IND AS) EBITDA grew ~44% YoY to INR6.5b, with margin expanding ~220bp YoY to 13%.

* Adjusted PAT stood at INR4.1b (up ~33% YoY), as higher EBITDA was partly offset by higher D&A (up 38% YoY) and finance costs (+17% YoY).

Highlights from the management commentary

* Demand and macro events impact on costs: Consumer sentiment remained stable in 4Q, but discretionary spend remained cautious due to macro uncertainty and cost pressures. Geopolitical disruptions impacted select input costs and labor availability; India-led sourcing offers partial insulation.

* LFL growth was in low single digits in 4QFY26 and FY26. Management is pursuing micro-market revenue growth rather than store-level LFL.

* New city additions: Zudio entered 78 new cities in FY26, with 80%+ of additions coming in Tier II/III and peripheral markets. Cluster densification is improving revenue density and profitability. New markets to take 2-3 years to reach maturity stage.

* Competitive positioning: Intensity remains high. Own-brand and direct-toconsumer model enable pricing control and differentiation. The company’s focus is on gradual premiumization and brand moat expansion. * Capital allocation: The Board approved INR25b fundraise for store upgrades, new categories/brands, warehouse automation, digital/AI, and commitment in acquiring real estate to drive growth in Star.

Valuation and view

* Trent’s revenue growth decelerated to ~18% YoY in FY26 due to cannibalization of sales in existing stores, weak consumer sentiment, and entry into newer cities, which start at lower initial productivity.

* However, our channel checks indicate that sales decline in cannibalized stores have now eased off. Further, we note Trent’s recent store additions in Zudio are primarily focused on entry into new cities, which could have lower initial productivity, but it would not further cannibalize sales in existing stores.

* Despite relatively weaker growth, Trent continues to display strong cost controls to report healthy profitability in FY26. Going ahead, we believe the margin expansion would largely be dependent on recovery in LFL growth.

* We continue to like Trent for its strong footprint additions, retail formats with robust store economics, long runway for growth in Star (presence in just 12 cities), and potential scale-up of emerging categories (Beauty, Innerwear and Footwear). However, sustained revenue growth acceleration led earnings upgrades remain key to further re-rating.

* We raise our FY27-28E Pre-IND AS EBITDA/PAT by ~5-6%, driven primarily by higher margins and partly offset by lower other income. We build in a CAGR of 21%/22%/11% in standalone revenue/pre-IND AS EBITDA/adj. PAT over FY26- 28E.

* Reiterate BUY on Trent with a revised TP of INR5,250, premised on 45x FY28E EV/pre-IND AS EBITDA for the standalone (Westside and Zudio) business, 2.5x EV/sales for Star JV, and ~2x EV/EBITDA for Zara JV. The stock currently trades at ~62x FY28 standalone P/E, excluding contribution from Star and Zara JV.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412