Buy CIE Automotive India Ltd for the Target Rs.542 by Motilal Oswal Financial Services Ltd

Strong show due to upbeat overall performance

Indian to remain the key growth driver

* CIEINDIA’s 1QCY26 EBITDA/PAT of INR4b/INR2.4b came in ahead of our estimates of INR3.7b/INR2.2b, led by better-than-expected performance, both in India and Europe. India business margins were maintained QoQ despite input cost headwinds. Moreover, the EU business saw better margin expansion post restructuring last year.

* The company’s India business is likely to be a key growth driver, given the pickup in demand across segments. Further, on the back of its new order wins, we expect the India business to resume outperformance relative to industry growth, which was lacking in the recent past. In Europe, it will continue to focus on maintaining margins at reduced demand. At CMP, the stock trades at 18.2x/17.1x CY26E/CY27E consolidated EPS. Reiterate BUY with a TP of INR542 (~20x Mar’28E consolidated EPS).

India demand sustains, upbeat EU performance

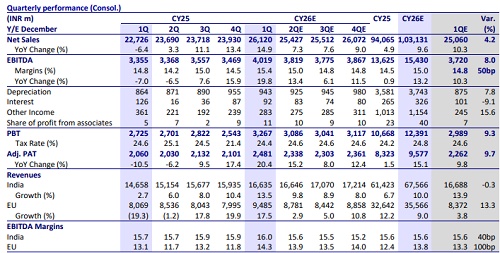

* 1QCY26 consol. revenue grew 15% YoY to INR26.1b, coming in slightly above our estimate of INR25b. Revenue growth was led by 15% growth in the India business and currency translation benefit in the Europe business (17% benefit).

* EBITDA stood at ~INR4b (vs est. INR3.7b), growing 20% YoY. EBITDA margins stood at 15.4% (est. 14.8%), rising 60bp YoY/90bp QoQ.

* Adj. PAT grew 20% YoY and stood at INR2.4b, ~10% above our estimates.

* Indian business performance: Revenue grew 13.5% YoY to ~INR16.6b (in line). India EBITDA margin stood at 16% (est. 15.6%), rising 30bp YoY. Margins were maintained QoQ despite input cost headwinds, led by operational efficiencies.

* EU business performance: EU business revenues saw a healthy 17.5% YoY growth to INR9.5b, above our estimates of INR8.4b. Entire revenue growth was driven by currency translation gains, while revenues in EUR terms were largely flat YoY. Margins expanded 120bp YoY to 14.3% vs the estimate of 13.3%. Margin expansion was due to restructuring benefits of Legazpi and Metalcastello.

* The Board of Directors has approved the merger of CIE Aluminum Casting India into CIE Automotive India. The rationale for the merger includes: 1) Production and marketing synergies, 2) Cross Selling across OEM relationships, 3) Organizational and operating efficiencies, 4) Stronger financial position, and 5) Elimination of inter-company transactions. In CY25, CIE Aluminum casting posted revenue of INR11.7b, with PAT of INR948m.

Highlights from management commentary

* India revenue grew 15% YoY in 1QCY26, broadly in line with the market. Management expects the positive momentum in the Indian business to continue, supported by healthy domestic demand and new order wins

* New order wins remained strong in 1QCY25 at around INR3.5b, with EV-related orders contributing 11%. Management is confident of outperforming market growth on account of these new order wins.

* On capacity, all businesses are performing well, and the company is adding capacity across all verticals except magnets to support expected growth from new orders. Growth capex in India is expected to be higher in CY26 than in CY25, with around 95% of total growth capex directed towards India.

* On raw material inflation, management does not see any major issue in terms of pass-through. The impact of aluminum price increases is expected to reflect in 2Q.

* IHS has estimated a 1-2% YoY decline in LV volumes in Europe in CY26.

Valuation and view

* Domestic demand in India is expected to revive across segments following the GST rate cut. However, the Europe outlook remains subdued, although it seems to be stabilizing at lower levels. Thus, the Indian business is expected to be the primary growth driver for the company, even in CY26.

* Some of the financial attributes unique to CIEINDIA include: being net debt free, having strict capex/inorganic expansion guidelines, generating positive FCF, and tracking an improving return trajectory.

* The CIEINDIA business is likely to be a key growth driver, given the pickup in demand across segments. Further, on the back of its new order wins, we expect the India business to resume its outperformance relative to industry growth, which was lacking in the recent past. In Europe, it would continue to focus on maintaining margins at reduced demand. At CMP, the stock trades at 18.2x/17.1x CY26E/CY27E consolidated EPS. Reiterate BUY with a TP of INR542 (~20x Mar’28E consolidated EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041