Buy UltraTech Cement Ltd for the Target Rs.13,800 by Motilal Oswal Financial Services Ltd

Cost efficiency measures to boost EBITDA

We attended the plant visit event organized by Ultratech Cement (UTCEM) at its Baga plant in Solan, Himachal Pradesh, where we interacted with the management team, followed by a tour of the plant. Key highlights of the interaction: 1) its market share stands at 31.4% vs. capacity market share of 27.8%; 2) it targets EBITDA/t of INR1,400 by 4QFY28 and ~15%+ ROCE by FY28; 3) Industry demand is estimated to clock ~7%- 8% CAGR over the next few years; and 4) UBS stores’ contribution to total volume is targeted to increase to ~40% from the current ~21%.

Key takeaways from management meeting

* Per-capita cement consumption below global average: India’s per-capita cement consumption, at 320kg, is well below the global average of 470kg520kg despite clocking ~5% CAGR over FY16-20. It is expected to rise at ~7% CAGR over FY26-30E, supported by rising urbanization, with urban population share projected to increase to ~40% by FY30 from ~37% currently.

* Demand should grow at ~8% CAGR by FY29E: Industry cement demand is expected to increase at ~7-8% CAGR over the next few years, led by strong growth in rural and urban housing (~7% CAGR each over FY26–30E) and infrastructure demand (~8%+ CAGR). Continued affordable housing allocations will help drive demand growth, rising land purchases by real estate companies (increased by +47% YoY in 2025), and higher infrastructure investments over FY26-30E is expected to be at 1.5x of FY21- 25 investment levels, with roads accounting for ~55% of spending, which will remain key demand drivers.

* Market share gain with improving profitability: UTCEM has continued to gain market share, with its current market share at ~31.4% vs. capacity market share of ~27.8%. This growth has been supported by stronger profitability, with average EBITDA/t improving to INR1,143 during FY20-26 from INR975 in FY15-20. The company targets ~15%+ RoCE by FY28E and aims to achieve INR1,400/t EBITDA by 4QFY28, driven mainly by cost improvement measures.

* Cost-efficiency measures driving profitability improvement: Cost efficiency programs delivered a cumulative benefit of INR185/t during FY25-26, led by lower lead distance, higher green energy usage, improved clinker-tocement ratio, and reduced power and heat consumption. The company expects to surpass its earlier cost-saving target of INR300/t by FY28.

* Cable & Wires Capacity Utilization and Asset Turn Targets: The Cable & Wires segment targets optimum capacity utilization by FY30E, with asset turns expected at 4–5x. The product mix is guided toward ~60% wires and ~40% cables (primarily LT cables)

Valuation and view:

* UTCEM is a market leader with ~31% market share. The company reported strong profitability in 4QFY26, led by cost efficiency and a timely integration of acquired assets. UTCEM believes cost headwinds due to the West Asia conflicts are manageable in the near term with multiple levers and partially through the price hike taken so far. We estimate a CAGR of 13%/15%/18% in consolidated revenue/EBITDA/PAT over FY26-28. We estimate its consolidated volume CAGR at ~10% and EBITDA/t of INR1,136/INR1,216 in FY27E/FY28E vs. INR1,103 in FY26.

* We estimate its net debt at INR178.4b in FY27 (to be peaked out) vs. INR146.9b in FY26. The net debt-to-EBITDA ratio is estimated to remain below 1.0x. We estimate its RoE/RoCE to increase to ~14%/12% by FY28 from ~11%/10% in FY26, backed by a rise in profitability and lower capex for ongoing expansions.

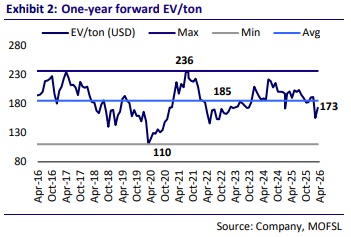

* The stock is currently trading at 19x/15x FY27E/FY28E EV/EBITDA. We value UTCEM at 18x FY28E EV/EBITDA to arrive at a TP of INR13,800. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412