Buy Mahindra Lifespaces Ltd for the Target Rs. 425 by Motilal Oswal Financial Services Ltd

Pre-sales growth expected to pick up

Healthy business development provides comfortable growth visibility

Mahindra Lifespaces (MLDL) added seven projects in FY26, offering INR105b GDV as a part of the business development activity. The development plan for Thane land was approved by the authority in FY26, which added INR75b to the GDV addition. Mitsui Fudosan, the partner for the Blossom project, has committed to one more deal, and the company is exploring potential JVs with other financial partners. In FY27, it targets new project additions offering INR100b GDV, which would replenish the launch pipeline and offer mediumterm growth visibility.

Healthy pre-sales momentum driven by sustenance and new launches

MLDL recorded strong 55% YoY growth in pre-sales to INR16.3b (in line with estimates), which led to an overall 21% YoY growth to INR34b in FY26. During the year, it launched INR74b GDV across projects, including New Haven (Bengaluru), Marina64 (MMR), Lakewoods (Chennai), Blossom (Bengaluru), and Rainforest (MMR). Except for the Rainforest project (launched in FY26-end; pre-sales expected from FY27), the remaining five projects contributed meaningfully to FY26 performance. The share of sustenance sales increased to 40% in FY26 vs 35% in FY25, and the company anticipates this to further increase to 75% by FY30. We expect MLDL’s healthy launch pipeline worth INR70b in FY27, as well as sustenance inventory and bookings from the Rainforest project, to drive a 27% CAGR in pre-sales to INR55b during FY26- 28E.

C&IC operations progressing at a healthy pace

IC&IC business revenue grew 26% YoY to INR3.6b in 4QFY26 on the back of nine deals during the quarter. Total leased area in the quarter stood at 84.9 acres. Overall, the segment witnessed 44% YoY growth in revenue to INR7.1b in FY26. Strong leasing activity and higher realization were observed in Jaipur and Chennai. MLDL has resolved legacy issues at its Origins Ahmedabad site and is scouting for an apt anchor customer, with a potential closure expected in FY27 (marketing activities already started). Further, it is in the process of land aggregation for Origins Pune, which would drive revenue growth over the medium term. We expect a 10% CAGR in IC&IC business revenue to INR8.6b during FY26-28E.

Financial performance

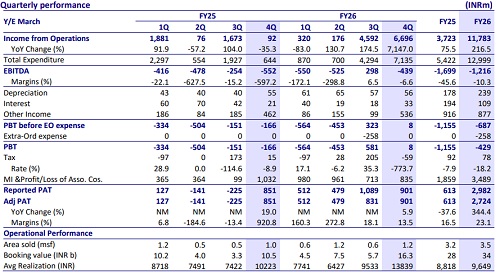

* MLDL’s revenue came in at INR6.7b due to four completions in the quarter - Ph1 of Eden, Nostalgia, Tatawade, and Palghar. EBITDA loss stood at INR439m vs. a loss of INR552m for 4QFY25. PAT stood at INR901b, up 6% YoY. In the residential segment, collections grew 36% YoY to INR6.4b, while in FY26, they grew 15% YoY to INR21b. The OCF generation was strong at INR8.4b, despite incurring the approval cost of the Rainforest project, which had no bookings in FY26.

* In FY26, MLDL’s revenue came in at INR11.8b, rising 3x YoY. EBITDA loss stood at INR1.2b vs. a loss of INR1.7b for 4QFY25. Adj PAT stood at INR2.7b, up 6% YoY.

Valuation and view

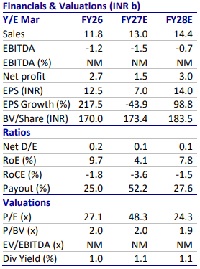

* We value the residential business on a DCF basis, with a WACC of ~12.3%, translating into INR68b.

* We upgrade our rating to BUY on the stock with a TP of INR425, reflecting a 25% upside.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412