Neutral Alkyl Amines Chemicals Ltd for the Target Rs. 1,720 by Motilal Oswal Financial Services Ltd

Muted quarter, with gradual demand recovery likely in FY27

Strong beat on our estimates

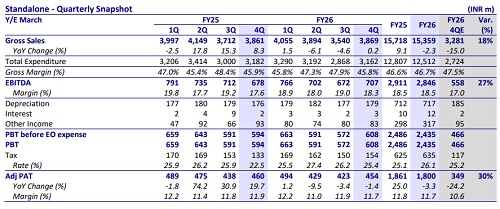

* Alkyl Amines Chemicals (AACL) reported a steady operating performance with EBITDA growth of 4% YoY in 4QFY26. The company successfully mitigated raw material cost pressures through price pass-throughs, driving a 70bp YoY improvement in EBITDA margin to 18.3%.

* While volume growth remained flat in FY26, the growth momentum is expected to improve steadily, driven by rising demand from the pharma segment led by peptides, with management guiding a 5-10% overall volume growth. Further, the anti-dumping duty (ADD) on acetonitrile is likely to aid price recovery and strengthen AACL’s market position.

* We broadly maintain our earnings estimates and value the stock at 40x FY28E EPS to arrive at a TP of INR1,720. Reiterate Neutral.

Stable operating performance with margin resilience

* Revenue stood flat YoY while growing 9% QoQ to INR3.9b (est. INR3.2b), while gross margin remained flat YoY and contracted 200bp QoQ to 45.8%.

* EBITDA margins expanded 70bp YoY but contracted 70bp QoQ to 18.3% (est. 17%). Employee costs as a percentage of sales stood at 7.5% (vs. 6.4% in 4QFY25), while other expenses stood at 20.1% vs. 21.9% in 4QFY25.

* EBITDA stood at INR707m, up 4% YoY and 5% QoQ (est. of INR558m).

* Adj. PAT stood at INR454m, down 1% YoY and up 7% QoQ (est. of INR349m). ? In FY26, Revenue/EBITDA/Adj. PAT declined ~2%/2%/3% to INR15.4b/INR2.8b/INR1.8b.

* The company stands debt-free as of Mar’26. Further, the cash flow from operations in Mar’26 stood at INR2.4b

Highlights from the management commentary

* Guidance and outlook: Management remains cautiously optimistic on the outlook, supported by a moderation in aggressive pricing from Chinese players, which is expected to aid industry-wide margin recovery. While prices are unlikely to revert to pre-Feb levels, the company believes the worst of the downturn is behind it and continues to guide a 5-10% volume growth.

* Macro environment: FY26 remained challenging, with flat revenue and profit performance amid subdued demand, although the company gained market share in select products. Additionally, the ADD on acetonitrile reduced imports and supported an improvement in domestic pricing towards the end of the year.

* End-user demand scenario: The pharma industry remained relatively insulated from tariff-related disruptions, with the outlook continuing to remain positive, led by the growth in the peptides segment. However, the Agri segment’s outlook remains cautious due to El Niño-related concerns.

Valuation and view

* We expect short-term headwinds to persist due to the uncertainty in the microenvironment and significant uncertainty stemming from the tensions in the Middle East, impacting the raw material prices.

* Going forward, the growth will be aided by i) the planned commercialization of a new product at the Kurkumbh facility in 2QFY27, ii) additional products in the R&D pipeline, iii) the anti-dumping duty on acetonitrile, iv) headroom in improving capacity utilization leading to operating leverage, and v) rising demand from the pharma segment.

* We estimate a CAGR of 6%/6%/7% in revenue/EBITDA/PAT over FY26-28 and maintain our earnings estimates. We value the stock at 40x FY28E EPS to arrive at our TP of INR1,720. Reiterate Neutral.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)