Buy Coforge Ltd for the Target Rs.1,900 by Motilal Oswal Financial Services Ltd

Growth, no matter what

Ambitious targets in a challenging macro setup, but evidence tilt the odds in Coforge’s favor

We attended Coforge's Analyst Day, where discussions were centered on the company's medium-term growth aspirations, margin outlook following the Encora acquisition, evolving commercial models and the role of AI across its key verticals. Management outlined its ambition to scale up revenue from ~USD2.5b currently to ~USD5b by FY30, implying a revenue CAGR of ~19% (~15% organic), supported by deeper penetration within existing verticals, increasing wallet share in large accounts, sustained large-deal momentum, and selective acquisitions. The company also indicated that its margin profile has structurally improved, with portfolio rationalization, acquisition integration and productivity initiatives supporting margins at levels above historical averages.

We came away with the view that Coforge is attempting to evolve beyond a purely volume-led growth model. Management increasingly emphasized domain-led transformation programs, outcome-oriented commercial structures, and larger, proactive engagements across key verticals such as Banking (29% of revenue) and Travel (25% of revenue). While the medium-term ambition appears achievable given the company's execution track record, sustained delivery will depend on successful large-deal conversion, integration of acquisitions and continued monetization of AIled opportunities. We continue to view COFORGE as a structurally strong mid-tier player and reiterate it as our top pick. We value COFORGE at 26x FY28E EPS with a TP of INR1,900, implying a 30% potential upside. Reiterate BUY.

Revenue outlook: Growth aspirations supported by vertical depth, deal momentum and acquisitions

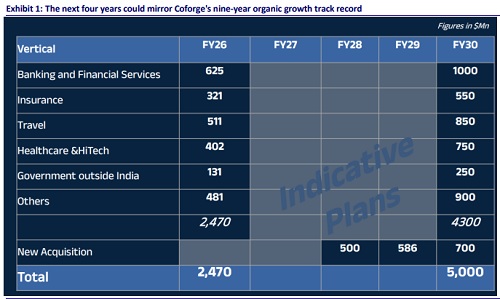

* Management outlined an ambition to scale up revenue from ~USD2.5b currently to ~USD5b by FY30, implying a revenue CAGR of ~19% (organic revenue growth of 15%; see Exhibit 1). The growth framework is built around deeper penetration within existing verticals, increasing wallet share in large accounts, and selective acquisitions.

* The next leg of growth is expected to be driven by scaling up existing franchises rather than building new businesses. Management expects Banking to expand from ~USD625m currently toward ~USD1b, Travel from USD511m toward USD850m, Insurance from USD321m toward USD550m, and Healthcare & Hi-Tech from ~USD402m toward ~USD750m over the planning period.

* Large deals remain an important source of visibility. The number of large deals increased to 21 in FY26 from 11 in FY22, while the 12-month executable order book expanded to ~USD1.75b from ~USD720m over the same period. Management also highlighted that order intake has nearly doubled over the last four years.

* We believe the key takeaway is that Coforge is attempting to move beyond a purely volume-led growth model. Increasing wallet share within large accounts, embedding AI into transformation programs, and expanding outcome-oriented engagements could gradually improve the quality and durability of growth. That said, execution around large-deal conversion, acquisition integration, and AI monetization will remain key monitorables

Valuation and view

* We expect COFORGE to be the growth leader within our coverage universe and we reiterate it as our top pick.

* The analyst day reinforced our confidence in Coforge's medium-term growth outlook. Management outlined its ambition to scale up revenue to ~USD5b by FY30, supported by increasing wallet share within key accounts, healthy large-deal momentum, deeper penetration across core verticals, and a structurally stronger margins profile.

* We continue to view COFORGE as a structurally strong mid-tier player, supported by an improving margin profile, strong deal wins, and consistent growth outperformance. We value COFORGE at 26x FY28E EPS with a TP of INR1,900, implying a 30% potential upside. We reiterate our BUY rating on the stock.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)