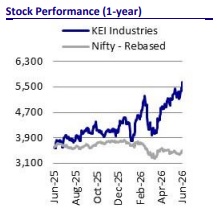

Buy KEI Industries Ltd for the Target Rs.6,640 by Motilal Oswal Financial Services Ltd

Power cable expansion improving margin Capacity expansion continues to drive growth

KEII has outlined a disciplined expansion strategy, with INR20b of investments planned over the next 3–4 years, largely funded through internal accruals. The Sanand facility is expected to be a key growth driver, with incremental revenue potential of INR60b by FY29 and sales of INR27b–30b targeted for FY27. LT/HT cable trial production commenced in Dec’25, while mediumvoltage and EHV capacities are expected to be commissioned by mid-FY27 and Mar’27, respectively. Beyond Sanand, the company plans further brownfield and greenfield expansions, including projects at Bhiwadi and Baroda. It plans to manufacture HVDC cables at Sanand, potentially becoming the first Indian company to do so, positioning it to benefit from rising investments in renewable energy, long-distance power transmission, and upcoming government-led HVDC projects

Strengthening retail presence; expanding market reach

KEII has significantly strengthened its retail presence, with B2C contribution rising from ~29% in FY20 to ~56% in FY26, supported by sustained distribution expansion and brand-building initiatives. Its network now comprises over 2,125 active dealers/distributors across India, with dealer contribution at ~54% in FY26. The dealer business comprises ~50–55% wires and ~45–50% cables, while the institutional segment remains largely cable-led. Exports continue to be a key growth driver across the Middle East, Australia, Africa, Europe, and the US. The company has also entered the solar cables and wires segment using electron beam technology. Backed by a healthy order book of INR36.9b across EHV, institutional, EPC, and export businesses, management expects volume growth of ~17%–18% in FY27.

Robust growth ahead; capex well-funded through healthy cash flows

We estimate Revenue/EBITDA/PAT CAGR at ~21%/26%/23% over FY26-28, led by ~22% growth in the C&W segment and ~7% growth in the SSW segment. However, EPC revenue is likely to decline ~3% p.a. OPM is expected to expand 30bp/60bp to 10.9%/11.5% by FY27/FY28 vs. 10.6% in FY26. We estimate a cumulative OCF of INR12.4b over FY27-28 vs. INR8.1b over FY25-26. Cumulative FCF is estimated at INR1.8b over FY27-28E vs a net cash outflow of INR11.4b over FY25-26. We estimate the company’s net cash to stand at INR15.1b by FY28 vs. INR13.3b as of FY26.

Valuation and view

Near-term growth will be partially constrained by capacity limitations at existing plants, which are already operating at near peak utilization. Incremental growth will, therefore, be driven primarily by new capacities. The company is likely to continue its expansion journey over the medium term, which will also contribute to fueling its growth. In addition, it is scaling up exports with a target of ~20% of total revenue in FY27E vs. ~15% in FY26. We reiterate our BUY rating and value KEII at 45x FY28E EPS to arrive at a revised TP of INR6,640.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412