Neutral Mahindra Logistics Ltd for the Target Rs. 410 by Motilal Oswal Financial Services Ltd

Healthy growth across key segments; strong outlook

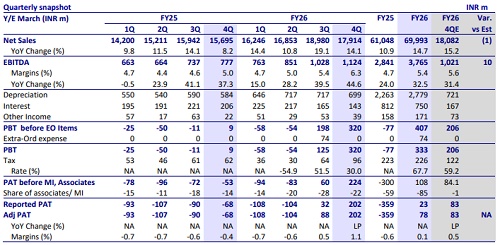

* Mahindra Logistics’ (MLL) revenue grew ~14% YoY to ~INR17.9b in 4QFY26 (in line). EBITDA margin came in at 6.3% in 4QFY26 (up 130bp YoY/90bp QoQ) vs. our estimate of 5.6%. EBITDA grew ~45% YoY to INR1,124m (10% above our est.)

* Adjusted net profit stood at INR202m in 4QFY26 vs. an adjusted net loss of INR68m in 4QFY25.

* Supply chain management recorded revenue of INR16.8b (+13% YoY) and EBIT of ~INR297m. Enterprise Mobility Services (EMS) reported revenue of INR1,139m (+42% YoY) and EBIT of INR23.7m.

* In FY26, the company’s revenue/EBITDA grew 15%/33%, while its APAT turned positive and stood at INR78m vs a loss of INR359m in FY25.

* MLL reported healthy revenue growth and EBITDA margin in 4QFY26, driven by broad-based growth across the 3PL, Freight Forwarding, Mobility, and Express segments. We largely maintain our estimates for FY27 and increase FY28 earnings on the back of improved outlook in the Express business, as current investments in capabilities would start yielding results by then. We forecast a revenue and EBITDA CAGR of 16% and 25%, respectively, over FY26-28, and reiterate our Neutral rating with a revised TP of INR410 (premised on 20x FY28E EPS).

Improved execution and margins drive earnings

* MLL reported a 14% YoY growth in consolidated revenue in 4QFY26, driven by a 12% YoY increase in the Contract Logistics segment, ~49% YoY growth in the Express segment, 17% growth in the Cross Border segment, and a 39% YoY rise in the Mobility business.

* Management stated that volume growth is driven by improved execution and customer engagement and is sustainable in nature.

* The company delivered healthy gross margins across business segments, with strong improvement in Last Mile, Cross-Border, and B2B Express segments, while Contract Logistics also witnessed a marginal uptick.

* The Express business reported its third consecutive quarter of positive gross margin at INR66m. However, it continued to report losses at the EBITDA level.

* White space reduction in warehousing remains on track, with the company targeting a 95% reduction by Sep’26 from an initial 1.6m sq. ft. It has already reduced this to ~0.7m sq. ft. by FY26-end, implying a reduction of ~0.9m sq. ft. during the year.

Highlights from the management commentary

* Within Contract Logistics, the company secured multiple wins across diverse segments, supporting scale-up. Additionally, a strong expansion in margins in the B2B Express and Last-Mile Delivery businesses, along with marginal improvement across other verticals, led to a broad-based expansion in EBITDA margins.

* The company indicated its intent to step up investments in technology in FY27, highlighting that such investments had been largely deferred over the past two years.

* MLL witnessed a healthy volume growth in Express business volumes, which supported revenues and helped reduce losses. The express markets hold huge potential for MLL, and the company expects improved profitability ahead.

* MLL rights issue proceeds were utilized to significantly reduce borrowings, with standalone operations now debt-free. The savings in interest cost post repayment of debt also aided in profitability.

Valuation and view

* MLL reported healthy revenue growth and EBITDA margins in 4QFY26, driven by broad-based growth across the 3PL, Freight Forwarding, Mobility, and Express segments. Going forward, the company remains focused on strengthening execution, enhancing yields, optimizing existing capacity, and improving the Express business.

* We largely maintain our estimates for FY27 and marginally increase FY28 earnings on the back of improved outlook on the Express business. We forecast a revenue and EBITDA CAGR of 16% and 25%, respectively, over FY26-28, and reiterate our Neutral rating with a revised TP of INR410 (premised on 20x FY28E EPS).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412