Buy Mahindra & Mahindra Financial Ltd for the Target Rs. 350 by Motilal Oswal Financial Services Ltd

Management overlay prudent amid macro uncertainties

PPoP beat; in-line PAT due to higher provisions from management overlay

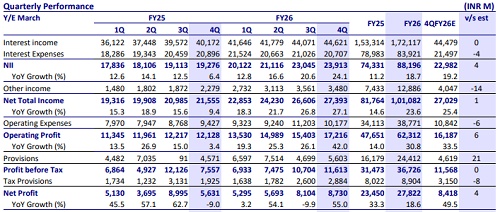

* Mahindra & Mahindra Financial’s (MMFS) 4QFY26 PAT rose ~55% YoY and 8% QoQ to ~INR8.7b (in line). FY26 PAT grew 19% YoY to INR27.8b. 4Q NII stood at INR23.9b (in line), up ~24% YoY. Other income rose ~53% YoY to ~INR3.5b, driven by healthy fee income and dividend income of INR309m received from MIBL (PQ: INR464m).

* Opex stood at ~INR10.2b (up ~8% YoY) and the cost-income ratio stood at ~37.2% (PQ: ~42.1% and PY: ~43.7%). The sequential decline in employee expenses was because 3Q had one-time expenses related to the implementation of the labor code. PPoP stood at ~INR17.2b (~6% beat), up ~42% YoY. FY26 PPOP grew ~31% YoY to INR62.3b.

* Credit costs stood at ~INR5.6b (~21% higher than MOFSLe). Annualized credit costs stood at ~1.7% (PQ: ~1.5%). In 3QFY26, the company had created a management overlay of INR6.35b. Subsequently, in 4QFY26, the company computed ECL provisions based on its updated ECL model and created an additional management overlay of INR2.2b, taking the cumulative management overlay to ~INR8.5b.

* Management shared that overlays were created to factor in macro risks such as geopolitical uncertainties and monsoon-related El Nino concerns that could impact asset quality, particularly in the tractor portfolio; MMFS shared that collection efficiency has remained stable with no material deterioration observed in Apr’26 (relative to Mar’26).

* The company targets ~16-18% AUM CAGR over the next 4-5 years, with the core wheels business expected to grow in line with industry trends, while MSME, mortgage, leasing, and cross-selling segments are likely to grow at ~30-40%, thereby driving overall healthy mid-teens loan growth.

* MMFS delivered a steady FY26 with improved margins, robust profitability, and a sharp improvement in asset quality, supported by momentum in core and emerging segments. Growth picked up in 2HFY26 but the outlook remains cautious due to geopolitical uncertainties and monsoon-related risks, particularly for the rural portfolio.

* We raise our FY27/FY28 PAT estimates by 3%/2% to factor in slightly lower opex driven by operating efficiency. We estimate a ~19% PAT CAGR over FY26-FY28E, with FY28 RoA/RoE of 2.2%/14%. Reiterate BUY with an unchanged TP of INR350 (based on 1.6x Mar’28E BVPS).

* Key risks: a) yield compression due to higher competitive intensity from banks; b) strong auto demand (post the GST rate cut) fizzling out in the coming quarters, potentially leading to muted loan growth; 3) impact on asset quality and credit costs due to the ongoing West Asia war and El Nino impact; and 4) any compression in NIM from the scale-up in the mortgage business.

NIM expands ~10bp QoQ; yields (calc.) decline ~20bp QoQ

* Yields (calc.) declined ~20bp QoQ to ~14%, while CoF (calc.) declined ~30bp QoQ to 7%, leading to spreads expanding by ~10bp QoQ to 7%. NIM (calc.) rose ~10bp QoQ to ~7.3%.

* Fee income improved to 1.4% (as % of avg. assets) in FY26 (vs. 1.1% in FY25). Management guided for fee income to improve to ~1.4-1.5% as a sustainable medium-term range. We model NIM of 6.4% each (as a % of avg. assets) for FY27/FY28E (vs. 6.2% for FY26).

Key takeaways from the management commentary

* MMFS shared that in the CV segment, the company is shifting its focus toward LCV/SCV categories, selectively expanding in HCVs, and increasing its presence in used vehicles, which remain an attractive opportunity despite ongoing supply constraints.

* Management highlighted that margin expansion was driven by a better product mix (higher share of tractors and used vehicles), rising fee income, and improved treasury performance which led to decline in CoF.

Valuation and view

* MMFS reported a steady operational quarter, with healthy disbursements driven by sustained momentum in tractors and vehicle demand following GST cuts. Asset quality improved meaningfully, with GS3 and NS3 nearing multi-year lows, resulting in lower net slippages, although the company remains cautious amid geopolitical tensions and potential El Nino impact. NIM expanded during the quarter, supported by strong fee income and a decline in cost of funds.

* MMFS currently trades at 1.5x FY27E P/BV. With a projected PAT CAGR of ~19% over FY26-FY28E and RoA/RoE of 2.2%/14% in FY28E, we reiterate our BUY rating with an unchanged TP of INR350 (based on 1.6x Mar’28E BV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412