Multiplex Sector Update : BO trend and Rs1bn pipeline for 2QFY27E by PL Capital

Industry wide NBOC’s (including regional movies) increased 12.1% YoY to ~Rs27.6bn in 1QFY27E. List of movies that have done well during the quarter include: -

* Peddi – Rs2.41bn

* Karuppu – Rs1.98bn

* Bhooth Bangla – Rs1.82bn

* Vaazha 2 – Rs1.29bn

* Drishyam 3 – Rs1.1bn

* Raja Shivaji – Rs963mn

* Cocktail 2 – Rs867mn

* Obsession – Rs824mn

* Welcome to the Jungle – Rs815mn (Spillover to happen in 2QFY27E)

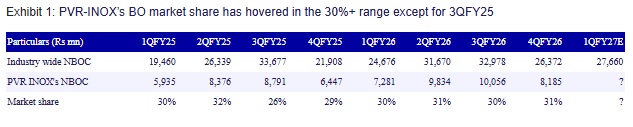

As can be seen, barring Bhooth Bangla, no Bollywood movie was able to strike a chord with the audience and BO collections for 1QFY27E were dominated by regional movies. However, in regional genre PVR INOX’s BO market share ranges from ~10-20%. Thus, we believe, in 1QFY27E, PVR INOX’s BO market share could be lower than the historical average of 30% odd (check exhibit 1 below for historical trends). In fact,1QFY27E takes us back to the memories of 3QFY25, where-in the market share was lower than historical average as BO collections were dominated by Pushpa-2.

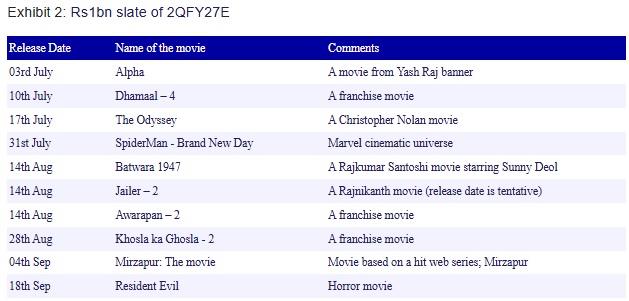

While 1QFY27E is expected to be lukewarm, the pipeline for 2QFY27E seems exciting as the content flow in July and Aug is good. Here is our Rs1bn list for 2QFY27E.

Our view: Apart from the content pipeline which appears decent for 2QFY27E, there are 3 key reasons why we like PVR-INOX at CMP.

* Improvement in BS strength: After generating FCFF of Rs7,901mn, BS strength has improved considerably with net debt declining to Rs1,619mn in FY26.

* Pivot towards capital light model: A pivot towards capital light model (138 screens signed under FOCO/asset-light model) will not only enable cash preservation ensuring BS strength remains intact but will also aid in improving capital efficiency.

* Attractive valuations: The stock trades at 9.1x/7.0x our FY27E/FY28E pre-IND AS EBITDA estimates. We retain BUY on the stock with a TP of Rs1,309 (9.5x FY28E pre IND AS EBITDA)

Please refer disclaimer at Report

SEBI Registration number is INH000000933

More News

Defence & Aerospace Sector Update : Revenue softness due to execution timing, but margin & e...