Buy RBL Bank Ltd for the Target Rs. 370 by Motilal Oswal Financial Services Ltd

Core earnings inline; Credit cost remains elevated

NIMs contract 22bp QoQ to 4.41%

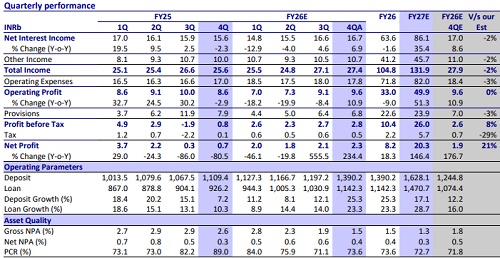

* RBL Bank (RBK) reported 4QFY26 PAT of INR2.3b (up 234% YoY, 7.4% QoQ), aided by a lower tax rate, though PPoP stood in line.

* NII saw healthy growth of 7% YoY/0.8% QoQ to INR16.7b (in line). NIMs declined 22bp QoQ in 4Q, driven by lower yields and mix changes. The bank expects NIMs to remain stable in 1QFY27 and improve from 2Q onward.

* Opex grew 5% YoY/fell 1% QoQ (in line), while other income was INR10.7b (broadly in line). C/I ratio, thus, improved to 65.1% (vs. 66.3% in 3QFY26).

* Advances grew strongly at 23% YoY/10.8% QoQ, while deposits grew 25% YoY/16% QoQ. CASA mix improved to 33.6% vs. 30.9% in 3QFY26, aided partly by period-end flows. * Fresh slippages increase slightly to INR9.3b. GNPA/NNPA ratios, however, improved sharply by 43bp/16bp QoQ, aided by healthy upgrades to 1.45%/0.39%. PCR improved further to 73.6%.

* We cut our FY27/28 earnings estimates by 14%/5% to factor in the margin compression and slightly higher credit cost given ongoing credit card stress. We thus estimate RoA to recover to 1.3% by FY28E. Reiterate BUY with a TP of INR370 (1.3x Sep’27E ABV)

Guides for 20%+ growth in FY27; PCR improves to 73.6%

* RBK reported 4Q PAT of INR2.3b (up 234% YoY/7% QoQ) amid lower-thanexpected provisions and lower tax.

* NII was up 7% YoY/flat QoQ at INR16.7b (largely in line). NIM declined 22bp QoQ in 4Q to 4.41%, driven by lower yields on advances (repo cuts, mix shift). Management expects NIMs to improve from 2QFY26 onward.

* Other income grew 7% YoY/2% QoQ to INR10.7b (in line), led by core fee income growth of 9% YoY/10% QoQ to INR10.6b. Treasury income was modest. Total revenue grew 7% YoY/1% QoQ to INR27.4b. Opex rose 5% YoY/fell 1% QoQ to INR17.9b. C/I ratio declined 117bp QoQ to 65.1%.

* PPoP grew 11% YoY/5% QoQ to INR9.6b (in line), as lower other income was offset by lower opex.

* Provisions remained elevated at INR6.8b, largely driven by credit card, MFI and PL. Of total provisions, cards accounted for INR4.9b, MFI INR1.5b and wholesale INR70m. Management expects credit cost moderation in FY27.

* Advances grew 23% YoY/11% QoQ to INR1.14t. Retail advances grew 21% YoY/11% QoQ, while wholesale advances rose 28% YoY/11% QoQ. Secured retail continued to scale up strongly at 36% YoY/17% QoQ.

* Deposits grew 25% YoY/16% QoQ to INR1.39t. CASA mix improved 273bp QoQ to 33.6%, partly aided by temporary wholesale CASA flows. C/D ratio moderated to 82.2%

.* Fresh slippages rose slightly to INR9.3b from INR9.1b in 3QFY26. GNPA ratio improved sharply by 43bp QoQ to 1.45%, while NNPA ratio declined 16bp QoQ to 0.39%. PCR improved to 73.6%.

* CAR stood at 14.25% with CET1 at 12.77%. Management expects Emirates NBD capital infusion in 1QFY27, which should support growth acceleration and lower funding costs.

Highlights from the management commentary

* Loan growth is guided to be in the 20%+ range, with wholesale at 20-25%, secured retail strong, and MFI/unsecured at calibrated 15-20%.

* ROA is expected to improve progressively through lower liability costs, secured retail scale-up and credit cost normalization.

* FY27 deposit growth is expected in single digits to low double digits as the bank prioritizes deploying equity capital and avoids expensive deposits. Retail deposits will continue to grow ~25%. From FY28, deposit growth is expected to re-accelerate to 15-20%.

* From FY28, deposit growth is expected to re-accelerate to 15-20%.

Valuation and view

RBK reported an in-line quarter, with NII and PPoP largely in line, while a lower-thanexpected tax outgo led to an earnings beat. NIMs declined sharply by 22bp QoQ, impacted by yield compression and a shift in portfolio mix. Business growth remained strong, with the bank reiterating its loan growth guidance of 20%+, led by wholesale growth of 20-25% and MFI/unsecured growth of 15-20%. The bank continues to pursue calibrated expansion in the unsecured segment. Additionally, the capital infusion from Emirates NBD is expected to support stronger credit growth. On asset quality, slippages are expected to remain elevated in 1HFY27, primarily driven by credit cards, before moderating thereafter. Slippages are likely to gradually decline in 2HFY27, which should support a reduction in credit costs toward ~1.5%. We cut our FY27/28 earnings estimates by 14%/5% to factor in the margin compression and slightly higher credit cost given ongoing credit card stress. We thus estimate RoA to recover to 1.3% by FY28E. Reiterate BUY with a TP of INR370 (1.3x Sep’27E ABV).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412