Neutral Hindustan Zinc Ltd for the Target Rs. 630 by Motilal Oswal Financial Services Ltd

Earnings beat over favorable pricing and lower costs

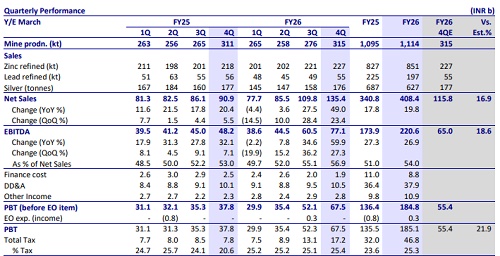

* Hindustan Zinc (HZ) reported revenue of INR135b (+49% YoY and +23% QoQ) for 4QFY26, beating our estimate of INR116b. The growth was driven by favorable commodity prices and volumes recovery. * EBITDA came in at INR77b (+60% YoY and +27% QoQ), against our estimate of INR65b during the quarter. The increase was primarily on account of favorable metal prices and lower cost of production. EBITDA margin stood at 56.9% in 4QFY26 vs 55.1% in 3QFY26 and 53% in 4QFY25.

* Zinc COP (ex-royalty) stood at USD903/t in 4QFY26, declining 9% YoY and 4% QoQ, driven by lower power costs from increased domestic coal usage and better mined grades of 7.9% in 4QFY26 (~7.3-7.4% in FY26).

* APAT stood at INR50b (+68% YoY and +29% QoQ), against our est. of INR41b in 4QFY26.

* Mined metal for the quarter stood at 315kt (+1% YoY and +14% QoQ), driven by higher ore production and better grade.

* Refined metal production for the quarter stood at 282kt (+5% YoY and QoQ), driven by incremental capacity via debottlenecking at Chanderiya and Dariba with better plant availability. Refined zinc production was 227kt (+6% YoY and +3% QoQ), while refined lead production stood at 55kt (-2% YoY and +12% QOQ) due to partial pyro operation on lead mode.

* Salable silver production rose 11% QoQ and remained flat YoY at 176kt, in line with lead production.

* In FY26, the revenue grew 20% YoY to INR408b, whereas EBITDA and PAT increased by 27% and 34% YoY to INR221/138b, respectively. Zinc CoP (exroyalty) stood at USD956/t (-9% YoY) in FY26.

* HZ clocked mined metal production of 1.11mt (+2% YoY), while refined metal stood flat YoY at 1.05mt in FY26. Of this, refined zinc output stood at 851kt (+3% YoY), and lead production declined 13% YoY to 197kt. The salable silver output declined 9% YoY to 627t during FY26.

Key management commentary

* The company guided for refined metal production of 1,100ktpa and expects to achieve silver output of 680t for FY27.

* HZ expects Zinc CoP (ex-Royalty) to remain at USD975-1,000/t in FY27. Crude volatility, explosives, and chemicals are included in FY27 cost assumptions. Management retains confidence, supported by higher renewable-energy usage and better ore grades.

* For 1QFY27, 20kt zinc is hedged at ~USD3,100/t and 25t of silver at ~USD57/oz, while FY27 hedges stand at 71kt of zinc at ~USD3,225/t and 59t of silver ~USD60/oz, offering partial downside protection. * Management guided that the bulk of silver growth (towards ~1.5kt target) is contingent on doubling of lead capacity and SK mine ramp-up.

Valuation and view

* HZ delivered a strong earnings performance in 4QFY26, primarily driven by favorable metal pricing and a recovery in volumes. The company continues to focus on increasing production output with tighter cost-control measures, which could lead to margin sustenance.

* The recently announced expansion plans are aligned with its long-term objective of doubling existing capacity and enhancing long-term earnings visibility. Although near-term earnings growth is capped due to limited capacity headroom, the LME/silver price inflation emerges as the key catalyst for incremental upside in the near term. We maintain our FY27/28 estimates and believe further price volatility could remain a potential risk or reward for the earnings visibility.

* At CMP, HZ trades at 7.8x FY28E EV/EBITDA, and we believe the current valuation has priced in all the positive factors. We reiterate our Neutral rating with a TP of INR630 (premised on 8.5x EV/EBITDA on FY28E).

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412