Buy Zensar Ltd for the Target Rs. 640 by Motilal Oswal Financial Services Ltd

Recovery to follow steadily

2HFY27 growth hinges on mega-deal ramp up; TMT drag continues

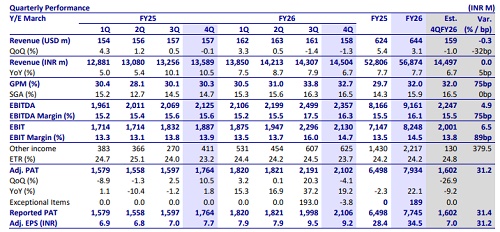

* Zensar (ZENT) reported 4QFY26 with a revenue decline of 1.9% QoQ CC (est. a decline of 1.8% CC). BFSI grew 1.2% QoQ CC, while HLS/MCS declined 6.6%/3.9% QoQ CC. Deal TCV: Bookings came in at USD401.8m (up 122.9% QoQ/down 88% YoY), and the book-to-bill was 2.5x. EBIT margin was 14.7% (est. 13.8%), down 130bp QoQ. Adj. PAT of INR2,102m (down 4.1% QoQ/19.2% YoY), above our estimate of INR1,602m.

* For FY26, revenue/EBIT/adj. PAT grew 7.7%/15.4%/22.1% YoY in INR terms. In 1QFY26, we expect revenue/EBIT/adj. PAT to grow 7.5%/9.6%/3.7% YoY. Cash flow from operations stood at ~97% of adj. net profit for FY26. For FY26, RoE came in at 18.1% (vs. 17.0%/20.3%/11.6% in FY25/FY24/FY23). We reiterate a BUY rating on ZENT with a TP of INR640, implying a 17x FY28E EPS.

Our view: Near-term margins could be impacted by deal ramp-up investment

* Growth visibility improves with large deal but near-term growth and margins remain tight: ZENT’s revenue declined -1.3% QoQ CC, impacted by TMT weakness and delayed ramp-up of the mega deal (closed only in Feb). Management indicated that 1QFY27 is unlikely to see a further decline, with growth trajectory dependent on the pace of ramp-up of the ~USD210m deal (full run-rate only from 3QFY27). While order intake remains strong (ex-large deals at ~USD190-200m; BTB >1.1x), conversion into revenue will be gradual, given the transition timelines. We estimate an uptick in revenue in 2HFY27, with 1H likely softer with a modest growth of 1.0%/2.0% QoQ cc in 1Q/2QFY27.

* AI-led shift impacting pricing: Clients continue to prioritize cost optimization, with AI spends largely coming from existing ADM/testing budgets rather than incremental spend. We believe this is creating pricing pressure on legacy services, especially during renewals.

* Vertical mix remains uneven; TMT drag persists: TMT (weakest vertical) declined ~9.7% YoY in FY26 and continues to face structural pressure from insourcing and shift in spends toward AI infrastructure. Management does not expect recovery in the near term, with the top client (~6–8% of revenue) likely to remain a drag. BFSI remains steady and is expected to drive growth, while MCS is stabilizing, and HLS may remain flat amid client consolidation. Overall, we believe growth will remain dependent on nonTMT verticals, offsetting continued weakness in these verticals.

* Margins to see near-term pressure from large deal investments: EBITDA margins contracted ~130bp QoQ in 4Q, impacted by ~110bp reversal of leave benefits, ~110bp increase in SG&A (including deal-related costs), and ~30bp volume decline, partly offset by ~120bp forex tailwind. Management indicated that transition and hiring costs (already ~50–60bp impact in 4Q) will increase further in 1Q–2QFY27 before normalizing. While mid-teens margin guidance is maintained, we expect 1H pressure with a recovery in 2H as revenues ramp up. We build in EBITDA margins of 16.1% for FY27E

* Deal momentum strong but competitive intensity rising: Order book reached an all-time high in 4Q, with total intake up ~123% QoQ, supported by a ~USD210m mega deal (largest in company history). Ex-large deal intake stood at ~USD192–206m (vs. ~USD180m in 3Q), implying a book-to-bill above ~1.2x. That said, revenue ramp from large deals is phased (limited in 1Q, gradual in 2Q, meaningful from 3Q), and competitive intensity has increased with Tier-1 vendors participating more actively in similar deal sizes. Sustaining win rates and deal economics in a competitive environment will be key monitorables.

Valuation and change in estimates

* 4Q performance reflects continued demand unevenness, with TMT weakness and delayed deal ramp impacting growth, while margins saw early pressure from transition costs. The mega deal (~USD210m) provides better medium-term revenue visibility, though contribution will build gradually from 2Q and scale meaningfully only from 3QFY27.

* At the same time, AI-led reprioritization of spends is keeping pricing tight in legacy services, limiting near-term margin expansion. We cut our estimates by - 2.5%/-2.0% for FY27/FY28. We estimate EBITDA margins of ~16.1%/16.2% for FY27E/FY28. Our TP of INR640 is based on 17x FY28E EPS. We reiterate our BUY rating.

Revenues in line with our estimates and beat on margins; strong deal TCV wins (up 123% QoQ)

* ZENT’s revenue stood at USD158.4m, down 1.9% QoQ in CC terms, in line with our estimates of a 1.8% decline QoQ CC. Reported 4Q USD revenue was down 1.3% QoQ. For FY26, revenue was up 3.1% YoY to USD643.7m.

* BFSI grew 1.2% QoQ CC, while HLS/MCS declined 6.6%/3.9% QoQ CC.

* Deal TCV: Bookings came in at USD401.8m (up 122.9% QoQ/88% YoY), and the book-to-bill was 2.5x. For FY26, deal TCV stood at USD912.7m, up 17.8% YoY. ? EBIT margin was 14.7% (est. 13.8%), down 130bp QoQ. For FY26, EBIT margin was 14.5% (est. 14.3%), up 100bp YoY.

* In 4Q, total headcount reached 10,779 (flat QoQ). LTM attrition was 9.8%, up 30bp QoQ. Utilization was up 80bp QoQ at 84.3%.

* Adj. PAT of INR2,102m (down 4.1% QoQ/up 19.2% YoY) was above our estimate of INR1,602m. Adj. PAT for FY26 stood at INR7.9b (up 22% YoY), above our expectation of INR7.4b.

* The company declared an interim dividend of INR 12.6/share.

Key highlights from the management commentary

* While clients are willing to expand AI adoption, the majority of AI spend is being carved from existing ADM and testing budgets rather than being incremental, resulting in pricing pressure on legacy services.

* Macro conditions and AI-related rethinking are compressing overall budgets, though management does not yet see a systemic push-out in decision-making.

* Tier-1 vendors have expanded their pursuit perimeter meaningfully, now competing for deals they would not have pursued a few quarters ago.

* Sequential decline was primarily caused by two factors: continued weakness in the TMT vertical and the mega deal closing only in February, leaving no material revenue contribution in 4Q.

* The mega deal has a gross TCV of ~USD210m; ex-large deal order intake for the quarter stood at ~USD192-206m (vs. ~USD180m last quarter).

* A majority of AI spend continues to be repurposed from existing application development and testing budgets, exerting pressure on renewals and pricing.

* Mid-teens EBITDA margin guidance is maintained for FY27 as a whole; margin pressure in 1H is expected to normalize from 2HFY27 as the large deal reaches full revenue run-rate.

* TMT: Management expects TMT to remain under pressure for the next several quarters, with the top client budgeted for continuous decline as insourcing trends and internal cost-cutting intensify. Top TMT client, which has declined in revenue share to ~6-8% of total revenue, remains a known drag; management has not assumed any growth for this account in its internal plans.

Valuation and view

* 4Q performance reflects continued demand unevenness, with TMT weakness and delayed deal ramp impacting growth, while margins saw early pressure from transition costs. The mega deal (~USD210m) provides better medium-term revenue visibility, though contribution will build gradually from 2Q and scale meaningfully only from 3QFY27.

* At the same time, AI-led reprioritization of spends is keeping pricing tight in legacy services, limiting near-term margin expansion. We cut our estimates by - 2.5%/-2.0% for FY27/FY28. We estimate EBITDA margins of ~16.1%/ 16.2% for FY27/FY28. Our TP of INR640 is based on 17x FY28E EPS. We reiterate our BUY rating.

* 4Q performance reflects continued demand unevenness, with TMT weakness and delayed deal ramp impacting growth, while margins saw early pressure from transition costs. The mega deal (~USD210m) provides better medium-term revenue visibility, though contribution will build gradually from 2Q and scale meaningfully only from 3QFY27.

* At the same time, AI-led reprioritization of spends is keeping pricing tight in legacy services, limiting near-term margin expansion. We cut our estimates by - 2.5%/-2.0% for FY27/FY28. We estimate EBITDA margins of ~16.1%/ 16.2% for FY27/FY28. Our TP of INR640 is based on 17x FY28E EPS. We reiterate our BUY rating.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412