Neutral TATA Motors Ltd for the Target Rs 416 by Motilal Oswal Financial Services Ltd

Focusing on profitable market share growth IVECO acquisition to pivot business to global scale

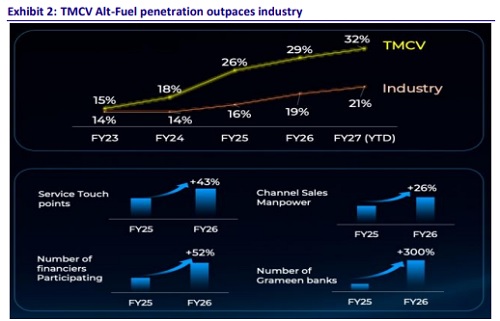

We attended the TMCV’s annual investor day wherein management outlined a roadmap for becoming a globally diversified, technology-led CV company, underpinned by profitable growth, market leadership and capital discipline. Management reiterated its confidence in the medium-term CV opportunity, driven by GDP-linked freight growth, rising logistics demand, electrification and continued expansion of the vehicle parc while maintaining its guidance of high single-digit industry growth in FY27 despite a moderation in volumes during the second half. The company expects strong doubledigit growth in 1Q and healthy momentum in 2Q. Key themes include sustaining leadership in trucks, a successful turnaround in the SCV-PU business, rapid progress in electric mobility and scaling downstream digital businesses. The proposed IVECO acquisition was highlighted as a transformational opportunity to accelerate global expansion, unlock sourcing and engineering synergies, and diversify earnings. Management also reiterated its aspiration of achieving sustainable double-digit EBITDA margins and increasing overall commercial vehicle market share toward 40% through growth in SCV-PU, buses, vans and ILMCV segments. The stock, trading at 21.7x FY27E EPS and 18.6x FY28E EPS, appears fairly valued. We reiterate our Neutral rating with a TP of INR416, valuing the core business at 12x FY28E EV/EBITDA.

Focus remains on profitable growth

Management unveiled its FY28 guidance for the CV business, aiming for market share improvement with continued focus on profitability.

FY28 guidance:

1) Increasing domestic CV market share to 40% from the current 35.7% with the bulk of improvement likely to come from SCV segment

2) Achieving double-digit EBITDA margin through a CV cycle and mid-teen margins in an uptrend

3) Spending 2-4% of revenue on investment

4) Generating FCF at 7-9% of revenue

5) Delivering RoCE of 30-35% after the IVECO acquisition (72% in FY26); and 6) growing non-cyclical business at 1.5x cyclical business

Management identifies three pillars for next phase of value creation

In order to accelerate value creation, management intends to focus on three pillars:

1) Strengthen the core – defend and grow domestic leadership with profitability in focus

2) Scale up new growth engines – lead India’s EV transition in CVs and grow downstream business and digitization initiatives to reduce business cyclicality

3) Strategic global pivot – expand international presence after the IVECO acquisition.

Valuation and View

Demand outlook for the domestic CV industry has turned cautious due to the recent geopolitical tensions and their potential impact on the Indian economy, with margins likely to remain under pressure in the near term. We now factor in a 6% CAGR in TMCV’s CV volumes over FY26-28. As a result, we estimate a CAGR of 8%/8%/10% in revenue/EBITDA/PAT over FY26-28E. The stock, at 21.7x FY27E and 18.6x FY28E EPS, appears fairly valued. Reiterate Neutral with a TP of INR416 per share, valuing the core business at 12x FY28E EV/EBITDA (in line with peers) and adding INR12/share for its stake in Tata Capital.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)