Buy Vinati Organics Ltd For Target Rs. 1,700 Motilal Oswal Financial services Ltd.

Capacity ramp-up in ATBS to drive earnings in FY27 Strong beat on estimates

* Vinati Organics (VO) reported a steady operating performance, with EBITDA at INR1.8b, remaining flat YoY (est. INR1.6b), and EBITDA margin expanding 170bp YoY despite fluctuations in raw material prices, logistics costs, and supply chain issues.

* Going forward, we expect revenue growth for Acrylamide Tertiary-Butyl Sulfonic Acid (ATBS) to be driven by volume growth, the ramp-up of Phase I expansion, and the commercialization of Phase II in Oct’26. Meanwhile, the phenol (BP) segment is expected to witness improving demand conditions, and the Isobutyl Benzene (IBB) segment is likely to post double-digit growth.

* We broadly maintain our earnings estimates for FY27/FY28 and value VO at 29x FY28E EPS to arrive at a TP of INR1,700. Reiterate a BUY rating on VO.

Steady growth led by an expansion in EBITDA margin

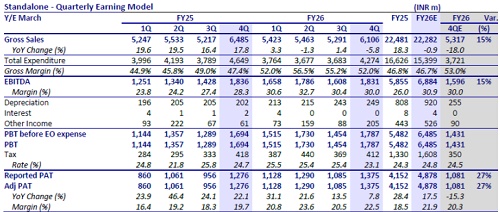

* Revenue came in at INR6.1b (est. of INR5.3b), declining 6% YoY but rising 15% QoQ.

* Gross margin stood at 52% (compared to 47.4% in 4QFY25 and 55.2% in 3QFY26).

* EBITDAM came in at 30% (+170bp YoY, -40bp QoQ).

* EBITDA stood at ~INR1.8b (est. of INR1.4b), remaining flat YoY but rising 14% QoQ.

* Adjusted PAT stood at INR1.4b (est. of INR1), rising 8% YoY and 27% QoQ.

* In FY26, revenue declined 1% YoY to INR22.3b, while EBITDA/Adj. PAT grew 18%/17% YoY to INR6.9b/INR4.9b.

* CFO stood at INR6.3b as of Mar’26, compared to ~INR5b as of Mar’25.

Valuation and view

* Veeral Organics (subsidiary) has commissioned a plant for MEHQ and Guaiacol, along with other products (Anisole, 4-MAP, etc.) in FY26. We expect them to be the key growth drivers for VO going forward.

* VO remains one of the largest producers of Anti-Oxidants (AO) in India. While Chinese competitors continue to pose a threat to supply, the long-term outlook for the segment remains positive on the back of a novel AO for lubricant additives, further strengthening of the portfolio.

* We expect the ATBS segment’s growth to be driven by the ramp-up of phase I (10,000 MTPA) capacity expansion and the commercialization of phase II (another 10,000 MTPA) in Oct’26, with higher utilization expected in FY28.

* We broadly maintain our earnings estimates for FY27/FY28 and expect a CAGR of 15%/13%/12% in revenue/EBITDA/PAT over FY26-28. The stock trades at ~22.4x FY28E EPS of INR59.4 and ~15.2x FY27E EV/EBITDA. We value the stock at 29x FY28E EPS to arrive at a TP of INR1,700. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041