Sell India Cements Ltd for the Target Rs. 350 by Motilal Oswal Financial Services Ltd

Beat led by strong operating performance

* India Cements (ICEM) reported EBITDA of INR1.6b (~37% beat) in 4QFY26 vs. INR11m in 4QFY25. EBITDA beat was led by all-round operating strength. EBITDA/t increased ~62% QoQ to INR498 (vs. est. INR396). OPM improved 5.5pp QoQ to ~13%. PAT (adj. for impairment of investment) stood at INR700m (vs. estimated INR193m) vs. a loss of INR618m in 4QFY25.

* ICEM capacity utilization has significantly improved in the past couple of quarters, standing at ~84% in 4QFY26 (up 11pp YoY). Realization/t (net of freight costs) grew ~6% YoY/3% QoQ to INR3,791. ICEM has committed a capex of INR20.0b over the next two years for capacity expansion (2.8mtpa) and efficiency improvement. It plans to increase the share of total RE power to ~80% by FY29 from ~6% currently. Power consumption/t of cement declined 8% YoY to 80.8 units in 4Q. The brand migration with UTCEM has been completed in Mar’26.

* We raised our EBITDA estimates for FY27/FY28 by ~7%/8%, factoring in higher benefits of cost efficiency initiatives and brand migration. We value ICEM at 14x FY28E EV/EBITDA to arrive at a TP of INR350. Maintain Sell.

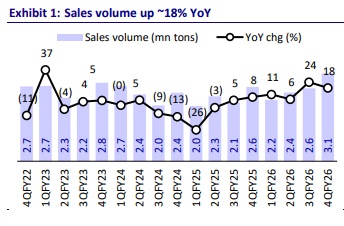

Volume up ~18% YoY; EBITDA/t at INR498 (est. INR396)

* ICEM’s revenue grew ~3% YoY to INR12.3b (in line) in 4Q. Volume rose ~18% YoY (~9% above estimate) to 3.1mt. Realization/t (net of freight cost) increased ~6% YoY/3% QoQ (~5% above our estimate).

* Opex/t dipped ~24% YoY (~14% below estimate), led by continuous costreduction initiatives. Variable cost/other expense per ton declined ~3%/21% YoY. EBITDA/t stood at INR498 vs. INR4 in 4QFY25. Depreciation was flat YoY, while interest cost declined ~39%. Other income was up 19% YoY. Adjusted PAT stood at INR700m vs. loss of INR618m in 4QFY25.

* In FY26, ICEM’s revenue grew ~10% YoY to INR44.8b. It posted EBITDA of INR4.0b vs. an operating loss of INR3.9b in FY25. Adj. PAT stood at INR567m vs. net loss INR7.4b in FY25. Volume grew ~15% YoY to 10.3mt. EBITDA/t stood at INR385. Net debt stood at INR12.7b vs. INR10.6b as of Mar’25.

Valuation and view

* ICEM is witnessing operational improvement under UTCEM’s leadership, with strong volume growth, margin improvement (led by cost efficiencies and better net plant realization), and the balance sheet strengthening. We estimate 11% revenue CAGR over FY26-28, led by volume/realization CAGRs of ~9%/2%. We estimate EBITDA CAGR at ~50%, albeit on a low base, and EBITDA/t of INR509/INR730 in FY27E/FY28E vs. INR385 in FY26. Net debt is estimated to surge to INR20.1b/INR19.1b in FY27/FY28 amid higher capex (est. cumulative capex of INR20.0b vs. OCF of INR16.5b over FY27-28).

* We believe the current valuation at 16x FY28E EV/EBITDA prices in most of operational improvements, which are expected due to this transition, and hence limit any further scope of re-rating. We value ICEM at 14x FY28E EV/EBITDA to arrive at our TP of INR350. Reiterate Sell.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)