2025-12-31 11:18:44 am | Source: Motilal Oswal Financial Services Ltd

Buy HPCL Ltd for the Target Rs. 590 by Motilal Oswal Financial Services Ltd

Diesel cracks easing; marketing leverage intact

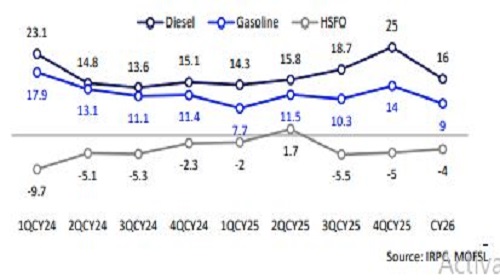

- HPCL’sstock price has increased ~20% over the last three months and is currently trading at 1.4x one-year forward P/B (vs LTA of 1.2x P/B). However, the stock has corrected 8% from its recent high over the last 15 days. The weakness is driven by a sharp decline in diesel gross marketing margin, which contracted 18% QoQ/46% YoY, as diesel cracks surged to as high as USD30/bbl (LTA: USD16/bbl). In a scenario where diesel cracks over Brent sustain at ~USD30/bbl, Brent averages USD63/bbl, and the INR/USD exchange rate stabilizes at INR89.4/USD, we estimate diesel gross marketing margin to decline 70% vs 2QFY26 margin. That said, diesel cracks have already started to correct, currently at ~USD22/bbl, which should help alleviate pressure on the stock.

- HPCL’s current valuation appearsreasonable, and we believe the stock should continue to perform well, as: 1) receipt of INR6.6b per month in LPG compensation over Nov’25- Oct’26 shall boost earnings; 2) a sharp decline in LPG under-recovery to INR30-40/cyl currently, vs ~INR135/cyl in 1HFY26, shall improve blended marketing margins; 3) midterm auto-fuel marketing margin outlook remains robust amid a weak crude price outlook (USD60/bbl in FY27/28); and 4)start-up RUF and HRRL, coupled with sustained strength in diesel cracks, would meaningfully boost refining earnings.

Near-term strength in diesel cracks; medium-term outlook remains balanced

- Refined product markets remain tight as elevated diesel/gasoil cracks reflect widespread refinery disruptions, including post-summer maintenance, unplanned outages, ~0.8mb/d cumulative product loss from refinery closures in CY25YTD in Atlantic Basin, and repeated strikes by Ukraine, which have curtailed Russian exports and temporarily removed ~1.1mb/d of Russian capacity. With global refinery downtime peaking at ~9.4mb/d in Oct’25 and Russia’s diesel export ban extending through CY25, near-term cracks are expected to stay above long-term averages. However, as maintenance cycles ease, new global capacity ramps up, and any progress in resolving the RussiaUkraine conflict enables Russian products to re-enter the market, cracks are likely to normalize. Over FY27-28, we maintain a neutral stance on refining, as expected net capacity additions broadly match refined-product demand growth, although delays in project start-ups or fresh outages could continue to support margins.

Marketing remains a preferred sub-sector

- Our positive stance on retail marketing is driven by: 1) our negative bias for crude oil prices (FY27-28E: USD60/bbl), 2) expectations of limited sharp cuts in retail prices of MS/HSD. These factors, along with a healthy ~4% marketing volume CAGR, should drive robust marketing profitability. LPG under-recovery per cylinder declined to INR30-40 in 3QFY26’TD (vs INR100+ over the last few quarters). Further, INR6.6b per month LPG compensation that the company will receive over Nov’25-Oct’26 will directly add to earnings. The anticipated crude oil surplus is expected to keep crude oil and propane prices lower, enhancing stability in marketing segment earnings.

Valuation and view

- We continue to prefer HPCL among OMCs due to the following factors: 1) HPCL’s higher leverage toward the marketing segment, 2) higher dividend yield as HPCL’s capex cycle is tapering off, and 3) start-up of HPCL’s multiple mega-projects in the next 12 months, providing a push to earnings.

- HPCL currently trades at 1.3x FY27E P/B. We estimate the company to deliver 29.3%/19.9% RoE during FY26/27 and project a 3.8% FY27E dividend yield. Our earnings assumptions remain conservative as we build in a refining GRM of USD6.5/bbl and an MS/HSD gross marketing margin of INR3.5/lit. We have not assumed any significant benefits from: 1) the start-up bottom-upgrade unit and 2) Project Samriddhi, which has unlocked savings worth USD0.5/bbl in 1HFY26. We reiterate our BUY rating on the stock with our SoTP-based TP of INR590

Refining margin strength to sustain in the near-to-mid term

- Diesel and gasoline cracks have surged recently, averaging USD27/16 per bbl in Nov’25, vs LTA of USD16/12.6 per bbl. The strength in cracks is driven by recent refinery shutdowns, scheduled post-summer maintenance, unplanned outagerelated repairs, ~0.8mb/d cumulative product loss from refinery closures in CY25YTD in Atlantic Basin, and Ukraine’s strikes, which have disrupted Russia’s product exports. According to Thai Oil, a Southeast Asia-based refiner, Ukrainian attacks have disrupted 1.1mb/d of Russian refining capacity (~17%/~1% of Russia’s/global refining capacity). According to S&P Global, global refinery downtime in Oct’25 stood at 9.4mb/d, up 1.5/0.6 mb/d MoM/YoY, leading to tighter refined-product supply. Russia’s ban on Diesel exports till CY25-end to counter domestic fuel shortages (link) has further added to the global diesel shortage.

- While product cracks are expected to remain robust (above the LTA) in the nearterm, given the upcoming EU sanctions on the import of Russian refined products from Jan’26 (link) and recurring attacks on Russian refineries by Ukraine (link), we expect cracks to soften as planned refinery maintenance concludes globally and new capacities begin. According to recent media articles, Russia has seen the latest copy of a US plan to end the Ukraine war. We highlight that a resolution would likely allow Russian diesel to re-enter markets more freely, potentially leading diesel cracks to normalize to USDxx/bbl levels or even lower.

- Further, we reiterate our neutral stance on refining over FY27-28 as net refinery capacity addition over CY25-27 (~1.35mb/d) remains in line with the expected growth in refined product demand during the period (~1.32mb/d) (S&P Global estimates). However, delays in refinery start-ups or announcements of new shutdowns can support stronger margins.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

Disclaimer:

The content of this article is for informational purposes only and should not be considered financial or

investment advice. Investments in financial markets are subject to market risks, and past performance is

not indicative of future results. Readers are strongly advised to consult a licensed financial expert or

advisor for tailored advice before making any investment decisions. The data and information presented

in this article may not be accurate, comprehensive, or up-to-date. Readers should not rely solely on the

content of this article for any current or future financial references.

To Read Complete Disclaimer Click Here

Latest News

Quote on Markets by Mr Avinash Agarwal, Senior Vice ...

Uttar Pradesh continues to play a pivotal role in th...

Research report on Manthan- Oil & gas by Swarnendu B...

Market Round-up - 11th August 2026 by Motilal Oswal ...

India's Q1 FY27 GDP growth likely to near 8 pc amid ...

Buy Dalmia Bharat Ltd For Target Rs. 2,278 By Geojit...

Evening Roundup : Daily Evening Report on Bullion, B...

NASA invites ISRO to join Moon Base Programme as Ind...

Buy Suzlon Energy Ltd For Target Rs.56 By Geojit Fin...

India's merchandise exports touched record high at $...