Buy Aditya Birla Capital Ltd for the Target Rs. 250 by Motilal Oswal Financial Services Ltd

Strong growth in HFC AUM; NBFC NIM to improve hereon

Consol. PAT grew 6% YoY; unsecured MSME segment seeing stress

* Aditya Birla Capital (ABCAP)’s 4QFY25 consolidated revenue grew 13% YoY to ~INR141b and consolidated PAT grew ~6% YoY to ~INR8.65b. FY25 consol. PAT grew ~8% YoY to INR31.4b.

* The amalgamation of Aditya Birla Finance (ABFL) with Aditya Birla Capital has been successfully completed after obtaining all requisite approvals. The appointed date of the amalgamation is 1st Apr’24, and the effective date is 1st Apr’25. Post-amalgamation, ABCAP operates under two business segments: the NBFC lending business and the investment business, through which it holds investments in its subsidiaries, JVs, and associates.

* Management shared that the amalgamation has resulted in the release of ~INR30-35b of capital, which is expected to support the company’s growth ambitions for the next 12-18 months.

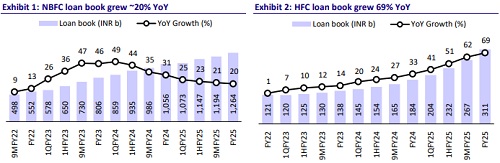

NBFC: AUM up ~20% YoY; NIM contracts ~10bp QoQ

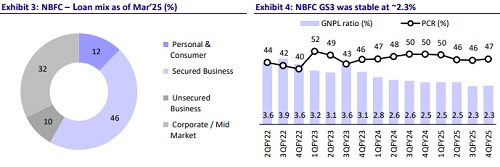

* NBFC Loan book grew ~20% YoY and 6% QoQ to ~INR1.26t. 4QFY25 disbursements grew ~8% YoY and 28% QoQ to ~INR195b. Loans to Retail, SME and HNI customers constitute 64% of the total loan portfolio.

* Management remains confident of delivering robust loan growth, targeting a ~25% CAGR in the overall portfolio over the next three years, with a target to double the loan book within this period. The company expects all business segments to register growth in FY26, with a continued increase in the contribution from the retail and MSME segments.

* Asset quality improved QoQ, with GS2 + GS3 assets declining ~50bp QoQ to ~3.8%.

* NIM contracted ~10bp QoQ as yields compressed due to a reduction in personal and consumer (P&C) loans to 12% (PY: ~17%). Management highlighted that the P&C segment has now stabilized and is expected to grow going forward, which should lead to an expansion in yields and NIMs in the subsequent quarters.

HFC: Robust growth in HFC AUM; GS2+GS3 declines ~35bp QoQ

* HFC disbursement jumped ~98% YoY to ~INR58.2b and loan book grew 69% YoY to ~INR311b.

* Management expects the current business momentum to sustain and has guided for a significant improvement in RoA to ~2.0-2.2% over the next 8- 10 quarters. This improvement is expected to be driven by better operating leverage, partially offset by a decline in NIMs, while credit costs are expected to remain broadly stable.

* NIM was largely stable QoQ at ~4.05%. RoA/RoE stood at 1.45%/11%

* Asset quality improved with GS3 declining ~33bp QoQ to ~0.66%. PCR rose ~15pp QoQ to ~55%.

Asset Management: QAAUM rose ~15% YoY

* The mutual fund quarterly average AUM (QAAUM) rose 15% YoY to INR3.82t. Individual monthly average AUM grew by 6% YoY to INR1.84t as of Mar’25.

* The domestic equity mix stood at ~44.3% (PQ: ~46.8%). Monthly SIP inflows grew ~5% YoY to ~INR13.2b in Mar’25.

Life Insurance: Individual FYP grew ~34% YoY; 13th month persistency rose to 88%

* Individual FYP grew 34% YoY to ~INR41b in FY25, while renewal premium grew 14% YoY.

* Net VNB margin stood at ~18% in FY25. 13M persistency rose to ~88% in Mar’25. Management has guided for a ~20-22% CAGR in individual FYP over the next three years, with a continued focus on expanding the VNB margin beyond 18%.

Health Insurance: Market share among SAHIs improves

* GWP in the health insurance segment grew 33% YoY to ~INR49.4b. The combined ratio improved to 105% (from ~110% YoY).

* ABHI’s market share among standalone health insurers (SAHIs) rose from 11.2% in the previous year to 12.6% in Mar’25.

Highlights from the management commentary

* The company is exploring collaborations with select marquee digital platforms, where sourcing will be driven by partners, while ABCL will manage underwriting and collections.

* Udyog Plus, the company’s comprehensive B2B ecosystem platform, has continued to scale rapidly, reaching an AUM of over INR35b in less than two years since its launch. Notably, the ABG ecosystem contributes ~50% of the disbursements on the Udyog plus.

Valuation and view

* ABCAP continued to exhibit an improvement in operational metrics in 4QFY25. Loan growth remained healthy across both the HFC and NBFC segments, accompanied by a further improvement in asset quality. While NIMs in the NBFC business witnessed some contraction during the quarter, management has guided for NIM improvement in the subsequent quarters, supported by a favorable shift in its product mix.

* We expect a consolidated PAT CAGR of ~24% over FY25-27E. The thrust on cross-selling, investments in digital, and leveraging ‘One ABC’ will lead to healthy return ratios, even as we build in a consolidated RoE of ~14% by FY27. Reiterate BUY with an SoTP (Mar’27E)-based TP of INR250.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412