Neutral KFin Technologies Ltd for the Target Rs.1,200 by Motilal Oswal Financial Services Ltd

PAT below est. due to lower-than-expected revenue

* KFin Technologies (KFin) reported a 15% YoY growth in operating revenue to INR2.7b in 1QFY26 (9% miss), led by 17%/24%/34% YoY growth in domestic MF solutions/issuer solutions/international solutions segments.

* Total operating expenses grew 16% YoY to INR1.6b (8% lower than expectations), with employee expenses growing 17% YoY to INR1.1b (in-line) and other expenses rising 15% YoY to INR485m (22% below expectations). The cost-toincome ratio was at 58.5% (58% in 1QFY25).

* KFin’s EBITDA grew 14% YoY to INR1.1b (10% miss), with EBITDA margin at 41.5% (42% in 1QFY25). It posted a net profit of INR773m, up 14% YoY (13% miss) in 1Q.

* Management expects yield compression to normalize to 3–3.5% YoY going forward and maintain a consistent sequential trend for the next three quarters. The non-mutual fund business (ex-global business) is anticipated to sustain a growth trajectory of 30-35%.

* We cut our earnings estimates for FY26/FY27 by 2% each, considering the decline in MF yields and lower revenue from issuer solutions and international business in 1QFY26. We expect KFin’s revenue/PAT to post a CAGR of 15%/17% over FY25- 27. We reiterate our Neutral rating on the stock with a one-year TP of INR1,200, premised on a P/E multiple of 45x on FY27E earnings.

Equity AAUM share stable; yields dip

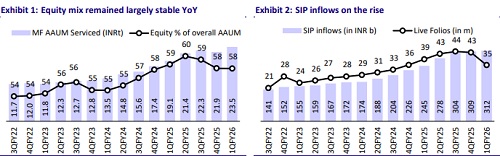

* KFin’s total MF AAUM serviced during the quarter rose 23% YoY to INR23.4t. Equity AAUM, at 58% of total MF AAUM, grew 22% YoY to INR13.6t, reflecting a market share of 33% (33.4% in 1QFY25).

* Strong net flows with stable market share offset by a slight decline in yield to 3.5bp in 1QFY26 resulted in a 17% YoY growth in revenue from the domestic MF business to INR2b (in-line). This segment contributed 75% to the overall revenue in 1QFY26 (73% in 1QFY25).

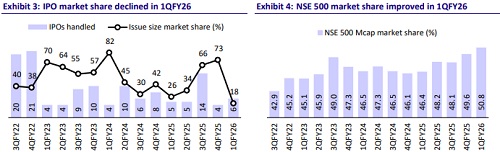

* In the issuer services business, the main board IPO market share (concerning issue size) declined YoY to 18% in 1QFY26 (from 26.3% in 1QFY25). KFin handled six IPOs during the quarter (five in 1QFY25), resulting in a 24% YoY revenue growth from issuer solutions to INR330m (29% miss). The segment contributed 12% to the overall revenue (11% in 1QFY25).

* In the international investor solutions business, the number of clients reached 82, taking the total AUM serviced to INR864b. Revenue from this segment grew 34% YoY to INR366m, contributing 13% to overall revenue (11% in 1QFY25).

* In the alternates and wealth business, Kfin’s market share stood at 37% with an AUM of INR1.6t. NPS market share continues to rise and was at 9.9% in 1QFY26 (8.4% in 1QFY25), with an AUM of INR582b.

* The non-domestic mutual fund revenue contributed 26.5% to the overall revenue, down from 27.7% in 1QFY25. The value-added services contributed ~7% to its revenue.

* Other income grew 24% YoY to INR100m (in line).

Key takeaways from the management commentary

* KFin launched its KRA platform during the quarter and signed up five clients within just two weeks, marking a swift go-to-market execution.

* Yields declined ~5% YoY (vs. an average of 3–4%), driven by telescopic pricing and volume-linked discounts to fast-growing AMCs. Additionally, the growing share of passive products contributed ~20% to the dip.

* Ascent’s EBITDA margin remained subdued due to continued investments in senior hiring across global markets. However, profitability is expected to improve meaningfully with future large contract wins. Post-integration, Ascent’s margin profile is expected to be similar to or better than KFin’s, leveraging the latter’s strong productivity and execution capabilities.

Valuation and view

* Structural tailwinds in the MF industry are expected to drive absolute growth in KFin’s MF revenue. With its differentiated ‘platform-as-a-service’ model offering comprehensive, end-to-end solutions powered by proprietary technology, KFin is well-positioned to capitalize on strong growth opportunities in both Indian and global markets.

* We cut our earnings estimates for FY26/FY27 by 2% each, considering the decline in MF yield and lower revenue from issuer solutions and international business in 1QFY26. We expect revenue/PAT to post a CAGR of 15%/17% over FY25-27E. We reiterate our Neutral rating on the stock with a one-year TP of INR1,200, premised at a P/E multiple of 45x on FY27E earnings.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412