Buy Time Technoplast Ltd for the Target Rs. 289 by Motilal Oswal Financial Services Ltd

Robust outlook; attractive valuation

- We remain upbeat on the robust prospects of Time Technoplast (TIME) and expect healthy returns on the stock, which is currently trading at an attractive valuation of ~15x FY27E P/E.

- The company is working on several new products that are either under development or in advanced stages of OEM approvals, offering significant growth potential.

- The recent fundraise of INR8b will be used towards growth capex and debt reduction, further enhancing the company’s prospects.

- Management guidance of over 15% volume growth and a higher growth in PAT for the next few years remains intact, driven by a 20-30bp margin expansion annually and savings on finance costs.

- The company also targets an RoCE expansion to 20% in FY26 from ~18% in FY25; RoCE is likely to rise 2% per annum thereafter.

- Capex of 600 composite CNG cascades is scheduled to be commissioned in 4QFY26, taking the total capacity to 1,080 units, with a revenue potential of INR8b.

- Discussions with auto OEMs are ongoing to supply individual cylinders for cars and buses. This is an untapped market currently.

- Driven by a robust outlook and attractive valuation, we reiterate our BUY rating on TIME with a TP of INR289, based on 22x FY27E P/E. Our TP implies an upside potential of 44%.

Healthy performance continues

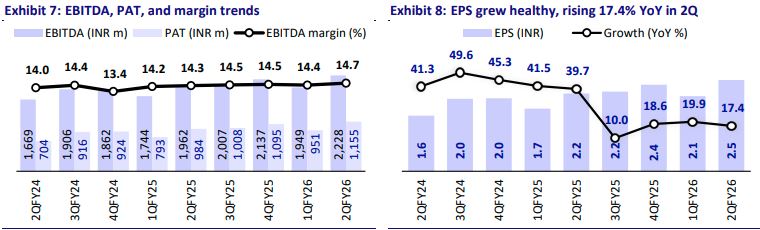

TIME reported an in-line 2Q, with volume growth of 14% YoY and revenue growth of 10% YoY, driven by an 18% YoY growth in value-added products (VAP; 18.7% EBITDA margin). Overseas operations (volume/revenue up 16%/13%; 35% of the mix) outperformed India (volume/revenue up 13%/9%). EBITDA margin came in healthy at 14.7%, and PAT rose 17% YoY to INR1.2b. Established products’ revenue grew 7% YoY and delivered a 13.1% EBITDA margin.

VAP mix on track to reach 35% over the next 2-3 years

VAP, a high-margin business for TIME with 20-30% revenue CAGR and over 18% margin, grew 18% YoY in 2Q. EBITDA margin remained strong at 18.7%. The revenue mix increased to 30% in 2Q (vs. 27% in FY25), led by 24% YoY growth in composite products, mainly CNG cascades. Management targets a 35% mix in 2-3 years, which is expected to drive TIME’s consolidated EBITDA margin to over 15%.

Recent fundraise to be used towards growth capex and debt reduction

TIME raised INR8b recently via QIP, which is expected to be used towards growth capex and debt reduction. This further enhances the company’s prospects. Of the total proceeds, INR4b will be used for debt repayment, leading to interest cost savings of ~INR350m per annum from FY27. The remaining amount will be allocated towards inorganic growth, automation capex (INR900m), and the setup of recycling plants (INR550m). TIME’s transition to 75% green energy over the next two years is expected to save INR300m per annum from FY27. The company plans to invest INR1.2b over three years in recycling units, with Phase 1 (Western region) set to be commissioned by Jan’26, followed by a unit in North India.

New products under development offer significant growth potential

TIME is working on several new products that are either under development or in advanced stages of OEM approvals, offering significant growth potential. Composite fire extinguishers for railways are slated to launch in 4QFY26. Pilot runs of hydrogen cylinders for drone applications are likely to conclude by Dec’25. 14.2kg composite LPG cylinders are under development in consultation with IOCL/HPCL. Moreover, to expand its product offerings in FIBC packaging, TIME has signed an MoU to acquire a 74% stake in Ebullient Packaging for INR1.5b, with due diligence currently ongoing. BIS approval for HDPE pipes in gas distribution and approval from the International Center for Automotive Technology for E-rickshaw batteries are also expected to generate revenue in the near future.

Strong guidance intact; composite CNG cascade capacity to double in 4Q The guidance of over 15% volume growth and a higher growth in PAT for the next few years remains intact, driven by a 20-30bp margin expansion annually and savings on finance costs. It also targets ROCE to expand to 20% in FY26 from ~18% in FY25 and rise by 2% per annum thereafter. Capex of 600 composite CNG cascades will conclude in 4QFY26, taking the total capacity to 1,080 units, with INR8b revenue potential. Discussions with auto OEMs are ongoing to supply individual cylinders for cars and buses (an untapped market currently).

Valuation and view: Reiterate BUY with INR289 TP (44% upside)

After posting a CAGR of 16%/19%/39% in revenue/EBITDA/PAT over FY21-25, we expect a CAGR of 15%/16%/23% over FY25-28, to be fueled by its strong performance in the VAP segment. Pre-tax RoCE and RoIC are expected to expand from ~18.2% each in FY25 to ~23% and 25% in FY28, respectively, led by healthy operating performance, improved plant efficiency, and tightening of the net working capital cycle. Driven by a robust outlook and attractive valuation (~15x FY27E P/E), we reiterate our BUY rating and a TP of INR289 (44% upside potential), based on 22x FY27E P/E

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412