Buy Tata Power Ltd for the Target Rs. 455 by Motilal Oswal Financial Services Ltd

Mundra SPPA and RE execution key drivers in FY27

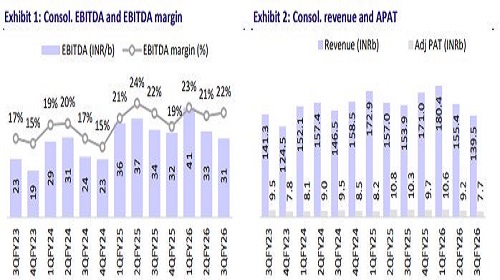

* Weak 3Q amid Mundra shutdown: Tata Power (TPWR) reported a 3QFY26 APAT of INR7.7b, indicating a 20% miss vs. our est. The weaker-thanexpected performance was primarily attributable to the standalone business, which reported a PAT loss of INR1.6b during the quarter due to the Mundra plant remaining shut. In contrast, profitability at TPDDL improved sharply, supported by the receipt of INR3.4b towards past-period tariff recoveries. Reported EBITDA was INR30.5b, which was 4% below our est.

* Key things we liked about the result: 1) the Odisha distribution business continues to report a stellar improvement in profitability on a YoY basis driven by lower ECL charges and improved cash collections; 2) management guided that the company is close to finalizing the Mundra SPPA with the Gujarat government, and the plant could potentially restart by the end of FY26; 3) cell and module assets continue to operate at industry-leading scale with a yield of ~95%; and 4) rooftop earnings momentum remains strong, with 9MFY26 EBITDA up 2.7x YoY.

* Key monitorables: Finalization of the Mundra SPPA and restart of the plant by the end of FY26. While its own RE commissioning was weak at 559MW in 9mFY26 (FY26 target: 1.1GW), this should pick up in FY27 as third-party installation will significantly decline.

* Key changes to our earnings estimates: We cut our FY26E/FY27E PAT by 4%/3% to account for the potential closure of the Mundra plant in 4QFY26 and a slower-than-expected pace of its own RE commissioning. We cut our EV/EBITDA multiple for the renewable business to 12x (vs. 14x earlier).

* Valuation and view: The valuation of TPWR is segmented across various business units. The regulated business is valued using a 2.5x multiple on regulated equity; the coal segment is valued at 1x book value; the renewables segment is valued at 12x FY28E EBITDA; the pumped storage segment and other segments are valued at 1x PB; and for cash and investments, we add INR37/share. The sum of these contributions results in a TP of INR455/share.

Result below our estimates; Mundra shutdown affects performance Financial Performance

* TPWR reported revenue at INR139.5b (-9% YoY, -10% QoQ), missing our estimates by 23%. The miss was attributed mainly to the continued shutdown of the Mundra plant.

* TPWR posted an EBITDA of INR30.5b (-9% YoY, -7% QoQ), which missed our estimates by 4.3%. The EBITDA margin was 21.9% vs. the projected 17.6%.

* APAT was INR7.7b (-25% YoY, 16% QoQ), missing our estimates by 19.7%.

Operational Performance

* TPWR commissioned 919MW RE capacity, including 357MW own projects and 562MW of third-party EPC.

* It installed ~0.57m smart meters and added 372MWp rooftop capacity in 3Q.

* The company’s total portfolio now stands at 26.3GW, with 16.3GW operational and 10.0GW under construction.

* TPWR’s module manufacturing arm produced 990MW and 962MW of solar modules and cells, respectively.

* TPWR has an order book of INR11.7b for their rooftop EPC and a utility scale order book of INR9.2b

Highlights of the 3QFY26 performance

* During 3QFY26, new businesses scaled up well, with the Cell & Module manufacturing segment reporting a sharp improvement in profitability and rooftop solar execution rising to 372MW vs. 173MW in 3QFY25; rooftop solar PAT increased to INR1.1b from INR0.6b YoY.

* The Odisha discom business delivered a strong turnaround, with PAT increasing to INR2.26b from INR0.8b last year.

* Delhi distribution performance improved, with higher EBITDA aided by a one-off FY23 tariff true-up, contributing ~INR3.44b to PAT in 3QFY26.

* Losses from the Mundra plant shutdown, estimated at ~INR8b over nine months due to foregone capacity charges, were partly offset by stronger performance in Delhi distribution and rooftop solar; a similar regulatory impact was seen in the same quarter last year.

* The Mundra power plant did not operate in 3QFY26; however, SPPA discussions with the Gujarat government are nearing completion, and the plant is expected to restart ahead of summer demand, with similar arrangements planned with other states.

* The renewable energy pipeline stands at 5.2GW, with 2.5-3.0GW targeted for commissioning next year (around 50% solar); an additional 400–500 MW is nearing completion this quarter (9MFY26: 559 MW), and third-party EPC activity is largely tapering off. ? In solar manufacturing, module sales totaled 960 MW (including 168 MW under ALMM), with increasing use of in-house cells.

Valuations

* The valuation of TPWR is segmented across various business units, leading to a TP of INR455/share.

* Regulated business is valued using a 2.5x multiple on regulated equity.

* The coal segment is valued at 1x book value.

* The renewables segment is valued at 12x FY28E EBITDA.

* The pumped storage segment and other segments are valued at 1x PB. For cash and investments, we add INR37/share.

* The sum of these contributions results in a TP of INR455/share, reflecting the comprehensive valuation of TPWR’s diverse business segments.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412

.jpg)

Tag News

Tata Power Company rises on getting LoA from SECI to provide pumped storage services