Buy Raymond Lifestyle Ltd for the Target Rs. 1,500 by Motilal Oswal Financial Services Ltd

Weak quarter; demand recovery key for re-rating

* Raymond Lifestyle’s (RLL) reported tepid performance as the weak consumer sentiment was further exacerbated by a ransomware attack impacting revenue/EBITDA by ~INR2.5b/INR 0.7b.

* Although the overall demand environment remains challenging, there are signs of improvement, with stronger secondary sales and a 12-13% increase in autumn bookings.

* After the recent correction (down 51% YTD), RLL’s valuation appears attractive at ~21x FY26E PE or 1.3x FY26 EV/sales. However, we believe improvement in execution and sustained growth recovery remain the key for re-rating of the stock.

* We cut our FY26E EBITDA by ~5%, while our FY27E EBITDA is broadly unchanged. However, due to higher finance costs, we cut our FY26-27E EPS by 6-13%.

* We value RLL at 22x on Mar’27E P/E to arrive at our TP of INR1,500. We reiterate our BUY rating on RLL, primarily due to reasonable valuations.

Performance weaker than our muted expectations

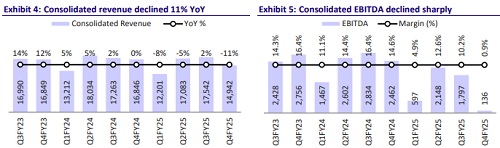

* RLL’s consol. revenue was down 11% YoY to INR15b (-15% QoQ) in 4Q.

* Revenue was significantly impacted by continued weak consumer demand, high inflation, and operational disruptions caused by a ransomware attack.

* RLL opened 35 new stores in 4Q, taking its total retail store network to 1,688.

* Gross profit declined 20% YoY (-16% QoQ) to INR6.2b (in line) as gross margins contracted by 455bp YoY to 41.8%.

* EBITDA declined sharply to INR135m (vs. INR2.5b YoY and our est. of ~INR770m) due to operating deleverage, adverse sales mix, and investments in retail store expansions.

* EBITDA margin was ~1% (vs. 14.6% in 4QFY24 and our est. of 5.3%).

* Depreciation and amortization increased 30% YoY, while finance costs jumped 13% YoY.

* Other income doubled YoY (2.1x of our estimate), led by subsidy benefits in the high-value shirting segment.

* Despite higher other income, the company reported a loss of INR450m (higher than our est. of ~INR120m).

* As per RLL, it has once again become a net debt-free company (vs. INR5.7b net debt in 2Q). This was likely driven by better secondary sales and consequent improved collections in 3QFY25.

FY25 a challenging year

* Consol. revenue declined 5% YoY to INR61.7b, driven by weaker customer demand, especially in branded textiles (-13% YoY).

* RLL opened 170 new stores (including 128 EBOs) in FY25, taking the total retail store network to 1,688 stores (up 11%). The company opened 38 EBOs of Ethnix by Raymond in FY25, taking the total store count to 152.

* Consol. EBITDA declined sharply by 50% YoY to INR4.7b, due to operating deleverage, adverse sales mix, and investments in retail network expansions.

* For FY25, RLL reported a modest PAT of INR382b (vs. INR4.8b YoY).

* Net working capital (NWC) days stood at 80 in FY25 (vs. 78 as of Mar’24 end). The impact of inventory stocking (up by 7 days to 104) in the retail and distribution network was offset by higher payables (up by 6 days to 78).

* OCF declined 46% YoY to INR5.3b, while FCF outflow stood at INR1.4b (though improved on INR5.1b outflow as of 1HFY25).

* RLL reported net cash of INR0.9b (vs. net cash of INR0.2b at end-Mar’24).

Highlights from the management commentary

* Demand environment: Weak demand persisted throughout FY25 due to inflation and lower discretionary spending, but signs of recovery are emerging with improved secondary sales and 12-13% YoY growth in AW2025 bookings. EBOs and LFS saw better sales in March–May.

* Ethnix: It surpassed INR1b in revenue in FY25 despite weak consumer demand and fewer weddings, with a focus on expanding through franchisee-led stores to optimize profitability. However, some stores have underperformed, extending break-even timelines to 36-40 months (vs. 24 months planned earlier).

* Garmenting: Profitability in 4Q was hurt by global uncertainties, price renegotiations, an adverse sales mix, and higher manpower training costs. The UK FTA is expected to enhance cost competitiveness, with UK revenue projected to rise from 20-22% to 30-40% over the next two years.

* Guidance: Raymond Lifestyle expects revenue growth of 10-15%+ in FY26, driven by demand recovery, dealer restocking, and easing inflation. Profitability is set to recover strongly as scale improves and store performance stabilizes. Steady-state margins are targeted at 20–22% for Branded Textiles and 14–15% for the overall business

Valuation and view

* FY25 was a challenging year for RLL, driven by lack of wedding days in 1H and impact of ransomware and overall weak discretionary environment in 2H. We expect growth recovery in FY26-27 (on a low base).

* After the recent correction (down 51% YTD), RLL’s valuation appears attractive at ~21x FY26E PE or 1.3x FY26 EV/sales. However, we believe improvement in execution and sustained growth recovery remain the key for re-rating .

* We cut our FY26E EBITDA by ~5%, while our FY27E EBITDA is broadly unchanged. However, due to higher finance costs, we cut our FY26-27E EPS by 6-13%.

* We value RLL at 22x on Mar’27E P/E to arrive at our TP of INR1,500 (earlier INR1,600). We reiterate our BUY rating on RLL, primarily due to reasonable valuations.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412