Buy Orient Electric Ltd For Target Rs. 274 By Yes Securities Ltd

Stock price correction overdone; reiterate BUY

Result Synopsis

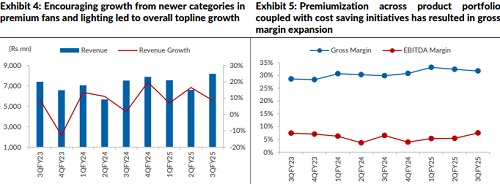

Orient Electric (ORIENTEL) revenue growth of 8.6% was 4.9% lower than our estimates. ECD has witnessed lower than expected growth, with ECD revenue growing 7.3% yoy, while lighting revenue grew 11.9% yoy despite pricing challenges on B2C consumer lighting side. Sluggish demand post the festive season and delayed start to winters impacted ECD growth. On the gross margin front various actions taken by the company is bearing fruits resulting in higher gross margin. Gross margin stood at 31.7% showing expansion of 184bps. EBITDA margin has improved on both yoy and sequential basis, it’s still lower than estimates as employee cost has shot up 18% as company hired various mid-level and toplevel management as it is gearing for strong growth. The company has also started to manufacture ceiling fans in the Hyderabad plant and ramp up is underway as company gets ready for the summer season. ORIENTEL is targeting to grow faster than the industry in the medium term as investments are being made to achieve strong growth. On the margin front company expects margin to be in high single digit in Q4 and it has endeavor to reach double digit margins which it believes can achieve in Q1FY26 if summer continues to remain strong. Given the investments that company is undertaking for strong growth in domestic markets and new exports opportunity we expect company to deliver industry leading growth with margins improving from next fiscal. We continue to remain positive on the stock and reiterate our BUY rating with PT of Rs274 valuing 33x on FY27. We believe stock has over corrected and at CMP it provides excellent entry point for medium to long term investment..

We are anticipating revenue CAGR of 13%, and EBITDA and PAT CAGR of 32% and 33% respectively for FY24-27E. We have modelled EBITDA margins to be ~8.3% in FY27 which we believe can be achieved given the work the company has on the cost savings. ORIENTEL is expected to outperform peers and could lead to further market share gains. We believe if strategy executed well could result in strong growth in medium term.

Result Highlights

* Quarter Summary -Revenue missed estimates as demand has been sluggish post the festive season and and there has been delayed start to the winter. The company has gained market share in B2C consumer lighting.

* ECD Segment – ECD segment has seen growth of 7.3% yoy driven by new product launches and premiumization. BLDC Fans has registered 60% growth vs last year. Hyderabad plant operations have stabilized contributing to the growth.

* Margins – Gross Margin has expanded by 184bps YoY, it is expected to sustain at ~31-33% range, with improvement in product mix, channel optimization with DTM, and premiumization across product categories. EBITDA Margin improved to 7.5% due to Spark Sanchay and other cost optimization initiatives.

* Lighting– Lighting segment saw an increase in share of luminaries on back of premiumization and strong traction in B2B, with execution of key projects in Street Lighting

Please refer disclaimer at https://yesinvest.in/privacy_policy_disclaimers

SEBI Registration number is INZ000185632