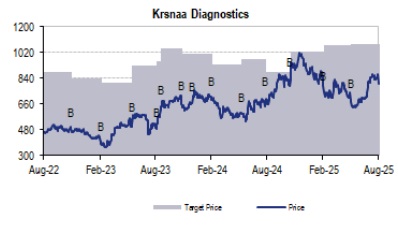

Buy Krsnaa Diagnostics Ltd for the Target Rs. 1,127 by JM Financial Services Ltd

Krsnaa’s 1Q revenue/EBITDA/PAT grew 13%/20% /14% YoY, which was 6%/8%/15% miss on our estimates. The EBITDA margins came in at 26.6%, up 157bps YoY, but, missed our estimates by 70bps. Retail and Rajasthan wins are the key positive takeaways from the quarter. On the Retail front, revenue grew 8x YoY led by the B2C segment, thus bringing the company a step closer to realising it retail aspirations. This strong Retail growth was enabled by a 7x YoY growth in the number of touch points. During the quarter, the much awaited Rajasthan NHM contract finally materialised. This is a 5 year contract, with revenue meaningful revenue materialization anticipated from FY27, and will be amongst the largest PPP diagnostics projects in India. To factor in the same, we have revised our future estimates upwards. Krsnaa is one of the most uniquely placed amongst its peer set of listed players, leveraging the PPP infra to offer services at a fraction of the competitor’s prices. We believe the ramp-up of Retail segment, execution of Rajasthan NHM project and future tender wins will enable the revenue, EBITDA and PAT to grow at a CAGR of 24%, 24% and 34% over FY25-28, respectively. This makes Krsnaa one of the fastest growing diagnostics player in the Indian listed space. We continue to value the company at 24x its June’27 EPS to arrive a TP of INR 1,127. Maintain Buy.

* Key metrics: The YoY growth was driven by sustained momentum in both radiology and pathology. With the Himachal and Karnataka receivables starting to come in, the receivable days are at ~120. The company reported a 3% YoY increase in number of tests performed, however, 1QFY25 included the BMC contract and thus making the growth seem muted. On a YoY basis, there is 134% increase in number of Pathology labs and 41% increase in number of Radiology labs. In 1Q, Krsnaa established 75 new centers.

* Retail: On a YoY basis, the Retail revenue grew 7.9x, now contributing 6% to the topline (vs 1% in 1QFY25). The growth was enabled a 6.7x growth in the number of touchpoints, now at 2,414 vs 362 in 1QFY25. The composition of Retail too has developed on a positive note, with B2C now contributing 66% to the segmental mix (vs 10% in 1QFY25)

* Rajasthan: The much awaited National Health Mission (NHM) tender finally materialised. Under the same, Krsnaa will be establishing 42 state-of-the-art Mother Labs, 135 Satellite Labs, and over 1,300+ Collection Centers. All targeted for operation by FY26, with meaningful revenue materialising for FY27. The tender is of 5 year in duration from commercialization and the management guided for an annual INR 3-3.5bn top-line contribution from the same. This will primarily be a pathology project and is one of the largest and most comprehensive PPP diagnostic project even undertaken in India. The estimated CAPEX for the project will range between INR 2-2.5bn.

* Future growth strategy: The company reiterated its strategy of – aggressively pursuing high-potential tenders across multiple states, expanding into new geographies through both PPP & fast-growing retail vertical, and strengthening pipeline to sustain momentum.

* Financial Highlights:

- Revenue at INR 1.9bn (-6% vs JMFe) and is +13% YoY

- Gross Profit of INR 1.5bn, +14% YoY, with gross margin at 75.4%% (-181bps vs JMFe; +63bps YoY)

- EBITDA at INR 514mn (-8% vs JMFe) and is +20% YoY

- EBITDA Margin at 26.6% (-67bps vs JMFe) and is +157bps YoY

- PAT at INR 205mn (-14% vs JMFe) and is +14% YoY

* Our view: The much awaited Rajasthan NHM tender finally materialised during the 1Q, providing much visiblity into the future growth. Given its scale, the management has guided for an INR 3-3.5bn annual revenue contribution from this tender, with meaningful contributions to start from FY27 onwards. Thus, we have increased our revenue estimates for FY27 and FY28, with the growth to flow through to EBITDA level. However, on account of this new tender win, we are reducing the EBITDA estimates for FY26 as these new centers will take time to ramp-up. Further, the expected depreciation drag on PAT margin for FY26 is much higher than our initial estimates, as the parallel revenue will start contributing from next year. Thereby, we have reduced our FY26 EPS estimates. To summarize, we continue to be positive on the company with expected FY25-28 CAGR of 24%/24%/34% across revenue/EBITDA/PAT. Thus, we continue to value the company at 24x its June’27 EPS to arrive at a TP of INR 1,127.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361