Add Max Financial Services Ltd For Target Rs. 1,950 By JM Financial Services Ltd

Axis Max Life reported APE/VNB growth of 15%/27% YoY in 2Q. [link to our First Cut] On margins, the company saw a 60bps hit due to GST 2.0, adjusting for which the margin expansion would have been 250bps for 2Q. Management explained that 60-70% of the expansion was led by product mix with the remaining coming from higher margin in the product categories – higher rider attachment, yield curve movements, etc. Management maintained its guidance for a growth of 300-500bps above industry and FY26e margins of 24-25%, both positive. The company looks on track to achieve these. We expect a steady 16% topline growth over FY25-FY28e, with expanding margins. We do not materially change our estimates. At CMP, the stock is trading 1 SD above its mean valuations, hence, despite the strong performance; we expect the stock to rerate only gradually. We raise our target price to INR 1,950, valuing the company at 2.4x FY27e EVPS (against 2.2x earlier) of INR 1,008 (down from INR 1,021). We downgrade to ADD.

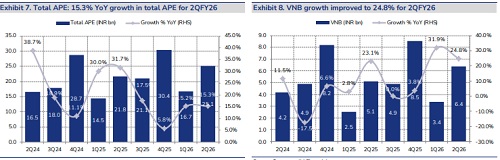

* APE growth in line with RWRP, prop was strong at +18% YoY: While individual APE grew a strong 15% YoY, slightly ahead of RWRP (Retail Weighted Received Premiums) growth of 14% reported to IRDAI, which was ~800bps lower in 1Q. Growth was led by proprietary channel, up 18% YoY to INR 19.4bn, while partnership channel also reported a healthy growth of 13% YoY. Axis banca grew 7% YoY and the strong 13% growth was led by smaller and

* Strong margin performance led by product mix: The product mix shift was sharp on a YoY basis - ULIPs declined by 7% YoY, while non-par grew at 17%, also seen a sharp increase in annuity by 85%. While we had anticipated the mix shift away from ULIPs towards non-linked savings, the strong shift from ULIP to non-par is seen in this quarter. Meanwhile, group credit life grew ahead of expectations, at 23%. the company saw a 60bps hit due to GST 2.0, adjusting for which the margin expansion would have been 250bps for 2Q. Management explained that 60-70% of the expansion was led by product mix with the remaining coming from higher margin in the product categories – higher rider attachment, yield curve movements, etc. The company hits its VNB for the 9 days starting 22nd September, and the impact on renewals was considered in its EV. Gross impact due to GST 2.0 was quantified at 300-350bps while the GST impact on EV was INR 2.7bn, 1.1% of opening EV. The improved product mix should compensate for the impact, and we cut our FY26e margins by only 20bps to 24.8%.. EV grew (2% QoQ, 15% YoY) to INR 268.9bn, in line with JMFe. The company has passed on the GST benefits to customers and is discussing with distributors to share the hit.

* Valuation and view – strong performance should continue, see limited room for rerating, downgrade to ADD: Management has guided for a growth of 300-500bps above the industry in FY26 and in the medium term, with margins in the guided range of 24-25% in FY26e. We cut our FY26e VNB margins by 20bps to 24.8%, and maintain our growth estimates of a steady 16% YoY over FY25-FY28e. This results in a ~1% hit to our VNB and EV estimates. . At CMP, the stock is trading 1 SD above its mean valuations, hence, despite the strong performance, we expect the stock to rerate only gradually hereon. We value the stock at 2.4x FY27e EVPS of INR 1,008 (against 2.2x FY27e EVPS of INR 1,021 earlier) to get a revised target price of INR 1,950. We downgrade to ADD.

Please refer disclaimer at https://www.jmfl.com/disclaimer

SEBI Registration Number is INM000010361