Buy LG Electronics India Ltd for the Target Rs.1,860 by Motilal Oswal Financial Services Ltd

Demand recovery in sight; margin poised to improve

Category outperformance continues; scaling up new growth engines

* Our recent interaction with LG Electronics India (LGEIL) management suggests that LGEIL continues to gain market share across key categories despite mixed industry trends, with refrigerators growing marginally against a 1.5-2.0% industry decline and TVs delivering 6.4% growth vs. 3.8% growth for the industry. In RAC, LGEIL outperformed with a lower volume decline (~4% vs. ~6% industry). The strong growth is being driven by premiumization and deeper portfolio expansion, with the entry into five-star two-ton, sub-one-ton, and fixed-speed AC segments, significantly widening its addressable market across price and capacity bands. It has implemented calibrated price hikes across categories to offset cost pressure. The company is also scaling adjacencies – AMC, B2B and export businesses.

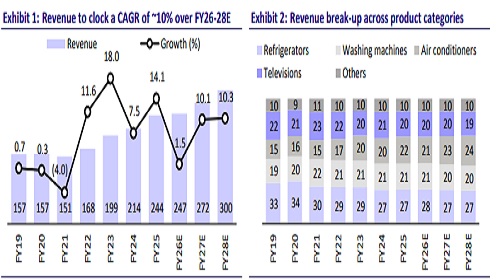

* We estimate LGEIL’s revenue/EBITDA/PAT CAGR at 10%/22%/23% over FY26-28. The stock trades at 46x/39x FY27/FY28E EPS. We value LGEIL at 45x FY28E EPS to arrive at our TP of INR1,860. Reiterate BUY.

Sustained market share gains, demand momentum strong

* LGEIL continues to demonstrate resilient market share gains across key product categories despite mixed industry demand conditions. Refrigerator market declined 1.5-2.0%, yet LGEIL recorded marginal growth, supported by premium product expansion, including French door models in Nov’25 and an expanded bottom-freezer portfolio. The company holds a strong ~43% share in side-by-side refrigerators.

* In televisions, industry growth stood at 3.8%, whereas LG outperformed with 6.4% growth, leading to consistent share gains and narrowing the gap with Samsung Electronics to 4.3%. LGEIL market share in TV stood at 27.4%.

* In RAC, industry volumes declined ~6%, while LGEIL saw a relatively lower decline of ~4%, resulting in further share improvement. The gap with VOLT has narrowed to ~1% now.

* LGEIL indicated strong momentum across product categories, particularly televisions and washing machines, with likely double-digit growth aided by demand tailwinds such as GST rationalization and festive consumption. The company aims to complete ~55% of RAC seasonal targets during Jan-Mar’26, supported by early channel filling for new star-rated models and stable pricing from launch

Portfolio expansion, premium mix, and distribution strength led growth

* Growth is being led by premiumization and expansion into new underrepresented segments. It has strategically expanded RAC portfolio, entering into the five-star two-ton AC and sub-one-ton models under the Essential series to tap into compact-room demand and affordable premium segment. Further, recognizing that ~12% of the industry comprises fixed-speed ACs, LGEIL has now entered this segment as well, introducing energy-efficient three-star models. These launches meaningfully broaden its addressable market and enhance participation across key capacity and price bands.

* The Essential Series continues to gain traction, targeting first-time buyers and underpenetrated markets across refrigerators, washing machines, and RACs. The company is expanding refrigerator offerings from four models to 11, launching 10kg washing machines and introducing 0.9-ton inverter ACs for the affordable premium segment.

* Dealer preference remains strong given LGEIL’s higher sell-through and stable pricing, supporting shelf visibility across its 36,000+ touchpoints and 800+ franchise-owned stores. Distribution reach remains a structural advantage, with ~500 distributors servicing 100–500 sub-dealers each, particularly strong in Tier2 markets. Manufacturing continues to be segmented by product positioning, with premium categories (TV, WMs, side-by-side refrigerators) produced in Pune and mass products in Noida.

Calibrated price hike and cost-saving measures to drive margin expansion

* The company has implemented price increases across categories to offset cost pressures, with ~9% for 5-star ACs, ~7% for 3-star ACs, and ~2% hikes in refrigerators and washing machines from Oct’25, alongside reduced promotional intensity. The price hike was inevitable due to the cost pressure amid higher input material costs, rupee depreciation, regulatory changes in scrap procurement pricing (increased minimum price) mandated by government-approved vendors, and new energy efficiency norms.

* After near-term margin pressure, management expects structural margin gains through mix enrichment and premiumization. Premium products contribute ~28% of sales vs. industry levels of ~16-17%, with further upside expected. Product engineering initiatives such as simplified refrigerator components and motor technology optimization in washing machines are designed to maintain affordability without compromising margins. Its RAC portfolio is positioned at ~10% premium to Voltas and ~4% above Daikin, reflecting brand strength.

* Localization continues to strengthen with domestic sourcing rising from 45-46% three years ago to 57-58% currently, with a target of ~65% over 3-4 years. Key components, including compressors, PCBs, and heat exchangers, are increasingly manufactured in-house, while panel sourcing from TCL locally has risen from zero in FY22 to ~30% currently, with a 50% target. Compressor capacity expansion remains a strategic priority. It consumes 1.8m compressors annually, with 0.9m currently produced in-house. New compressor facility is targeted by Mar’27 (Phase-2 of Sri City expansion), which should meaningfully reduce cost dependence on external suppliers.

* Annual maintenance contracts are expected to grow from USD40m in CY24 and USD60m in CY25 to USD100m by CY26. The B2B segment (~10% of revenue) includes VRF systems, cassette ACs, Chillers, data-center cooling solutions, HVAC equipment and interactive displays. B2B segment was growing at ~20% over the past few years, while it is estimated to be flat YoY in FY26.

* LGEIL plans to significantly scale up its export contribution. It has commenced manufacturing side-by-side refrigerator models that meet US specifications and has already secured export orders for these products. In addition, it exports mid- and entry-level products to over 50 neighboring countries and is strengthening its distribution network in these markets to drive growth. LGEIL is also targeting an expansion of microwave exports to Europe going forward.

Valuation and view

* LGEIL has established itself as a strong player in various consumer electrical categories, such as TVs, refrigerators, washing machines, RACs, and microwave ovens. The industry outlook remains constructive, led by rising preference for premium, energy-efficient products, while low penetration levels continue to offer volume-led growth opportunities.

* We estimate a CAGR of ~10%/22%/23% in revenue/EBITDA/PAT over FY26-28. We estimate OPM to expand to 12.0%/12.7% by FY27/FY28 vs. 10.3% in FY26. It has consistently generated positive operating cash flows over the years. We estimate a cumulative OCF of INR72b during FY26-28; however, its capex plans for the Sri City plant (INR39b to be spent during FY26-28E) are expected to moderate its FCF. Cumulative FCF during FY26-28 is estimated at INR33b.

* The stock trades at 46x/39x FY27/FY28E EPS. We value LGEIL at 45x FY28E EPS to arrive at our TP of INR1,860. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH00000041