Buy LG Electronics India Ltd for the Target Rs 1,750 by Motilal Oswal Financial Services Ltd

4Q earnings below estimates; FY27 expected to be strong Guiding mid-teen revenue growth; early double-digit margin in FY27

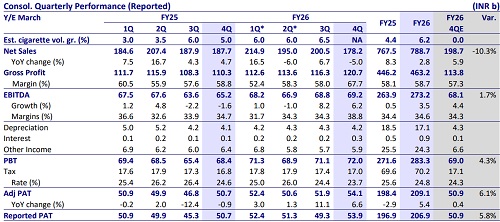

* LG Electronics India’s (LGEIL) 4QFY26 earnings came in below our estimates due to lower margins in both home appliances & air solution (H&A) and home entertainment (HE) segments. Revenue grew ~8% YoY to INR80.5b (in line). EBITDA declined ~10% YoY to INR9.5b (~12% miss). OPM contracted 2.4pp YoY to 11.7% (est. 13.2%). Adj. PAT declined ~8% YoY to INR6.9b (~14% miss).

* Management expects margin normalization in FY27, driven by calibrated price hikes, operating leverage, better product mix and higher localization. Demand outlook remains robust, supported by strong summer-led sellout, lean channel inventory and structural under-penetration in key categories like air conditioners. Premium segments of refrigerators and large-screen TVs continued to see healthy traction. It is guiding for mid-teen revenue growth and early double-digit EBITDA margins in FY27.

* We largely maintain our estimates for FY27-FY28. The stock trades at 44x/38x FY27/FY28E EPS. We value LGEIL at 45x FY28E EPS to arrive at a TP of INR1,750. Reiterate BUY.

H&A/HE margin contracted 2.5pp/2.8pp YoY to 11.9%/13.4%

* LGEIL’s consol. revenue/EBITDA/adj. PAT stood at INR80.5b/INR9.5b/ INR6.9b (+8%/-10%/-8% YoY; -1%/-12%/-14% vs. our estimates) in 4QFY26. OPM contracted 2.4pp YoY to 11.7%. Depreciation and interest costs rose 5%/59% YoY, while other income increased ~67% YoY.

* Segmental highlights: a) H&A revenue increased 6% YoY to INR65.2b, and EBIT declined ~13% YoY to INR7.7b. Segment margin dipped 2.5pp YoY to 11.9% due to cost pressure. b) HE revenue rose ~20% YoY to INR15.4b; however, EBIT declined 1% YoY to INR2.1b and margin dipped 2.8pp YoY to 13.4%.

* In FY26, revenue/EBITDA/adj. PAT stood at INR246b/INR24.2b/INR17.1b (+1%/-22%/-22% YoY). OPM contracted 2.9pp YoY to 9.8%. OCF stood at INR17.2b vs. INR16.5b in FY25. Capex stood at INR11.7b vs. INR3.4b in FY25. FCF stood at INR5.5b vs. INR13.1b in FY25.

Valuation and view

* Despite posting strong revenue and volume traction, mainly in RAC and premium segments, LGEIL saw margin pressure in 4QFY26 due to cost headwinds. The long-term outlook remains structurally favorable, led by low RAC penetration (~13%), rising premiumization, urbanization and increasing replacement demand, although near-term volatility from weather patterns, input costs and pricing actions may persist. LGEIL appears well-placed to outperform, supported by its strong brand equity, leadership in premium categories, and well-balanced portfolio spanning both mass (essential series) and high-end products. The ramp-up in exports, further improvement in localization and scale-up of AMC business remain key monitorables.

* We estimate a CAGR of 10%/24%/25% in LGEIL’s revenue/EBITDA/PAT over FY26-28. We estimate the H&A segment’s revenue CAGR of ~11% over FY26-28E and margin at ~12%/13% in FY27/FY28 vs. ~10% in FY26. The HE segment’s revenue CAGR of ~8% over FY26-28, and the margin is projected at ~14%/15% in FY27/ FY28 vs. ~13% in FY26. Net-cash balance is estimated to increase to INR57.3b by FY28 vs. INR44.8b in FY26. ROE/ROCE are estimated to improve to ~27%/28% in FY28 vs. 25%/26% in FY26. The stock trades at 44x/38x FY27E/FY28E EPS. We value LGEIL at 45x FY28E EPS to arrive at a TP of INR1,750. Reiterate BUY.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412