Buy ACC Ltd For Target Rs. 2,403 By Yes Securities Ltd

Strong volume, better pricing, and synergy benefits to play out

Result Synopsis

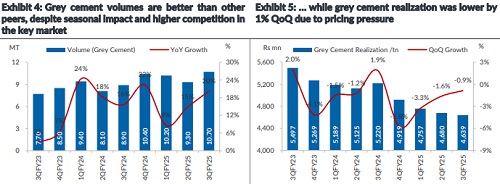

ACC Ltd, on standalone basis, have reported strong numbers in 3Q led by strong volume and high incentive amidst marginal decline in realization (~1% QoQ). After taking out incentive amount of Rs6.4bn from the revenue numbers, the numbers were 1). Revenue from its cement business were up by ~7% YoY and 14% QoQ primarily driven by strong volume (+20% YoY/ +15% QoQ) despite a realization decline (-11% YoY/ 1% QoQ). 2). EBITDA in absolute numbers down by 48% YoY but up by 10% QoQ. While EBITDA/tn was at Rs442 (-57% YoY/ -4.3% QoQ) is better than Ambuja’s consolidated numbers. Overall opex/tn remained flattish YoY as well as QoQ, implies better cost efficiency in 3Q. Despite certain regional and seasonal challenges, ACC have reported better numbers than Ambuja in 3Q. Despite having major capacity in eastern and southern region where prices/ demand are weak, the volume growth is strong in 3Q as compared to other regional and large players so far reported their numbers.

1.6mtpa grinding unit at Sindri, Jharkhand and 2.4mtpa grinding unit at Salai Banwa, Uttar Pradesh is expected to commission by 4QFY25 / 1QFY26 respectively. ACC’s current capacity utilization stands at 91% which is almost near to peak level. We expect the upcoming capacity to add volumes to cater increment demand in the regions (i.e., central). We are factoring a volume growth at 7.1% CAGR over FY24-FY27E at avg. capacity utilization of 97%. Though industry is facing certain challenges especially weak pricing, we believe various cost saving programs coupled with Master Supply Agreement (MSA) and synergy benefits to control cost structure in near-term to lead margin expansion. ACC’s MSA with Ambuja Cement, Sanghi Industry and volume addition from Penna Cement have helped to improve volume. Ongoing cost efficiency projects, higher usage of captive coal mines and green energy usage, reduction in lead distance through warehouse optimization are the key focus area of the management to reach a cost savings of Rs450-500/tn (Ambuja + ACC) in near-term. Despite weak realization, we believe, ACC’s EBITDA to improve further led by cost respites. We are factoring avg. cost saving of Rs153/tn over next three years to arrive at an EBITDA/tn of Rs718/ Rs763/ Rs979 level in FY25E/ 26E/ 27E.

Outlook & Valuation: At the current market price, the stock is trading at 8x Sep’26E EV/EBITDA. anticipate tepid industry growth in FY25E, impacting ACC due to pricing pressures and regional challenges. However, we expect gradual improvement from FY26E onwards. We have cut our estimates and building Revenue/ EBITDA/ PAT at 3.5%/ 11.5%/ 5.9% CAGR over FY24-FY27E in the anticipation of weak pricing and slow demand. And we reduced our Sep’26E EV/EBITDA multiple to 10x (Earlier 11x) with revised target price of Rs2403 (Earlier Rs2909) maintain BUY rating. Any price decline, weak demand and delay in capacity expansion is key downside risk to our recommendation.

.

Please refer disclaimer at https://yesinvest.in/privacy_policy_disclaimers

SEBI Registration number is INZ000185632

.jpg)