Neutral Oil and Natural Gas Corporation Ltd for the Target Rs. 250 by Motilal Oswal Financial Services Ltd

Muted volume growth in 1HFY26

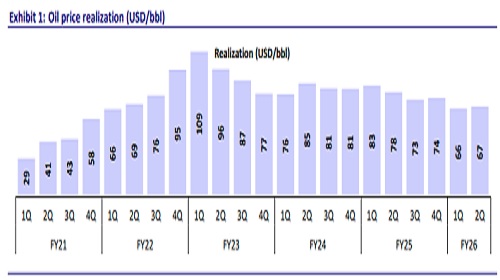

* ONGC’s 2QFY26 revenue came in line with our est. at INR330b. Crude oil/gas sales were in line with our est. at 4.8mmt/3.9bcm. VAP sales stood at 592tmt (est. 681.5tmt). Reported oil realization was USD67.3/bbl, a USD3.2/bbl discount to Brent in 2Q. EBITDAX/PAT also stood in line with our est. at INR177b/INR98.5b.

* Upstream has remained our least preferred sector since Jun’24 (Upstream remains our relatively less preferred sector despite cheap valuations): We have been bearish on crude oil prices since Jun’24 when Brent oil prices were USD83/bbl amid record-high OPEC+ spare capacity (Oil price outlook: Has the crude oil party peaked?). Since then, Brent prices have corrected ~23%, while ONGC’s stock price has corrected ~10%.

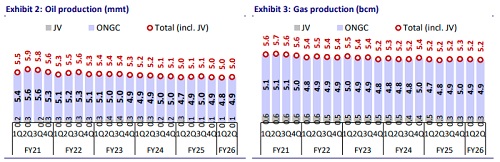

* For FY26, standalone production is guided at 19.8mmt of oil and 20bcm of gas, reflecting a marginal reduction vs. the previous guidance due primarily to delays in the ramp-up at KG-98/2. For FY27, guidance is maintained at 21mmt of oil and 21.5bcm of gas (i.e., 4%/5% CAGR w.r.t oil/gas production over FY25-27). However, in the past few quarters, ONGC has struggled to raise production/sales, with marginal YoY production/sales growth in 1HFY26. Hence, we build in a CAGR of 2%/3% in ONGC’s standalone oil/gas production over FY25-27, reaching 20.4mmt/20.8bcm in FY27.

* We maintain our Neutral rating on the stock and arrive at our SoTP-based TP of INR250 as we model a CAGR of 2%/3% in oil/gas production volume over FY25-27.

Key takeaways from the conference call

* Current NW gas is 13.4% of total gas, which should ramp up to 30-35% in the next three years.

* KG-98/2 -- Current production: 28kb/d oil and 3mmscmd gas. KG-98/2 gas productions should reach 10mmscmd by Jul’26.

* OPAL should run at 90%+ CUF in 2HFY26. Management also expects positive EBITDA in 2HFY26.

* FY26 standalone capex guidance is maintained at INR300-350b.

In-line performance; Volume growth remains weak

* Standalone 2Q revenue came in line with our est. at INR330b.

* Crude oil/gas sales were in line with our est. at 4.8mmt/3.9bcm. VAP sales stood at 592tmt (est. 681.5tmt).

* Reported oil realization was USD67.3/bbl, a USD3.2/bb discount to Brent during the quarter.

* Crude oil and natural gas production remained flat QoQ/YoY.

* Standalone EBITDAX/PAT came in line with our est. at INR177b/INR98.5b.

* DDA, dry well write-offs, and survey costs stood below estimate at INR74.7b.

* Both tax rate and other income came in below estimate.

* ONGC Videsh:

* OVL’s oil and gas production was down YoY at 1.72mmt/0.61bcm (1.82mmt/0.71bcm in 2QFY25).

* Crude oil sales stood at 1.27mmt, while gas sales came in at 0.4bcm.

* OVL’s revenue (incl. other income) was INR21.6b and PBDT stood at INR6.4b.

* The board has declared an interim dividend of INR6/sh (FV: INR5/sh).

Valuation and view

* In the past few quarters, ONGC has struggled to raise production/sales, with no meaningful production/sales growth YoY in 2Q. Further, we like the increased exploration intensity (which is key to building a robust development pipeline), though we believe it will likely be accompanied by higher dry well write-offs, which will weigh on earnings. Also, the benefits of increased new well gas proportion for ONGC will be mostly offset by subdued gas realization amid a weaker crude oil price outlook.

* We arrive at our SoTP-based TP of INR250 as we model a CAGR of 2%/3% in oil/gas production volume growth over FY25-27.

For More Research Reports : Click Here

For More Motilal Oswal Securities Ltd Disclaimer

http://www.motilaloswal.com/MOSLdisclaimer/disclaimer.html

SEBI Registration number is INH000000412